Background of the asset class

Corporate bonds have an attractive long-term risk/return profile. Historically the asset class generates returns somewhere between equities and sovereigns but, in the past five (albeit exceptional) years and in a favourable environment of global deleveraging, it has far outperformed equities. Corporates are a long-established asset class in the US where they are the mainstay of many pension funds and the asset class is expanding rapidly. Post credit crunch, many companies have turned to the credit markets rather than the banks for funding. Thus it is that Emerging Markets corporates has grown into an asset class of its own.

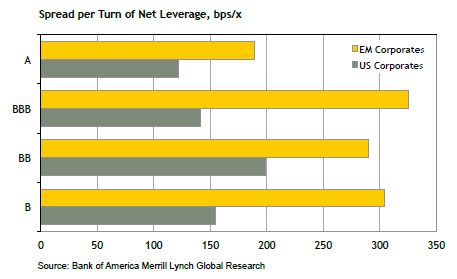

In the Emerging Markets, credit markets are maturing just as rapidly as stock markets. Not only do EM corporates offer attractive diversification away from EM sovereigns and equities, they also currently offer very attractive return potential, compared with their US counterparts. As the chart below shows, EM corporates are paying more per unit of risk than US corporates across much of the credit spectrum. With the High Yield credit premium at 800 basis points and Investment Grade at 250 basis points, the willingness of investors to settle for historically low or negative interest rates from US and European ‘safe’ sovereign bonds is all the more surprising.

- Spread per Turn of Net Leverage

What makes these risk premia all the more attractive is the fact that default risk is lower on average in Emerging Market nations because of the corporate tradition of keeping debt levels low and cash levels high. The higher cash buffers in EM companies will also help them to withstand recession better and invest for growth as the recession ends.

Investment opportunities in EM bonds

As markets begin to mature and companies are able to demonstrate a history of debt repayment and creditorfriendly behaviour, so a value approach to corporate bond investment becomes possible. As with value equity investment, value bond investment means looking for pricing inefficiencies in the markets and investing with a ‘margin of safety’ which hinges on a low net-debt-toequity ratio. Experience has shown that value and smallcap bonds in companies with low debts generate excess returns and therefore represent an identifiable alpha factor in the credit universe. This effect can be amplified in Emerging Markets. For example, we frequently find examples of smaller companies and value companies that are penalised by rating agencies for reasons totally unrelated to their ability to repay their debts. Also, the ‘sovereign ceiling’ effect has, in the past, meant that for some emerging market corporates, ratings are marked lower simply on grounds of the company’s head-office location. However, given that Developed Countries’ sovereign ratings seem to be on a negative trend - whereas we still expect positive rating actions among EM sovereigns we would expect future convergence between the average ratings of the more mature Emerging Market countries with Developed Market countries.

A value approach to corporate bonds seeks to identify ‘overlooked’ and under-rated companies that are forced to pay high yields while offering solid business models or assets or cash backing as a margin of safety for debt repayments.

Integrating SRI/corporate governance information

SRI and corporate governance insight is as important to fixed income investors as it is to long-term equity investors because any risk that might erode a company’s future profitability is also a threat to its capacity to repay debts. Corporate governance is known to be weaker in Emerging Market companies - although it is improving – and this is one of the reasons that EM corporates need to pay higher yields. Thus a thorough analysis of corporate governance should be included as an essential step in the corporate bonds investment process. Failure to consider environmental, social and governance risks can expose investors to large ‘tail risk’ like litigation risk or the risk of large lawsuits arising from – for example – environmental disasters. Rule of law and property rights are also an important consideration. For example the Mongolian Government has made a ‘National List’ of resources and sectors of strategic importance. This type of action could end up in assets being expropriated from companies– which may involve a significant headline risk for their debt holders.

What is the outlook for EM corporate bonds?

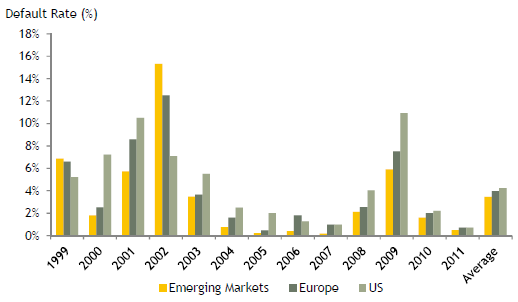

The pace of economic growth has been slowing in the emerging market economies. But this is potentially good news for credit investors. For a start, the extreme pace of economic growth was starting to cause problems for companies - such as increasing salary costs, increasing inflation affecting raw material prices and decreasing global competitiveness. But in general, lower growth scenarios favour corporate bond investors because they force companies to focus on profitability and careful, organic growth rather than on leveraging up their balance sheets and taking risks. For these reasons and because of the strong cash levels in EM corporates, we expect the default rate, which is already lower on average than in developed markets over the past decade to retain that advantage over the coming years.

- Default Rate