The dollar goes from strength to strength, but what might this mean for the US and other economies?

Over the past decade, we have seen several longer term trends play out, from swift urbanisation in developing nations to technological advances everywhere. Changes in currency trends have also had an impact on economies and stock markets, in particular the directional changes in the world’s reserve currency, the US dollar. In our view, the dollar’s recent strength is likely to continue and this could have major implications for both the US and other economies.

Long term currency shifts

Ever since the US switched to floating exchange rates in 1973, the dollar has been through several shifts in value. While nothing moves in a straight line, these shifts have tended to manifest as medium to long term trends. Between 1973 and 1979, the dollar fell as other currencies strengthened. It then rose to new heights in 1980-85 before falling precipitously in 1985-7 and continuing to fall post the 1987 October market crash until 1995. We then saw an abrupt reversal. The dollar rose throughout the late 1990s reaching a peak in early 2002, following a period of strength in the US economy even as growth in the rest of the world remained relatively stagnant.

Japanese deflation, continental Europe’s muted growth and high unemployment, the Asian financial crisis, and turmoil in places such as Russia and Argentina led to massive capital flight out of those countries and into the global economy’s “safe haven”, the US. Currency intervention by countries such as Japan and China also aided a change in the dollar’s trajectory. These and other (mainly developing) countries continued to buy large amounts of dollars to hold in reserve, which boosted the currency further.

Eventually, however, the US trade deficit started to widen to unsustainable levels. As emerging markets grew in strength and Europe became seen as an engine of growth, money left the US and the dollar, a trend on which the Jupiter Merlin portfolios were able to capitalise.

By 2007, not long before the financial crisis, a pound was worth over two dollars. When the crisis hit, both the dollar and gold, which is priced in dollars, were again ascribed a safe haven status. Extraordinary monetary intervention by the Fed in the years that followed the Great Recession kept the dollar weaker that one might have expected given the global uncertainty. Now that US quantitative easing has come to an end and many commentators are anticipating a rate rise in 2015 amid higher US GDP growth, the dollar has begun to strengthen again.

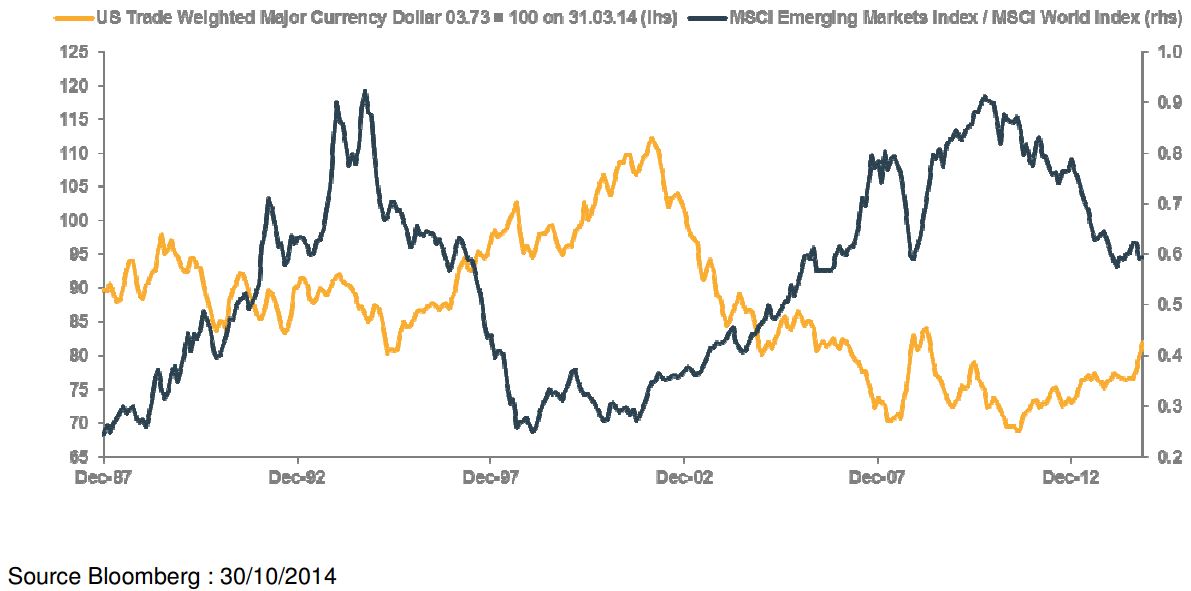

Stronger dollar, weaker emerging markets

However, the corollary of a stronger dollar has been weakness in emerging markets.

Emerging economies often borrow in dollars; as the latter appreciates so does the local currency size of their debt burden and interest payments, which is, of course, financially very painful.

As the chart shows, this sort of correlation is not unusual, cf. the 1990s Asian financial crisis. This time, weakness in developed markets such as Europe and more quantitative easing in Japan have caused major world currencies to fall in value too. If this trend persists for an extended period, we could see further intervention by countries such as China, whose renminbi is partially pegged to the dollar, to suppress the value of their currency, potentially through allowing a larger proportion to be free floating.

Chart 1: Emerging markets tend to struggle when the US Dollar is strong

The oil factor

An additional factor in this cycle has been the exploitation of oil shale reserves in the US, which has led to an oversupply of oil across the world and a 40% drop in the price [1]. Given that 72% [2] of the US economy is consumer-driven, this “tax cut” could drive further domestic growth. As an Economist headline of the early 1980s had it: “Cheaper oil makes ya strong”! It will, however, have an impact on oil producers.

In our view, this trend towards a stronger dollar is likely to continue, for the most part because the Fed is unlikely to intervene unless it becomes absolutely necessary to do so. A strong dollar is likely to have a limited impact on the domestic economy, as exports account for just 14% of US GDP compared, for example, to 32% for the UK [3].

Meanwhile, lower oil prices and weaker currencies are likely to benefit exporters in Europe and Japan as manufacturing and transport costs fall. We remain alive to the potential consequences of such an important change, as it is likely to impact both countries and companies, and ready to move swiftly to take advantage of opportunities as they open up.