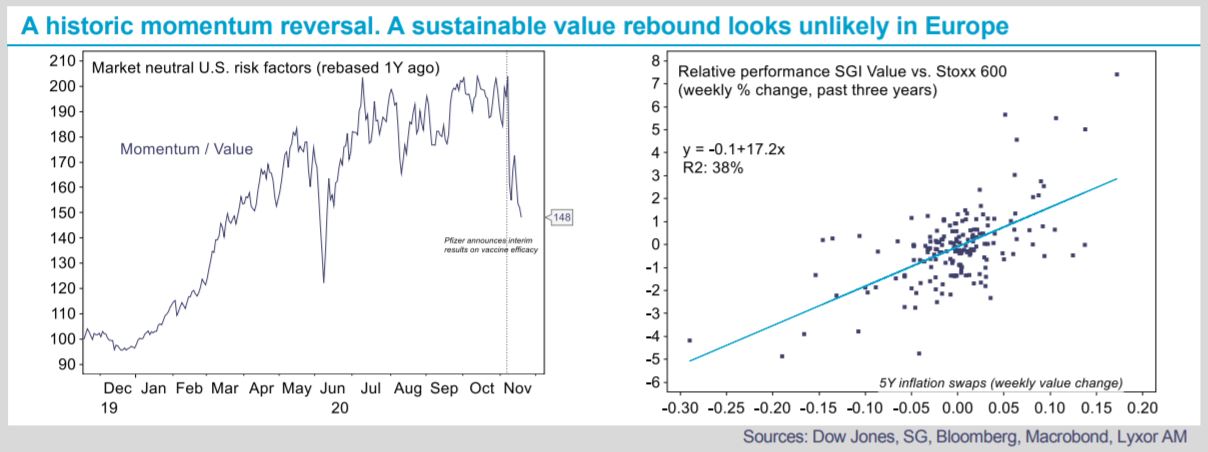

A massive momentum reversal occurred earlier in the month, when Pfizer announced interim results of its Covid19 vaccine. On November 9th, the U.S. Dow Jones Momentum Index fell by a record -14% in a single day. In this long/ short index, value stocks were on the short side and they experienced a massive rebound. Over recent days, such rotation out of momentum/ quality/ low beta into value/ size stocks has continued.

Several hedge fund strategies have momentum biases, in particular L/S Equity, and CTAs. Considering the fact that this rotation took place in a bullish environment, most hedge fund strategies ended the week in positive territory. Directional L/S Equity (+1.2%) benefitted from their market beta, but alpha contributed negatively for all but those strategies with an explicit value bias. One strategy benefitted particularly from the changing market landscape: Special Situations (+3%). In relative terms, their higher market beta and value bias was supportive.

CTAs and Market Neutral L/S ended the week in negative territory but losses, in the range of -1% to -1.5% according to the Lyxor Peer Groups, were overall contained. Dispersion has been high within the Market Neutral L/S space, with 20% of our sample down in excess of -3%, a significant loss for strategies which are traditionally low vol.

Most managers have now neutralized their factor biases to edge against further rotations into value stocks.

Going forward, a sustainable rebound in value stocks looks unlikely, particularly in Europe. A significant part of their

underperformance in recent years was also related to the low inflation/ low yield environment, which looks unlikely

to change. Some value sectors such as financials might benefit from the gradual normalization in economic activity,

which would occur in H2-2021, and could start to normalize dividend distribution next year. In parallel, momentum

crashes are usually short lived. In this context, we maintain the UW stance on Market Neutral L/S and upgrade.