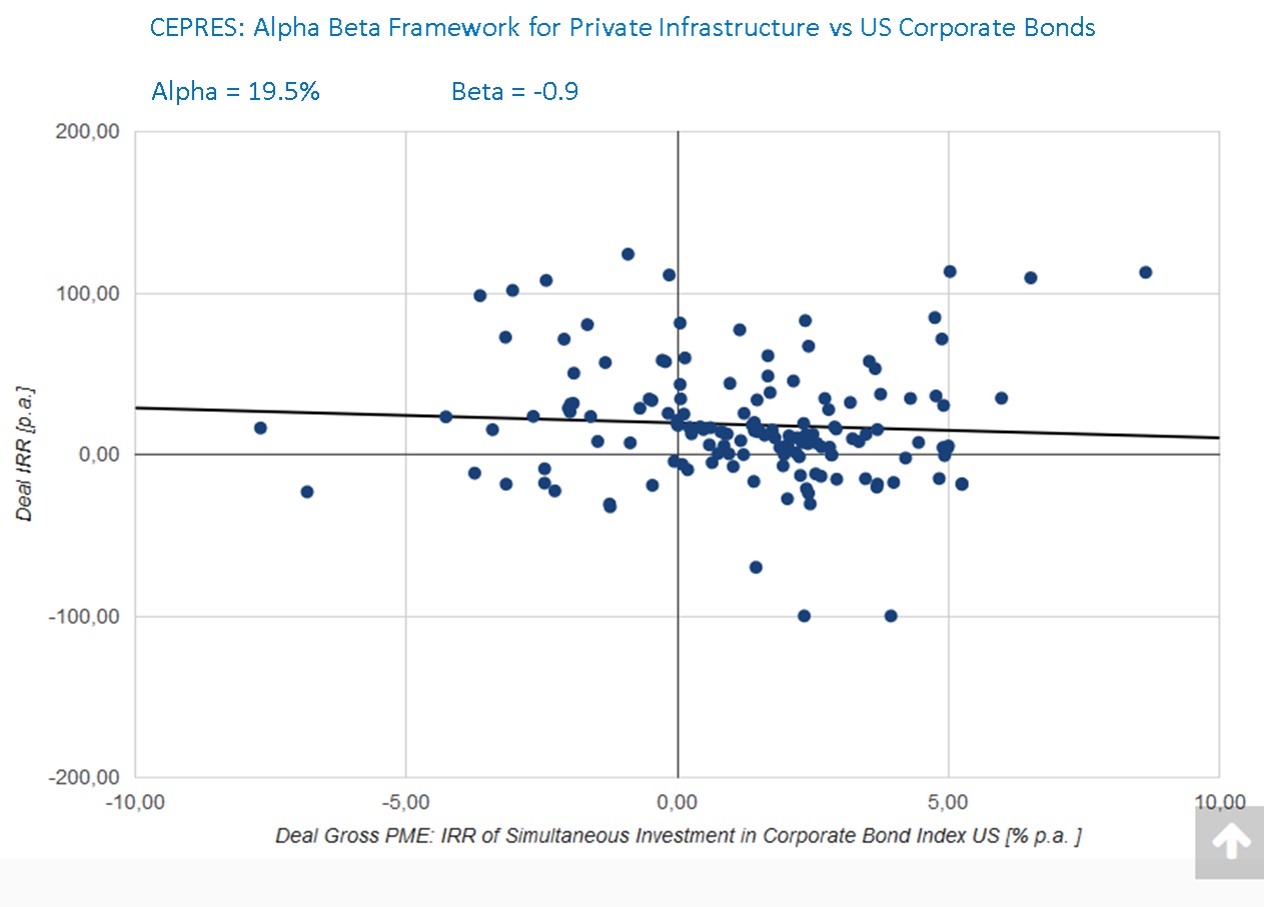

CEPRES today released an analysis demonstrating how Private (unlisted) Infrastructure can act as a Hedge for Corporate Bonds, whilst significantly outperforming on returns. Using PE.Analyzer to analyze thousands of privately held Infrastructure assets, CEPRES found that since 2002 there was a beta (co-movement) to the US Corporate Bond market of -0.9 and an alpha of 19.5%.

The results were derived from the new PE.Analyzer ‘Alpha Beta Framework’ that uses regression analysis to calculate the risk adjusted return (alpha), together with the correlation (beta) to an underlying market – in this case US Corporate Bonds. This new feature is ground breaking and brings private market investing to the same level as public market trading, because previously it was so challenging to perform this type of analysis based on reliable data.

- Risk adjusted alpha for Private Infrastructure versus US Corporate Bonds = 19.5%

- Beta correlation for Private Infrastructure versus US Corporate Bonds = -0.9

- A beta of -1 is a pure hedge to the comparative market

- Energy infrastructure adds higher outperformance, but also cyclicity (and hence risk)

Dr. Daniel Schmidt, CEO, CEPRES GmbH says “Infrastructure, as a yielding asset, can be a useful alternative for liability driven fixed income investors, like pensions and insurers seeking higher returns. For those especially worried about volatility and downward pressure on public markets, PE.Analyzer shows that private infrastructure can help hedge risk and enhance a balanced portfolio. We also saw how energy infrastructure increased returns, but at the cost of cyclicity. This may suit alpha driven investors, but introduce some risk that should be analyzed in the context of a complete Asset Allocation. Further variations for other sub-segments and comparison to other markets can all be done in PE.Analyzer.”