Bow to the OAT!

We continue to think that Euro IG spreads look too tight for the prevailing level of policy uncertainty. But we feel that risk premiums on corporate bonds will rise once the ECB slow down their QE buying from April. In the interim, the upcoming French elections are becoming a preoccupation for the credit market. Credit markets seem to be reacting to French government bond moves almost tick-for-tick now: the 1m correlation between iTraxx Main and 10yr OAT spreads is currently 85%.

French elections - the "biggest" event ever?

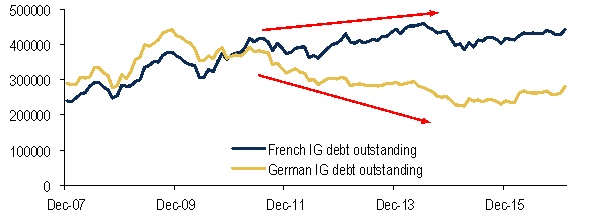

The sheer quantum of French IG debt means that the French elections are of systemic importance for the credit market. There is currently €410bn of French IG debt, more than the amount of IG bank bonds that existed at the start of ’07. What has caused France to become such a dominant part of the IG market (23%)? In part, German credits’ defensiveness. From 2011 to 2014, German credits deleveraged materially, shrinking the stock of German bonds by a third, and thus magnifying the growth of French credit. But in a world where "the street" is smaller, hedging such vast sums of French risk becomes virtually impossible. Even if the ECB bought only French corporates going forward, we estimate it would take them 25 weeks to help investors shift their bonds.

Further to travel in the sell-off we think

So far, French IG credits have widened 6bp since early Jan. With first round voting still 10 weeks away, short-covering is capping the underperformance. But as a reference point, Italian high-grade credits widened over 35bp into last year’s referendum, with the real sell-off starting 5 weeks before the vote. Even still, French credits have been richening lately versus French sovereigns, and 10+yr French corps now look especially tight, we think. While our economists point out the many hurdles to Marine Le Pen’s more dramatic proposals (redenomination, EU referendum), for French credits, we see a roughly 60:40 split between bonds governed under domestic law and those under foreign law.

The world of relative value

To guide investors over the next few weeks, tables 1 and 2 provide lots of relative value context for French credits, including the biggest outperformers and underperformers.

The size of German IG debt shrank by a third between the end of 2009 and the end of 2014