Paul O’Connor, Head of Multi-Asset, gives an update on the risks and opportunities in the run-up to the June EU referendum. With less than 40 days until the vote, opinion polls are fairly stable and suggest “remain” will be the outcome. However, the material risk of “Brexit” has resulted in the following action across their portfolios:

- Lowering UK small and mid-cap exposure

- Neutralising FX exposure

- Maintaining significant cash reserves

The final countdown

With less than 40 days to go until the UK referendum on EU membership, the opinion polls remain tight and fairly stable. Unless the outlook changes dramatically in the weeks ahead, these polls suggest that the race will go down to the wire and that there will be little certainty in the outcome of the referendum until all of the votes have been counted.

While considerable attention is being paid to the weekly surveys of public opinion, they do not give a very clear picture, as differing outcomes are predicted across pollsters and polling methodologies. At face value the overall message is that the two sides are neck-and-neck, as illustrated by the National Centre for Social Research’s latest poll-of-polls, which shows both “leave” and “remain” with a 50% share of the votes. However, we do not believe that the race is actually this tight and continue to see “Brexit” as a sizeable tail-risk for financial markets, rather than a central scenario.

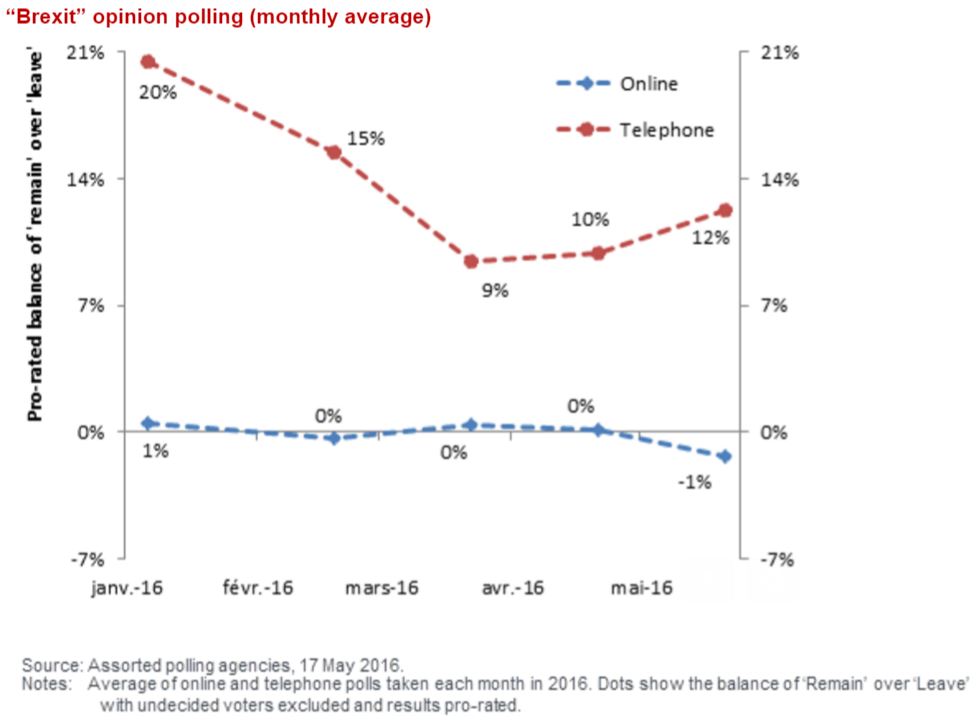

Polls apart

One key challenge in interpreting the evidence from opinion polls is the persistent divergence between the results of online and telephone polls. While the former suggest that the “leave” campaign is marginally in front, telephone polls show “remain” with a double-digit lead (see chart below). The most convincing explanation of this phenomenon is that the online polls involve a greater element of self-selection. They tend to include a more politically-engaged sample of voters, which in this referendum means “eurosceptics”. Telephone polls were more accurate predictors than online polls in the last two general elections and the last two referendums in the UK. With this in mind, we see good reason to favour the predictions of telephone polls over online polls, which leads us to believe that the current state of public opinion (excluding “don’t knows”) is probably closer to 55-45 in favour of “remain” than 50-50.

The undecided

Another important message from the opinion polls is that a large number of potential voters are still undecided. Most polls are recording between 10% and 20% of people as “don’t knows”, but many pollsters believe that this understates the true level of indecision. While at first glance, this would seem to cast even more uncertainty over the outlook, history suggests that support for change tends to drop as a referendum date approaches, implying that undecided voters tend to drift towards the status quo. So, in the absence of any significant new electoral dynamics, the “remain” campaign should expect to pick up more of the “don’t knows” than the “leave” campaign as we approach June 23rd, strengthening its current lead.

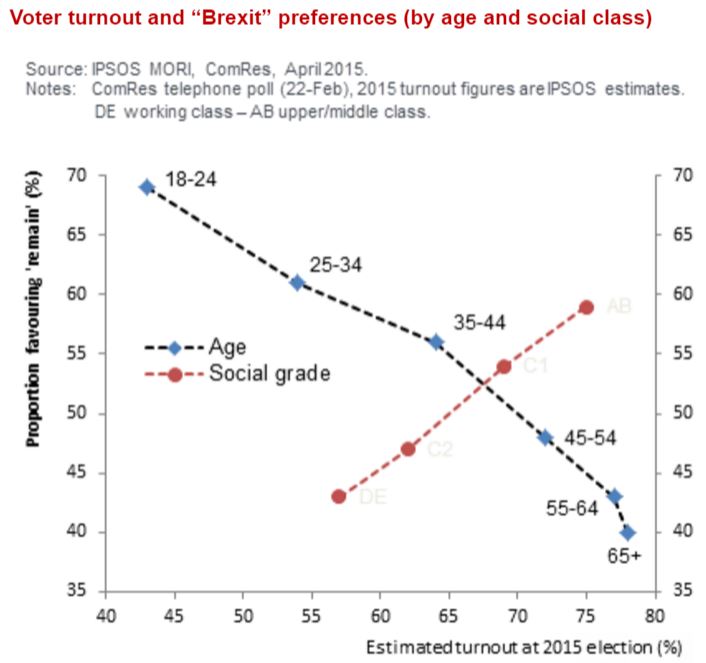

The middle-class versus the middle-aged

A final topic that has attracted a lot of recent attention is voter turnout. The issue here is the potential for turnout rates to affect the outcome of the referendum, particularly if there are different turnout rates for different types of voter. As the chart below illustrates, there are two competing demographic influences. When the population is split by age older voters tend to be both more pro-“leave” and more likely to vote. However, when the population is split by social-grade, the advantage appears to be tilted in the opposite direction, as middle and upper-middle class voters are both pro-“remain” and the most likely to turnout. At this stage, it is not obvious which effect will dominate – attempts by polling agencies to adjust for these effects are inconclusive.

A portfolio perspective

Weighing up all of the evidence, we still expect the UK to vote to remain in the EU, but recognise that there are considerable uncertainties surrounding this outcome. Although the result of the referendum will ultimately be binary (“remain” or “leave”), as investors we have to approach the issue probabilistically. In this regard, we have sympathy with the sort of probabilities priced in by currency markets, bookmakers’ odds and prediction markets, which see a “remain” vote as the most likely outcome, with a probability of just over 70%. However, at a near 30% probability, “Brexit” remains a material tail-risk scenario.

We have begun to make a number of adjustments to our portfolios to reflect this view. Our primary objective is to dampen the downside risk from a Brexit vote, without forgoing the potential for upside in the event that our base case scenario of a “remain” vote occurs. This process began last year, as we reduced our exposure to UK small and mid-cap stocks that tend to be highly exposed to the domestic UK economy. We took additional action at the start of 2016, by trimming our UK property holdings back from overweight to neutral. More recently, we neutralised our FX exposure, realising profits from our overweight positions in foreign currencies that have largely appreciated against sterling year-to-date. Finally, we have built significant cash balances across our funds to ensure that we have the firepower required to take advantage of any dips that might occur before or after the vote.