Investment « styles » aim to capture risk premia and/or market anomalies that can be seen structurally over long periods. While no formal classification exists, a distinction is traditionally made between four major style families, not only applicable to equities but also to other asset classes: Value, Size, Carry and Momentum (for more details read also Style portfolios, a solution to the conventional asset allocation dilemma?).

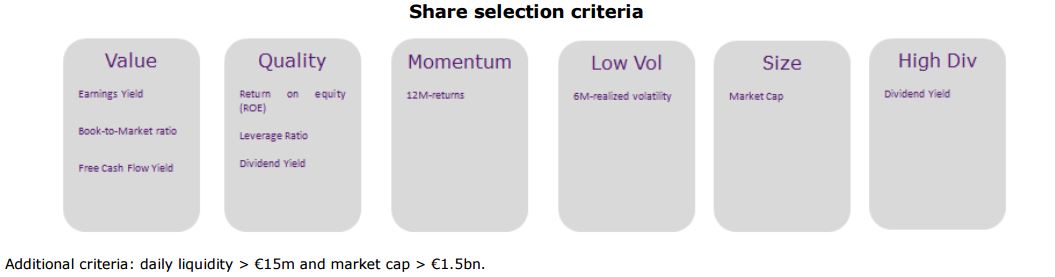

The Value strategy consists in picking assets that seem relatively undervalued, and is therefore based on a measurement of the gap between the fundamental value of the assets and their market price.

The Quality strategy is picking assets on solidity/stability criteria at any price.

The Momentum and Low Vol strategies are exploiting investors’ behavioural biases: the first one picks assets that have performed best over the last 12 months, and the second one, assets that were least volatile over the last 6 months.

The Size strategy is inspired from the work of Fama-French and picks assets with the smallest market caps.

The High Div strategy is a Carry strategy and picks assets offering historically the highest dividends.

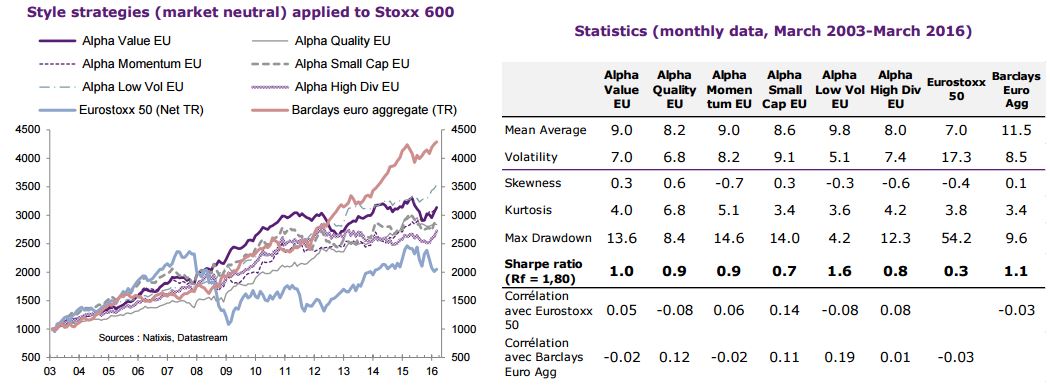

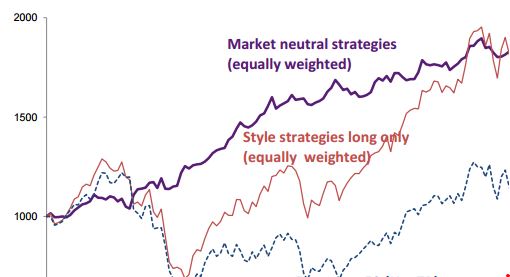

We will focus here on styles in the European equity universe (shares picked in the Stoxx 600). In their long only version (basket of 50 shares picked on the basis of above criteria), these strategies historically outperform their benchmark indices.

With the exception of the Low Vol strategy, the strategies show, in terms of historical volatility, levels equivalent to the traditional European indices, and all of them therefore show higher Sharpe ratios (ranging between 0.6 and 0.9). For some strategies (Momentum, Small Caps and High Div), these performances offset a risk of asymmetry (more negative skewness than the benchmark(s)). Lastly, these Long Only strategies obviously post a high correlation to the market (average beta to the Euro Stoxx 50 ranging from 0.55 to 0.93). In the long term, style strategies outperform their benchmark indices, but keep naturally a high beta to them.

In a second version (« market neutral »), we will neutralize this beta to keep only the premium that is found in these strategies.

We then study « market neutral » strategies consisting of :

- A basket long of 50 shares picked on style criteria,

- Whose beta (calculated on 60-days rolling) is neutralised with short positions in Euro Stoxx 50 futures.

Over the period 2003-2016, the Market Neutral strategies posted a return of 8 to 10% per year for an annualised volatility ranging between 5 and 9%. The Sharpe ratios are therefore very attractive (table below) and comparable to those offered by bonds (Barclays Euro Aggregate index). By construction, the strategies show a low correlation to the equity market. But the attractiveness also lies in the low correlation to the bond market (correlations ranging from 0 to 0.2 to the Barclays Euro Aggregate index).

Style investing in equities seems particularly attractive in a context marked by few opportunities for bond returns, a higher and more uneven equity volatility, and less directionality.

In their long only version applied to equities, these strategies historically outperform their benchmark indices. In their market neutral version, they provide a risk/return profile comparable to bonds, with a low correlation to them, thereby providing an attractive alternative.

We show in particular that for the European case, a welldiversified style portfolio reaches a Sharpe ratio of 0.9 with a positive skewness, a low correlation to the equity and bond market, even in periods of stress/corrections in these markets.