In November and December 2018, equity markets had fallen because of the accumulation of concerns about the US economic cycle: the prospect of an overly rapid monetary tightening by the Fed, the Government shutdown (partial shutdown of the US federal Government), the trade war between the United States and China and the sharp decline in oil prices (the United States has become the world’s largest producer of crude oil recently). A recession in the US had become imminent in the eyes of many market participants. However, the markets had finally rebounded in late December thanks to the dissipation of fears on each of these topics: Presidents Xi and Trump entered into a truce in the trade war on December 1 before intensifying their negotiations, OPEC+ countries agreed on December 6 to lower their output, Fed Chairman Jerome Powell said on January 4 that the Fed would be "patient" and attentive to market developments. Finally, the longest shutdown in US history ended on January 25. As a result, most of the risks to the economy seemed to have dissipated or were in the process of dissipating at the beginning of the year, which kicked off a strong market rally that lasted four months.

The dissipation of pessimism has masked the slowdown in the US economy

In the first part of 2019, the easing of the risks and of an undoubtedly exaggerated pessimism masked a fundamental phenomenon: the slowdown of the US economy. The negative effect on growth of fed funds hikes usually materializes with an average lag of 18 months, but the Fed raised its key rates three times in 2017 and four times in 2018, the negative effects of which will materialize in full in 2019 and 2020. Moreover, the effects of the massive tax cuts of 2018 began to fade, especially since these were offset from February 2018 by tariff hikes - which factually are tax hikes- decided by Donald Trump, in a context where companies have preserved their margins by passing on cost increases to consumers.

While economic indicators sent contradictory signals until a few weeks ago, they are now converging (in the wrong direction):

- ISM surveys have returned to their lowest levels since the election of Donald Trump,

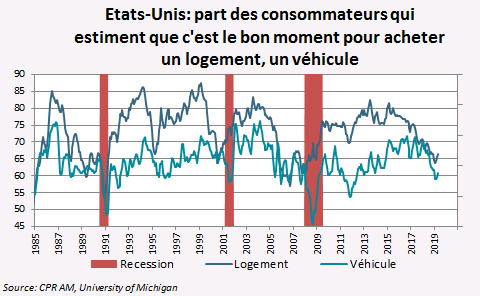

- University of Michigan surveys show fewer and fewer US households believe that is the right time to buy a house, a vehicle, or even durable household goods, particularly because they now estimate that these goods are too expensive,

- Credit conditions have begun to tighten for credit cards, a form of consumer credit used by the most vulnerable households. In addition, the demand for this type of credit has tended to fall over the last quarters while the default rate on credit cards has tended to increase. Incidentally, one of the dangers of a flat or even inverted yield curve is to see banks tightening credit conditions on other types of credit,

- The capacity utilization rate has decreased every month over the last five months,

- The labor market is showing signs of slowdown. Job creation and wage growth, which had been very dynamic in 2018, slowed significantly in 2019, illustrating that companies are more anxious about the economic outlook,

- In Q1 2019, domestic demand (household consumption and private investment) experienced its weakest growth since Q2 2015 (+ 1.3% quarter on quarter in annualized terms) and profits of financial companies fell by 3.5% (and even 4.4% for non-financial companies), unseen since Q4 2015.

To make matters worse, the beginning of 2019 (and particularly the month of May) was marked by a historically high number of tornadoes.

Obviously, not everything is somber. The service sector is more resilient than the manufacturing sector, which is directly affected by tariff hikes. Moreover, the fall in long-term interest rates has stimulated demand for mortgage loans, but unfortunately not in proportions that would allow residential investment to contribute positively to growth in a very significant way. Real estate prices continue to rise but are in deceleration compared to previous years.

Finally, the context of the US economy in 2019 is not unlike that of 2007, that is to say, a period of economic slowdown that preceded the recession of 2008/2009.

A multifront trade war

All it took was a tweet from Donald Trump on May 5 for doubts to come back. Through it, the US President announced that trade negotiations with China were not progressing fast enough according to him and that he was resuming his policy of tariff hikes on Chinese products: as of May 10, the raise of tariffs on $200 bn of imports of Chinese products rose from 10 to 25 percentage points (in total, $250 bn of imports of Chinese products were therefore overtaxed by 25 percentage points compared to the pre-Trump era). Some estimates circulated at the time indicated that this measure alone was one of the largest tax hikes taken in the US in recent decades. Worse still, Donald Trump threatened to tax imports of Chinese products that had been spared so far ($325 bn) but also to tax all imports of Mexican products (about $350 bn), on the grounds that Mexico would not do enough to stop the flow of migrants from Central America (the number of people apprehended at the Mexican border reached a 13-year high in May).

With regard to the Sino-US issue, it appears that trade negotiations could take much longer than expected, or even years, and that the risk is now that the confrontation changes in nature. Indeed, the two superpowers are opposed on several issues (North Korea, Iran, Venezuela).

Moreover, whatever Donald Trump’s decisions on tariffs on imports of Chinese, Mexican and European products, US companies and households are now facing unprecedented tax instability, depending on the moods and strategies of a single man. The Republican Party, Donald Trump’s own side, is also questioning the possibility of disavowing him on the subject... which would tarnish the launch of his re-election campaign.

A number of estimates have circulated about the cost of the trade war for the American consumer. Just before the threat of over-taxation of imports of Mexican products, the New York Fed estimated that the tariff hikes decided in 2018 and 2019 would cost $ 1235 per year per household.

Finally, the trade war exacerbates the US dollar’s strength. The announcement of tariff hikes for Chinese and Mexican products led respectively to a depreciation of the renminbi and the Mexican peso against the dollar. In the end, the effective exchange rate of the dollar (trade-weighted dollar) is at the highest level of the past two decades, which will weigh on growth and can potentially fuel the trade war on other fronts (the fall in the price of some imports may reinforce imbalances).

Towards a new round of global monetary easing

The last six months have seen a radical shift in monetary policy expectations. While the fixed-income markets anticipated in early November two fed funds hikes in 2019, they expected now up to four rate cuts by the end of 2020. Jerome Powell and Richard Clarida, the president and vice-president of the Board of Governors, have already indicated that the door was open for rate cuts if the trade war affected US growth. Moreover, a new round of monetary easing seems to begin at the global level: while no central bank of developed countries had lowered its key rates since October 2016, the New Zealand and Australian central banks cut rates in May and June respectively.

That said, since monetary policy has already acted as a stabilizer at the beginning of the year and interest rate markets are already anticipating a significant easing, equity markets will now face a decisive moment when it is the fundamental factors that will determine the trend.