Despite colossal headwinds related to trade tensions, the Brexit deadlock and the manufacturing recession, asset prices have been incredibly buoyant so far this year. Equities are recovering from the August drawdown and are approaching late-July record levels. The asset class could deliver the highest yearly returns since 2013 (MSCI World +18% year-to-date). Meanwhile, global bond benchmarks are on track to deliver their best year since 2000 (Barclays Global Aggregate +8.8% year-to-date).

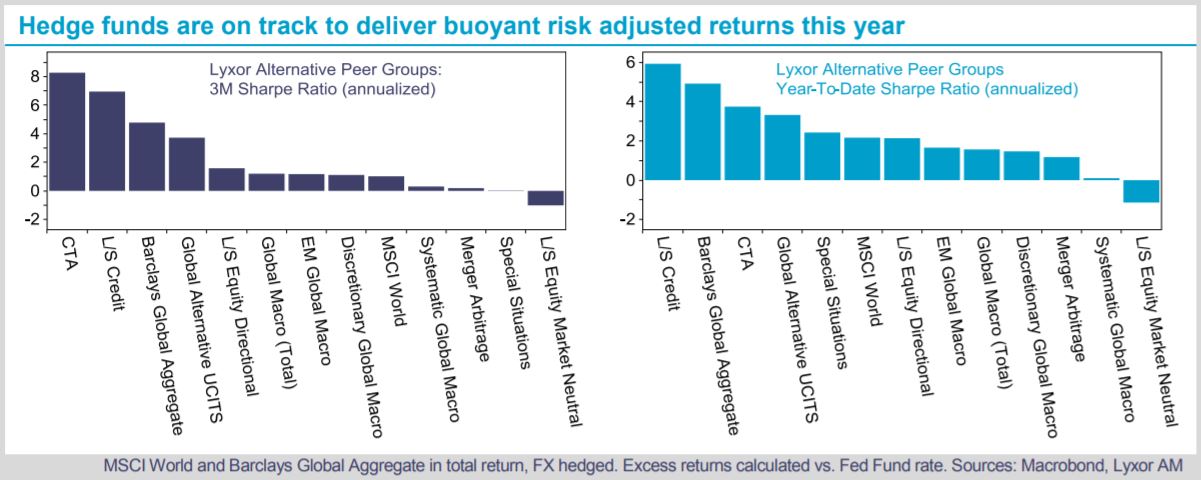

In this context, hedge funds are also posting robust returns. The Lyxor Global Alternative UCITS Peer Group was flat in August, leaving year-to-date returns close to +5% in USD terms. Performance in recent months was led by CTAs, which delivered impressive returns (+3.7% in August; +16.2% year-to-date as of September 3rd). Considering the higher volatility of CTAs, the picture on a risk adjusted basis is slightly different with L/S Credit leading the pack. It has an annualized Sharpe ratio of 6 so far this year (vs. 3.3 for our Global Peer Group).

As we are head into Q4 2019, we turn more defensive. U.S. trade tariffs on USD 250bn of annual imports from China are set to increase to 30% from 25% starting October 1st.. Manufacturing new orders continue to signal a contraction and the Michigan survey signals an erosion in consumer confidence which might hurt private consumption, the last engine of U.S. growth. In our view, the risks are highly asymmetric.

In this context, hedge funds might help with dealing with the ongoing uncertainty.

Merger Arbitrage and Market Neutral L/S are attractive despite their underperformance so far this year. We also reiterate our O/W stance on L/S Credit and EM Global Macro, as a stance in favor of carry strategies in a low bond yield environment. Meanwhile, high beta strategies such as Directional L/S Equity (U/W) and Special Situations (N) are likely to feel the brunt of the equity market volatility. With regards to CTA and Global Macro (N), we are reluctant to add to the former after the recent rally. Yet, it provides protection against a reversal in stock prices and/or adverse Brexit developments thanks to short GBPUSD positioning. Finally, within Global Macro, we prefer EM-focused strategies (O/W) to leverage our view that the Fed will materially ease monetary policy in the coming months. We anticipate two rate cuts from the FOMC before year-end (September 18th and December 11th).