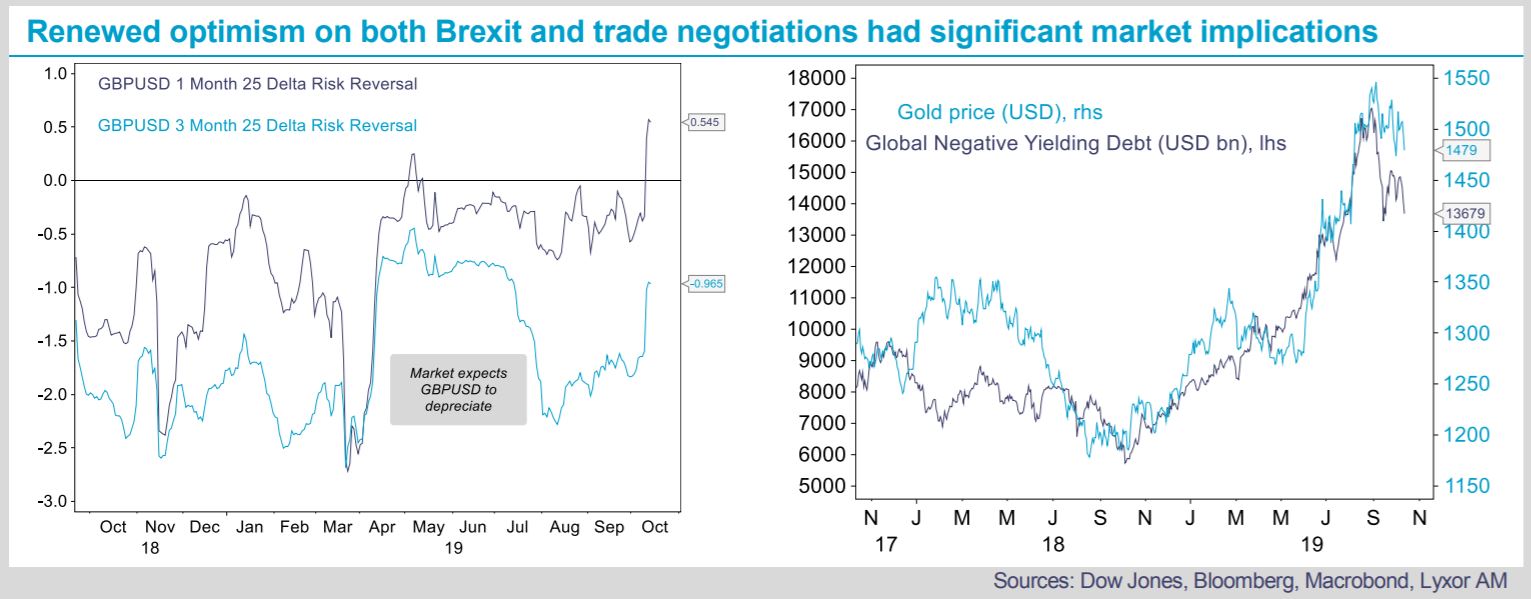

Progress in trade talks between the U.S. and China and in Brexit negotiations knocked down safe assets last week. Bond yields rose in most developed countries and gold prices fell, as the stance on both thorny issues reversed and turned positive. In FX markets, the EUR and the GBP appreciated while the JPY and the CHF, which are typical safe havens, depreciated vs. USD.

The reversal is likely to have negative consequences on CTA strategies, which have sizeable long positions on fixed income and gold. Their long positioning on the USD (vs. the EUR and the GBP in particular) has also been caught on the wrong side. Nonetheless, this may be partially offset by their long positioning on equities, which has benefitted from the easing of the geopolitical risk premium. Meanwhile, the impact on Global Macro strategies is likely to be positive.

Several blue-chip systematic strategies maintain short positions in fixed income, and the rebound in equity markets should also be supportive. Yet, the USD depreciation should partially offset such gains. Global Macro strategies are notoriously heterogeneous and can have an opposite positioning on a given theme. Although they do not take explicit positions on geopolitical issues, their portfolio is implicitly exposed to this risk factor and varies significantly according to the strategy. This is the reason why we frequently argue that investing in Global Macro strategies is more a bottom up than a top down exercise.

Concurrently, the rebound in EM assets (FX and sovereign credit) will likely be supportive for EM-focused Global Macro strategies on which our stance has been constructive (O/W). Our stance on Discretionary and Systematic Macro strategies is unchanged, at Neutral, but with a positive bias at present.

What lies ahead? Hopes of an easing of trade tensions have regularly been dashed in recent quarters. Will this time be different? Our view is that a trace truce is likely, but a broad trade deal is unlikely in the near term. This is nonetheless enough to lift bond yields and depress safe assets in FX and commodity markets.

In the space of alternative strategies, back in July we suggested to diversify CTAs with Global Macro strategies and we reiterate that view.