In this article, we discuss new approaches of commodity index design that address the issues of traditional indices and explain how to invest in this asset class in a risk-controlled way.

This evolution in index design is similar to what was witnessed in equities over the past years under the name of “Smart Beta” Investing. In the commodities market as well, systematicaly applying risk management techniques adds value to the investment process, both on an absolute and on a risk adjusted basis.

Portfolio allocation

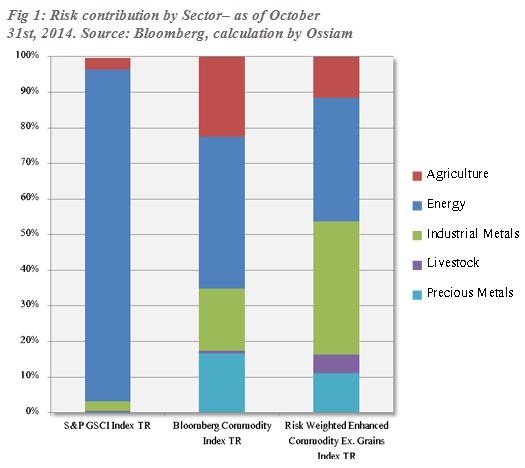

Traditional commodity indices are valid economic indicators but inefficient investment benchmarks for long-term investors. First, traditional indices are based on a cost-inefficient technique to roll expiring commodity futures. Second, the imbalance of production-based weights leads to severe concentration of the related index products on specific commodity sectors such as Energy.

The solution to the first problem has been brought by the second generation of commodity indices, which implement roll optimization techniques: they analyse the forward curves to benefit form backwardation and to limit the cost of contango. These second-generation indices lead to more efficient investments than the traditional indices, yet they fail to address one core problem: the lack of diversification, because they use the classic production based weight allocation.

Recently a new generation of broad commodity indices has emerged. They offer investors simple and efficient ways to access the asset class while ensuring diversification and optimize futures rolling cost.

In an asset class with only around twenty constituents, applying a “Risk Parity” allocation will provide a balanced portfolio containing all the commodities within the investment universe. Risk Parity allocates the same risk budget to each portfolio constituent. The weight of each commodity is inversely proportional to its realized volatility.

Such a construction evens out the risk contributions of the assets within the portfolio and better aligns the weight of differents sectors to the number of constituents they contain.

Figure 1 shows the risk contribution breakdown resulting from applying this risk-parity approach to S&P GSCI® investment set.

Fig 1: Risk contribution by Sector for a Risk Parity Portfolio – as of October 31st, 2014. Source: Bloomberg, calculation by Ossiam

This allocation can be described in an intuitive manner when compared to the most straightforward portfolio construction method, Equal Weighting – all assets have the same weight. The risk parity goes one step further than Equal Weighting in the diversification process. While for an Equally Weighted allocation the sector weights are strictly proportional to the numbers of assets that compose each sector, Risk Parity will also factor in the relative riskiness of each sector. For instance, as Energy futures are generally more volatile than the other commodities, their risk parity weight will thus be lower than what equal weighting would prompt. Livestocks on the contrary will be overweighted because of their relatively lower risk.

The two innovations, enhanced maturity management within mono-commodity indices and risk-aware portfolio allocation, lead to a large reduction in the volatility of broad commodity indices. When applied on the S&P GSCI® universe, it gives a commodity portfolio, the “Risk Parity Portfolio [1]”, with volatility reduced by around 45% comparing to the traditional S&P GSCI® index (over the period 2003-2014). The majority of the reduction (85%) results from the change in the weighting scheme while the remainder comes from the enhancement in roll management.

Portfolios designed around risk management are also better aligned with the new regulations advocating diversification. Additional capping mechanism may be embedded in the portfolio construction process to prevent any breach of the regulatory constraints.

Below we give an example of a new generation commodity index: the Risk Weighted Enhanced Commodity Index (ex Grains), that implements the portfolio construction principles described above and represents a risk-efficient investment benchmark.

Proof of concept

The Risk Weighted Enhanced Commodity ex Grains Index combines the enhanced construction of mono indices with risk parity weighting. In addition, the index methodology forbids investments in grains and ensures that the weight of each commodity sector does not exceed regulatory limits [2].

In Fig 2, we can see that the Risk-Weighted Enhanced Commodity ex Grains Index achieves better performance on the long term, and risk reduction using the allocation management techniques.

Fig 2: Comparison of historical performances and 1 year rolling volatilities for the Risk-Weighted Enhanced Commodity ex Grains Index and the S&P GSCI® index for the period 01/01/2003 to 31/10/2014.

- Source: Bloomberg, calculation by Ossiam

It should be noted that removing grains from the portfolio and introducing sector weight limits do not alter significantly the risk reduction potential: the unconstrained Risk Parity portfolio has roughly the same volatility as the Risk-Weighted Enhanced ex Grains index.

The volatility reduction is not the only benefit of the new index design. Over the period 2003-2014 the alternative commodity portfolios generated consistent overperformance with respect to the traditional S&P GSCI® index. This extra performance came from futures contract selection for 80% of it, the rest resulted from the allocation that was more evenly spread among commodities.