A recent drop in energy-related assets looks to be overdone. We believe this creates opportunities in selected energy equities and credit — even as we see oil prices trading mostly sideways in the near term.

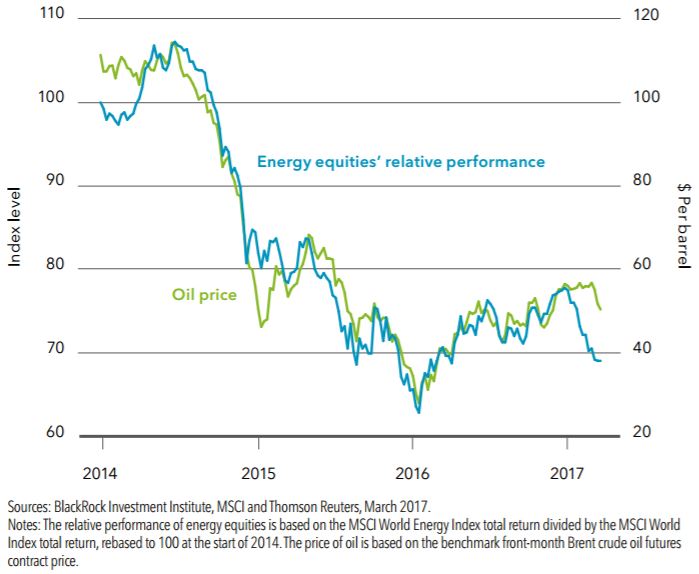

World energy equities’ relative performance and crude oil prices, 2014-2017

Oil prices fell this month after trading in a tight range in early 2017. Concerns about oversupply led to the unwinding of record-levels of speculative bets on higher crude prices. Energy stocks, however, appear to be pricing in too much pessimism. See the increasing performance gap between oil and global energy stocks above.

In a range-bound world

Demand and supply conditions supported oil prices earlier this year. Speculative trades in futures markets also contributed to crude’s rise on expectations the Organization of Petroleum Exporting Countries (OPEC) and non-OPEC countries would implement agreed-upon production cuts. Nervousness about record levels of such positions, rising U.S. supply and growing doubts about production-cut compliance sparked oil’s recent price drop. Further unwinding could pressure prices further in the short term.

Oil prices are hard to predict, as production cuts hinge on an uncertain political environment. We see oil trading mostly sideways over the next few months. OPEC members have shown discipline in cutting oil production, and U.S. inventory growth should soon stabilize as oil refiners increase purchases. Global demand is also likely to rise amid reflation.

Energy stocks appear to reflect a more bearish price outlook. This creates opportunities. We like U.S. shale companies, amid cost cuts, improving technologies and prospects for looser regulation. We also see value in the diversification potential offered by integrated-energy firms, including relatively cheap European oil majors. High yield energy bonds offer slightly better value after a recent sell-off. We prefer the debt of exploration companies due to attractive yields and balance sheet discipline.