We believe now is a good time to ready bond portfolios for reflation: improving growth, wage gains and higher inflation. We see global reflation running further in 2017 and spurring a modest rise in global bond yields.

Consumer confidence in selected economies, 2003-2016

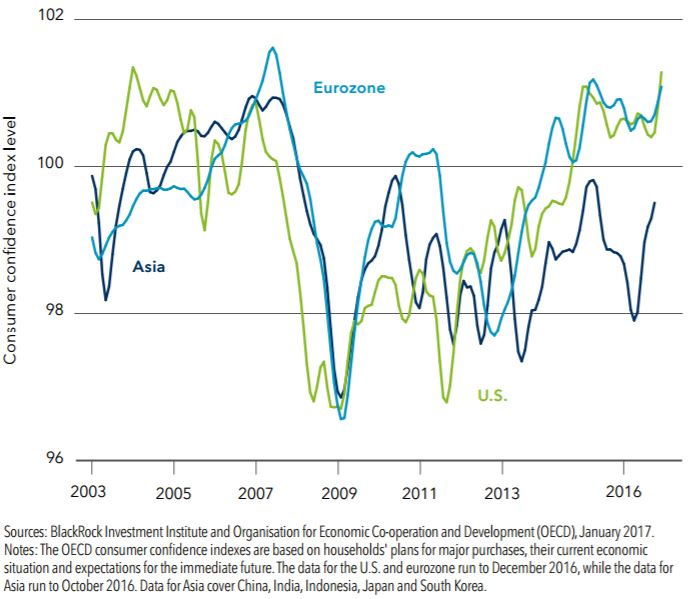

Consumers are gaining confidence, as the chart shows, possibly awakening animal

spirits. The synchronized nature of this global cyclical upswing makes it different

from previous false dawns. The key to our macro outlook: stronger confidence

needs to start translating into higher consumption and investment.

Consumers are gaining confidence, as the chart shows, possibly awakening animal

spirits. The synchronized nature of this global cyclical upswing makes it different

from previous false dawns. The key to our macro outlook: stronger confidence

needs to start translating into higher consumption and investment.

Our fixed income base case

The rise of U.S. wage growth last month to its highest annual rate since 2009 suggests the reflationary phase of this economic cycle has finally arrived. This economic backdrop was reinforced after Donald Trump’s surprise presidential victory opened the way for potentially game-changing tax and regulatory reforms. How and when any reforms are implemented are key to the market outlook this year.

Our base case: Moderately improving U.S. and global growth accompanied by tame inflation will lead to gradually rising longterm bond yields. We see U.S. yields remaining below historical averages, with further rises likely in line with Federal Reserve rate increases. A risk to bonds would be the Fed pressing ahead faster than our expected pace of two to three rate rises this year.

We advocate holding Treasury Inflation-Protected Securities (TIPS) instead of nominal bonds, favor shortening interest rate exposure and suggest owning more corporate credit. We prefer higher-quality investment-grade issues as well as financial paper in both Europe (Tier 1) and the U.S. (bank preferreds). Key elections in France and Germany and the possibility of decreasing monetary policy support create potential for higher yields in the eurozone, particularly in peripheral countries. Global reflation should be positive for emerging market economies, yet the potential fallout from a stronger U.S. dollar keeps us cautiously selective.