Britain’s unexpected decision to vote to exit the European Union has hit emerging market (EM) assets hard. Local currency bonds are down 3.0% while EM equities have lost 4.9% since the vote (JP Morgan GBI-EM Global Div and MSCI EM Equity). In our view, this impact will only be sustained to the extent that it has a fundamental impact on the global economic outlook.

EMs do not have significant direct exposure to the UK, and hence the impact on EM trade of a UK recession would be limited. The more significant risk is that increased uncertainty could cause a tightening in eurozone credit markets and a eurozone recession.

Such a recession could cause risk aversion to increase and eurozone interest rates to fall. Both would contribute to USD strength. USD appreciation tends to weigh on EM as a whole, but we view Turkey as being particularly vulnerable.

A eurozone recession is not, at this stage, our baseline scenario, but we will be monitoring this risk and have put on a partial hedge by going short EUR/USD or GBP/USD, depending on mandate.

The direct impact

It is extremely difficult to estimate the near-term economic impact of the UK referendum, but it is easy to see how increased uncertainty could dampen investment and weigh on sentiment. There is a significant risk that the UK economy falls into a recession starting in H2 2016, and the important question from our perspective is the likely impact this might have on EM.

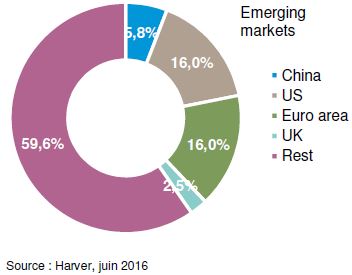

The first point to stress is that EM’s limited direct exposure. As Chart 1 shows, only 2.5% of EM exports go to the UK (rising to 5.6% for Central Europe). A decline in UK demand would be a mild headwind to emerging markets, but it is likely to be swamped by other factors.

Chart 1. Share in EM exports

The indirect impact

In our view a far more significant risk would be contagion via financial channels. Eurozone banks have been hit by negative interest rates and the potential tightening of bank regulations (Basel IV), and even before the UK referendum the EURO STOXX Banks index was down 35% from a year ago. Since the referendum, the index has fallen an additional 23%.

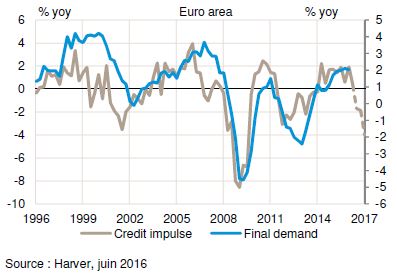

Chart 2. Credit impulse and GDP growth

This is a concern as banks shares have historically been an excellent indicator of future credit growth (Chart 2). If this relationship continues to hold, even partially, the impact on eurozone demand growth could be severe. If credit growth falls to -1% by the end of Q1 2017, the credit impulse will evolve in the manner shown in Chart 3. Clearly, this would plunge the region into recession.

Chart 3. EM private sector debt ratio

In all likelihood the bank regulation proposals will be watered down, and governments could recapitalise banks if capital adequacy looks likely to prove a drag on credit growth. As a result, a eurozone recession is not our baseline scenario. Nevertheless, we will be monitoring the risks. An important indicator to watch for will be the ECB bank lending survey released in late July.

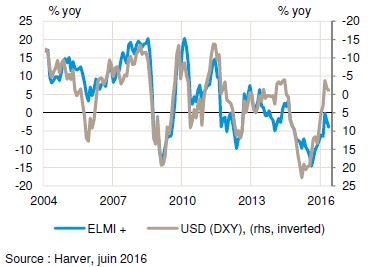

Chart 4. EM FX and the USD

A recession in the eurozone would have a direct impact on EM growth because, unlike the UK, it is a very significant trading partner for EM. In addition, it would likely cause risk aversion to increase, and eurozone interest rates to decline. Both developments would contribute to USD strength, and an environment of USD appreciation has generally been a challenging one for EM FX (Chart 4).

Risks to Turkey

While these developments would be negative for the asset class as a whole, Turkey might be most vulnerable. The eurozone and the UK are both extremely important trading partners for Turkey.

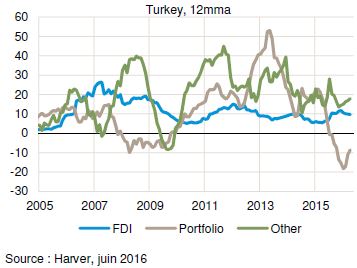

Chart 5. Turkey capital flows

Turkey also tends to run fairly large current account deficits. Portfolio inflows into Turkey have tended to be volatile, but to-date FDI and bank lending inflows have been relatively stable (Chart 5).

If credit conditions in the eurozone tighten, then loans to Turkey are likely to be an early victim. If risk aversion has increased and portfolio capital flows to developed markets, then Turkey’s balance of payments could come under pressure. The high levels of foreign currency debt in the country would mean that FX weakness could give rise to corporate default.

Conclusions

In our view EM fundamentals have improved materially over the past three years, and a turn in the credit cycle could cause EM growth to pick up by the end of 2016. However, we cannot ignore the possible risks associated with the UK referendum. If eurozone credit conditions tighten, the impact could be negative for EM, and particularly difficult for Turkey. At this point we have partially hedged these risks by going short EUR/USD and by underweighting Central Europe (because of correlation with the euro, not because of trade effect). If tighter conditions become more likely, we would shift to being more defensively positioned.