Getting out of Europe

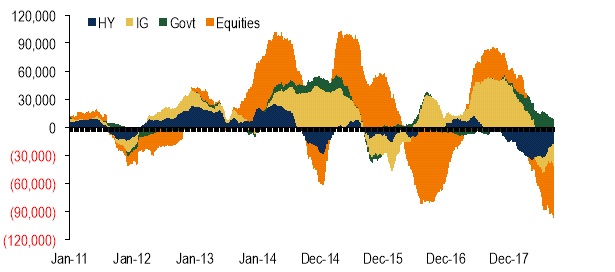

It has been a non-stop outflow trend from Europe it seems. Chart 1 below highlights that over the past 26 weeks almost $90bn has left European risk assets (IG, HY, Govies and equities). Last week’s inflow in equities and HY was short-lived, high grade funds continued with sizable outflows and govies barely saw any new money coming in.

Rate differentials across the globe are shifting flows away from low yielding assets. Note the significant shift of assets out of euro credit to dollar credit over the past months on the back of dollar strength.

Over the past week…

High grade funds recorded another sizable outflow last week. It seems that there is no respite after a week of record outflows (more here). High yield funds flow flipped back to negative, erasing the inflows seen over the previous two weeks. Looking into the domicile breakdown (chart 13), Global and European-focused funds suffered the most, while US-focused funds flows were almost flat.

Government bond funds recorded another inflow last week; the third in a row. But we note that this inflow was the smallest over that period, and a quarter of last week’s one. All in all, Fixed Income funds recorded a sizable outflow at the same pace to that of last week’s, mainly driven by the outflow from the high-grade pocket.

Last week’s inflow in European equity funds was short lived, as the sector lost AUM this week.

Chart 1: Out of Europe (Sum of 26 week cumulative flow, $mn )

- Source: BofA Merrill Lynch Global Research, EPFR

Global EM debt funds recorded another outflow last week; tripling the magnitude w-o-w. The asset class has suffered from 17 weeks of outflows over the past 21 weeks, amid significant stress in EM FX land. Commodity funds recorded another outflow.

On the duration front, all buckets have been recording outflows. The majority of the outflow was on the belly of the curve. Outflows from IG funds, were heavily skewed to mid-term and to a lesser extent short and long-term funds.