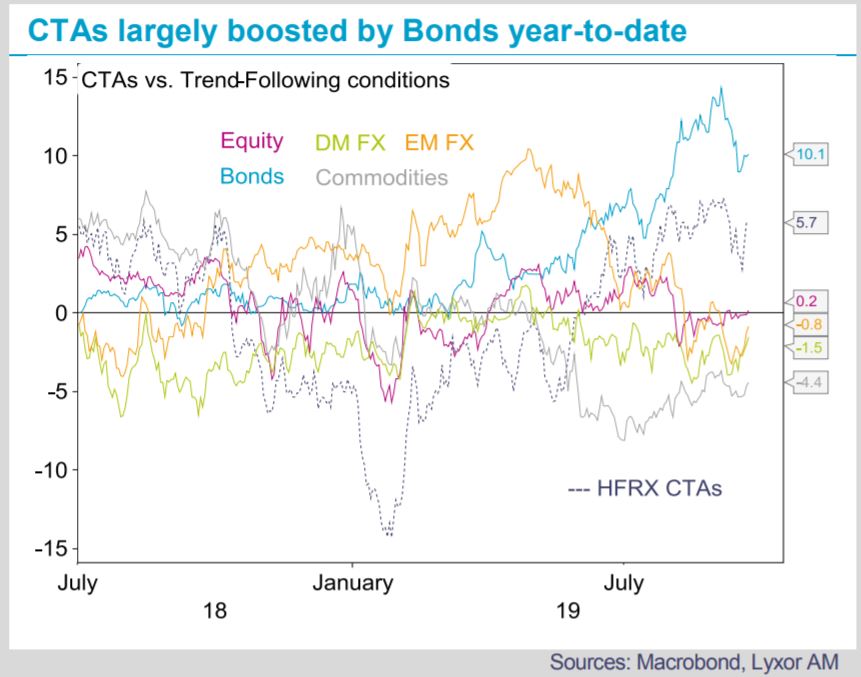

Timing CTAs is notoriously challenging. Monitoring their exposures provides a useful picture but has rarely been a reliable allocation method. They enjoyed an impressive rally this year, mainly supported by their long bond positions, which fueled high CTAs returns’ auto-correlations. Returns might prove less trendy going forward. Over the last two weeks they gave back some of their gains, hit by a notable rotation in govies. They remain long bonds (they shaved off their U.S. positions), moderately long dollar and equities, and they reinforced their long gold vs. short energy, base metals and soft futures. Their sensitivities to thematic baskets emphasizes that they are implicitly positioned for a gradual economic slowdown, persisting Chinese economic pressure, more monetary accommodation (especially in the US), and no pick-up in inflation.

Analyzing trend-following conditions has historically been a more effective approach. Large and broad reversals are the main CTAs’ enemies. To a lesser extent, periods of poor directionality are also adverse, leading to streams of small unprofitable positions. As of today, trend-following conditions are contrasted in our view. On the bright side, a number of ageing trends has just been reset, paving the way for better market directionality once the current rotations have washed out. Witness the few assets still showing an over-stretched pulse. Also, cross-asset dispersion normalized while we see only few cases of unstainable anomalies in cross-asset correlations. We observe similar patterns from a macro standpoint, with the recent convergence in our thematic baskets (tracking growth, inflation, monetary policies implied pricing etc.) also pointing to a lesser risk of reversals going forward.

Less positively, trend-following conditions appear increasingly driven by speculative rather than macro factors. The trade war truce earlier this year was followed by a brutal escalation, with hopes for a pause now building up again. These swings have been increasingly impactful for the global economy and monetary policies, and on markets. Relying on trend-following conditions analysis when non-macro factors dictate volatility regimes can be treacherous. We remain of the view that allocators might be better off with a core allocation to the strategy, for at least four reasons illustrated on the following page:

First, CTAs prove to be the most profitable in elevated and sustainably high volatility phases, typically observed early and late in the cycle, and in particular during economic recessions. See their positive correlation with volatility at these junctures.

Second, they bring diversification in portfolios. They are negatively or very little correlated to most other hedge fund strategies.

Third, they provide access in a liquid way to smaller market segments, in particular in agricultural, metals, and assets of smaller countries that a majority of investors would not cover.

Finally, CTAs optimize portfolio allocation in the long-run. A core holding in basic equity/bond portfolios tend to reduce volatility while slightly improving returns.