Following our article on banks’ Q1 2020 results, second quarter results have confirmed that Covid-19 is an earnings story rather than a balance sheet story. With greater visibility on the macro outlook and with many issuers having frontloaded Covid-19 related impacts, we believe the sector has reached the inflection point as the bulk of the negative hit has been taken. From a credit perspective, the resilient solvency of the financial sector and its ability to absorb negative effects from Covid-19 through earnings remains the cornerstone of our bullish view on the subordinated debt of financials. Regulators also share the view, with recent European Central Bank (ECB) analysis emphasising the resilience of the sector during this real life stress test.

Second quarter bank earnings - bondholder friendly

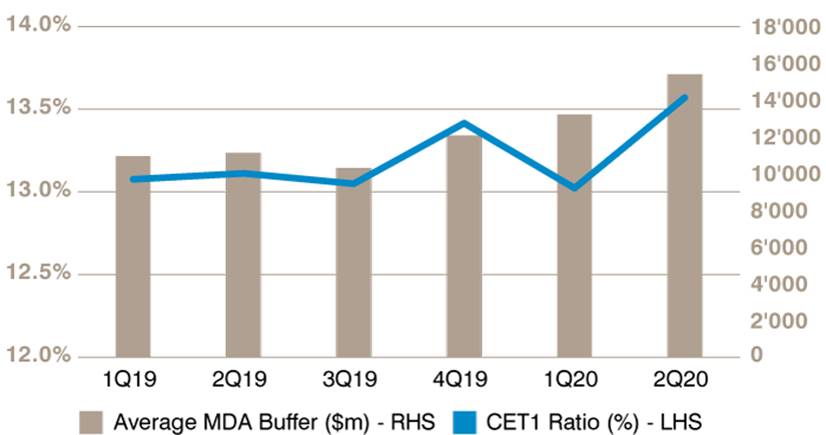

There is no doubt that from a pure earnings perspective, second quarter results followed the trend of first quarter results in being challenging. Pressure on interest margins, elevated loan loss provisions, one-off goodwill impairments have all led to pressure on headline earnings, only offset for certain banks by another record quarter of corporate and investment banking (CIB) revenues. Away from eye watering headlines in the press, the big positive beat was indisputably on capital. We have kept the sample [1] of banks used in Charts 1 and 2 unchanged from our last article; Chart 1 shows that both common equity tier one (CET1) capital ratios have recovered, and excess capital continues to grow.

While bank capital positions declined in Q1 due to risk-weighted asset inflation, Q2 was marked by a further round of regulatory easing and reduced headwinds from client activity that led to a recovery of CET1 ratios to pre-Covid-19 levels. Combined with cuts to capital requirements during the first quarter, excess capital has continued to increase. As an example, Barclays’ excess capital increased from GBP 4 billion as at December 2019 to GBP 10 billion in June 2020 as both CET1 increased and requirements were eased during the first half.

Chart 1: Bank capital positions remain resilient

- Source: Atlanticomnium, bank reports, see footnote data as at 17 August 2020. For illustrative purposes only.

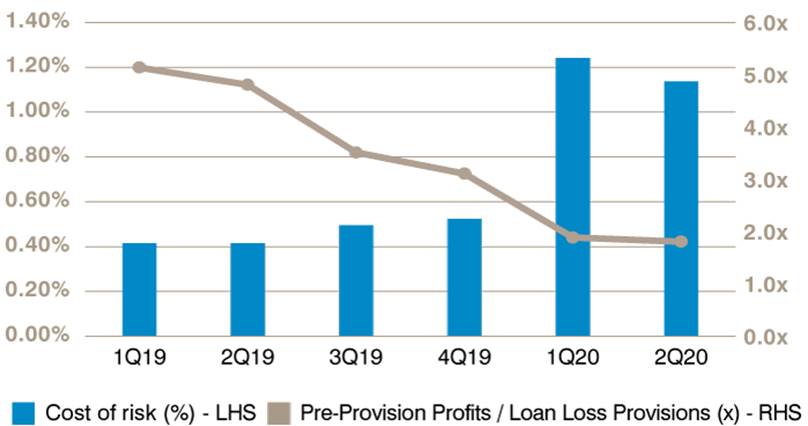

Loan loss provisions (LLPs) remained in focus as banks further adjusted their macroeconomic expectations and topped up provisions for sectors impacted by Covid-19. Cost of risk (loan loss provisions as a percentage of loans) only slightly declined from Q1 2020 levels to around 1.1% on an annualised basis, which remains elevated. Nevertheless, on aggregate, bank pre-provision profits (first line of defence) remain sufficient to absorb LLPs without impairing excess capital positions. Moreover, guidance for full year LLPs suggests that banks frontloaded Covid-19 impacts in Q1 and Q2 (covering more than half of full year provisioning needs), and therefore headwinds should alleviate going into the second half of the year. While inputs (GDP, unemployment) varied on a bank-by-bank basis, on balance, assumptions used were consistent with official forecasts and market consensus, providing comfort in provisioning numbers and bank guidance.

Chart 2: Earnings buffer provides first line of defence to absorb elevated loan loss provisions

- Source: Atlanticomnium, bank reports, see footnote, data as at 17 August 2020. For illustrative purposes only.

ECB vulnerability analysis shows banks’ ability to withstand real life stress tests

In parallel, the ECB has conducted its vulnerability analysis, modelling the potential impact of the Covid-19 pandemic on bank capital positions. The central scenario (most likely to occur according to the ECB) assumes a drop of 8.7% in Eurozone GDP in 2020 and a slow recovery until the end of 2022. In this case, bank solvency positions are expected to remain strong at 12.6% – a 1.9% drop over FY 2020-2022 compared to the baseline level of 14.5%, and hence with a significant buffer over requirements.

The analysis assumes around EUR 200 billion of loan loss provisions and overall EUR 300 billion of losses (including credit market and operational risk) over a three-year horizon which is fully absorbed by banks’ pre-provision profits. Should the situation deteriorate, European banks have in excess of EUR 350 billion worth of excess capital that can be used to absorb further unexpected losses. This is a strong message from the ECB on the resilience of the European banking sector.

Resilient first half earnings from insurers, despite pockets of weakness

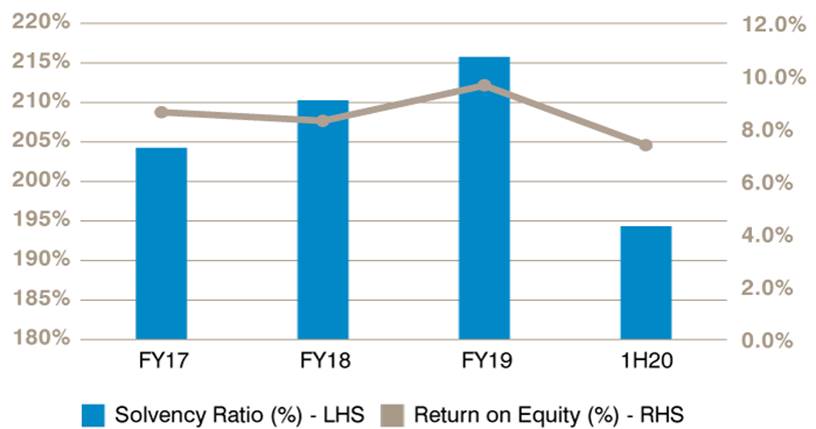

Insurers reported first half 2020 results (typically insurance firms report semi-annually rather than quarterly), which also demonstrated the resilience of the sector. Average solvency of the sector has declined compared to FY 2019 but remains at strong levels, just shy of 200% (down from around 215% in FY 2019) – or two times requirements, see Chart 3. The decline is mostly attributable to market impacts, namely lower interest rates as well as the decline in risk assets (equities, credit, etc).

Looking at the sector’s earnings, the average return on equity declined from close to 10% to slightly above 7% in the first half of year, reflecting the lesser impact of Covid-19 on insurers’ business models compared to banks. Several non-life business lines were heavily impacted, mainly business interruptions and event cancellations, as well as second order effects such as increased mortality also impacted life insurers, albeit of a lower magnitude. This led to some commercial non-life insurers or reinsurers taking larger hits than retail-focused players or diversified insurers. However, on balance, the industry’s profitability levels remain resilient in challenging market conditions.

Chart 3: Solvency positions of insurers strong at around two times requirements

- Source: Atlanticomnium, insurance company reports [1], see footnote data as at 17 August 2020. For illustrative purposes only. [1] Sample includes, M&G Plc, Generali, Aegon, Allianz, CNP, AXA, Phoenix, Scor, Aviva, Achmea, Ageas, Intesa Vita, Credit Agricole Assurances. Unipol Gruppo. Legal & General, Just Group, NN Group, Direct Line, Talanx, Munich Re, RSA Insurance Group, Admiral Group, Royal London. For illustrative purposes only.

Outlook for the second half – the light at the end of the tunnel

After a challenging first half of the year, both banks and insurers have taken steps to frontload the impact of Covid-19 which has led to downward pressure on profitability, with banks more impacted than insurers. While we believe the second half of the year is likely to remain challenging from an earnings perspective, we anticipate the pressure should gradually alleviate as the inflection point has been reached. More importantly, solvency of both European banks and insurers sector remains rock solid, providing strong protection for bondholders from coupon and principal risk on subordinated debt. As the latter is the key driver for subordinated bondholders, this remains supportive for the asset class where valuations continue to be attractive, in our view. We believe the ECB’s vulnerability analysis provides another layer of comfort for bondholders.