Guillaume Jamet, principal portfolio manager of the Lyxor Epsilon programme, comments: “This performance illustrates the de-correlating property of trend-following strategies”.

The market environment has been mixed for trendfollowing strategies over the last quarter, as illustrated by the SG Trend Index which returned -1.2% in Q2. Trendfollowing strategies thrive in environments in which

- Markets show clear trends, and

- Returns between asset classes are weakly correlated, allowing volatility to be reduced by diversifying across multiple asset classes

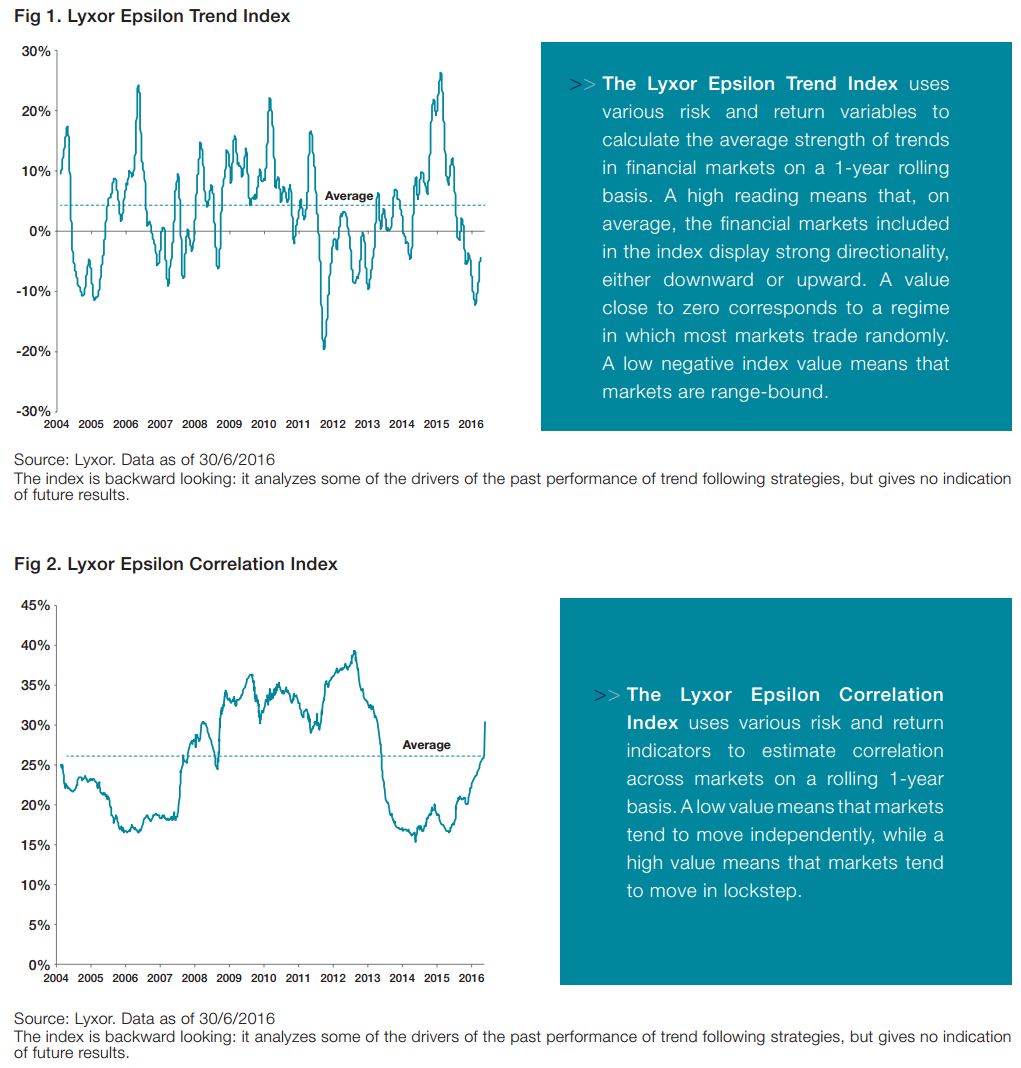

The first condition has not been met: market trendiness remains low, as indicated by the Lyxor Epsilon Trend Index, which reached -4% at the end of June, well below the historical average of 4% – see figure 1. The second condition has been partially met: market correlations remained low. As indicated in figure 2, the Lyxor Epsilon Correlation Index remained below its historical average of 26%, except the week following the Brexit, when it jumped to 4% above it. “Clearly, the Brexit impacted correlation statistics,” says Jamet. “However, there is as yet no indication that we are entering a systematic high correlation regime like the one from 2008 to 2012”.

“In the current environment risk management is key” says Jamet. “Four years ago we did a major review of the underlying model of the Epsilon programme. We introduced diversification over implicit risk factors, rather than over asset classes. We now see that this innovation has paid off. Our 3-year annual performance is 12.6% as at the end of June, while keeping to our target volatility of 10%. This places us in the top quartile of our peer group.”

The last few months featured several clear market trends, which all seemed to anticipate a Brexit, including:

- Depreciation of the British pound

- Appreciation of the Japanese yen, which typically serves as a safe haven for Asian investors

- Rally in both Gilts and Bunds, as a result of flight to quality and in anticipation of even more accommodative monetary policies.

Jamet elaborates: “Epsilon was able to benefit from all these trends. In the months before the referendum, markets were pricing in a Brexit. In contrast with many discretionary managers, CTAs did not overreact to the reversal in market sentiment which occurred the week before the actual vote, and held on to their long Brexit positions. This illustrates the advantage of a strategy which analyses markets differently.”