It is crucial to be aware of the risks and have a fundamental understanding of the environment and the challenge you are about to undertake. Ultimately, the risks we take are calculated: I work with the analysts to examine what is ahead of me.

Ellen MacArthur, Foreword to “Adlard Coles’ Heavy Weather Sailing, Peter Bruce”

Ellen MacArthur, Foreword to “Adlard Coles’ Heavy Weather Sailing, Peter Bruce”

2015: INITIALLY SUNNY, TURNED STORMY

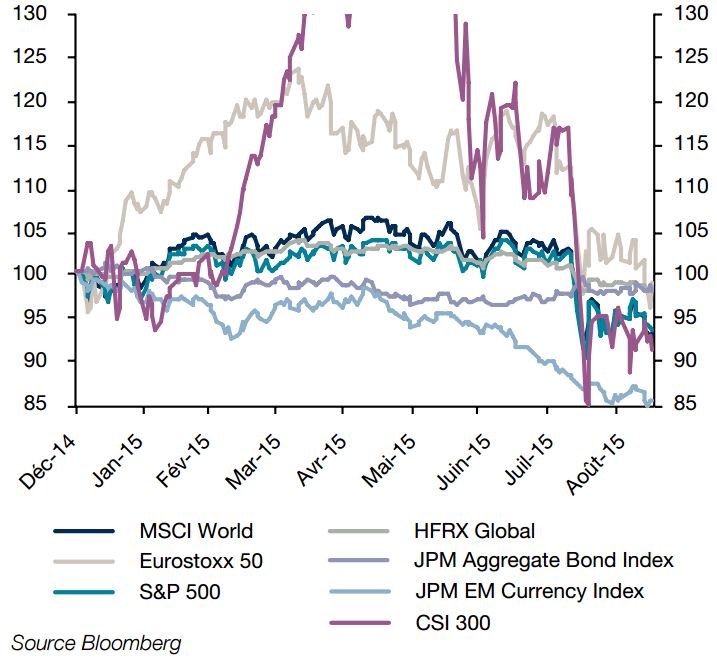

Sailors and mountaineers know it: weather can vary all of a sudden and change a nice family journey into a dangerous endeavour. 2015 started like a beautiful year, blessed by as many as fourteen central banks’ simultaneous efforts to support the economy, with the BoJ and ECB at the forefront. The family picture on 31 March was great: equities and bonds were up during the first quarter; European equities were finally catching up with US equities (up 22%), while Asian stocks were also posting double digit gains, led by China and Japan.

Then, storm clouds gathered. Having bottomed out at 7 bps on 20 April, the 10-year bund yield soared unexpectedly to 98 bps in just a month and a half, generating an unprecedented loss in value of 8.3%. As soon as bond markets stabilised, the Grexit drama came back to haunt investors and policymakers. These clouds dissipated eventually after another marathon all-night summit. But this was a short term relief. Concerns over China’s foreign exchange regime and uncertainties over the Fed’s stance caused unprecedented movements in equity markets in August. Over five trading sessions, between 17 and 24 August, the S&P 500 suffered a 10% drawdown. Digging into the data since 1928 it appears that the probability of such double-digit movements on a weekly basis is below 0.5%. Over the past 50 years, this has only happened on five occasions: October 1987, April 2000, September 2001, October 2008 and August 2015.

The market movement was not limited to stocks. Commodities and emerging market currencies were under pressure but overall, the damage was far more pronounced on equities. The Volatility Index (VIX) jumped from 13% on 17 August to 41% at market close on 24 August. Such a 200% rise in volatility on a weekly basis has not been observed over the last 25 years, i.e. as far back as our data goes (1990). During the global financial crisis and subsequently during the eurozone sovereign crisis, implied volatility as measured by the VIX reached extreme levels but the jump was much

more gradual. The extent of the movement in implied volatility registered in August 2015 was basically beyond what we experienced in the wake of the Lehman fallout.

DESPITE MARKET WORRIES, GLOBAL GROWTH SHOULD MAINTAIN ITSELF

There are fundamental weaknesses that justify market jitters. The economic recovery in Europe and in Japan is weak, large emerging markets ranging from Brazil to China and Russia are experiencing a severe growth deceleration and deflation risks remain significant across the board. Meanwhile, the Federal Reserve will sooner or later have to reverse an unprecedented accommodative stance. The valuation of US equities signals that they are now historically expensive, whether measured by the price-tobook ratio or by the cyclically adjusted price-earnings ratio.

That said, it seems to us that in the medium term, the positive developments on the US recovery front will outweigh the negative implications of the above. Private consumption, which has been robust lately, will continue to receive support from lower oil prices, despite the fact that they will depress capex from commodity sectors. Recent data suggested that the US economy grew 3.7% in the second quarter of 2015, fuelled in particular by private consumption which contributed 2.1 percentage points. Meanwhile, the US labour market is vibrant, with unemployment in August having reached 5.1%, a level that seems out of reach to many European countries. Finally, the real estate market is also upbeat, with existing home sales reaching their pre-recession pace recently (5.6 million units in July).

Overall, the world economy is likely to be supported by buoyant growth conditions in the United States. However, the sharp growth deceleration in emerging markets implies that aggregate demand will likely remain depressed. In this environment we continue to prefer European and Japanese equities. Their valuation remains attractive in relative terms and earnings momentum has recently been supportive. For the reasons listed above we maintain a neutral stance on fixed income: a low growth environment and deflation fears are supportive but valuations are expensive.

STAY INVESTED INTO HEDGE FUNDS AND RISK BUDGETING STRATEGIES

It is precisely because there are bad times that there is a long-term premium in investing into markets. If our scenario is correct, markets will keep on conveying the value generated by the growth of the global economy, possibly in a perturbed manner.

More than ever we believe that combining risk-budgeting and alpha strategies delivers returns in the long run. Riskbudgeting generates sound risk-adjusted returns.

Aside from this Market Premia harvesting, diversified Hedge Fund portfolios contribute to smoothing the ride. Let us review why.

Hedge Fund strategies have proven very resilient this year. Event Driven/ Risk arbitrage have suffered but most Equity L/S or Global Macro managers have managed to smoothen the global turmoil. As of end-September, the Lyxor L/S Equity Broad index is up 1% year to date, while global equity indices are down almost 10%. The HFR Fund of Fund was still positive end of August even if September moves will likely bring it in negative territories. At that date, some Funds of Hedge Funds were displaying positive performances, some of them above 2%, which is quite remarkable in this environment. Alpha strategies have been under pressure over the 6-year market rally. But over the course of 2015, investors have increasingly allocated to such funds due to traditional longonly funds being less attractive in relative terms. Interestingly, inflows into liquid alternatives in 2015 are reaching record levels in Europe, at EUR 50bn between January-August 2015. This confirms, if any proof was needed, the long-term hedging properties of Hedge Funds as long as investors put enough emphasis on due diligence matters.

The short term case for risk budgeting strategies is more involved. They have been roasted by some commentators recently for two reasons: 1) they have contributed to downward market movements; 2) they have posted disappointing performances. Not only risk budgeting has been wrongly charged of exacerbating market movements but we point out the remarkable long-term properties of these strategies.

Certainly risk budgeting strategies can lead the manager to sell despite having a positive outlook on the market. But this is like reducing the sail surface of a boat when the wind picks up. It might prove costly if the wind falls back but might also avoid a very difficult situation if the wind picks up again.

As the VIX soared brutally from 13% on 17 August to 41% on 24 August, some people judged that risk budgeting strategies would have immediately cut their position in the same proportion (by 3) hence worsening the sell-off. In our view, this is very much exaggerated.

First, the worst of the sell-off happened in China where, to the best of our knowledge, the risk-budgeting investment style simply does not exist. Second, if most risk-budgeting managers indeed use volatility as a proxy for risk, they typically use a 3M to 1Y historical volatility and not the VIX.

As an example, between 17 August and 24 August, 6-month volatility of the S&P 500 has moved from 11% to 16% which, while significant, is of a reasonable magnitude. On top of that, the proportion of investors investing with a risk budgeting approach is likely to be low as compared to the value oriented approach, which tends to increase positions when the market falls.

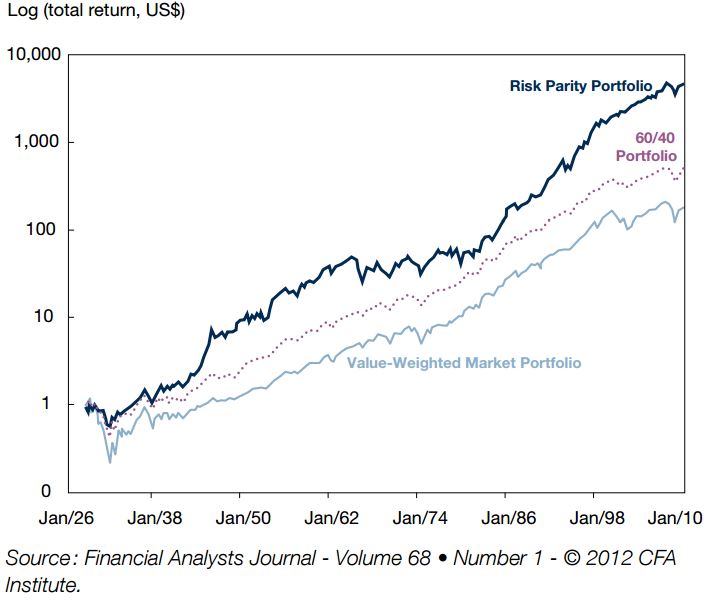

THE RISK PARITY, MARKET, AND 60/40 PORTFOLIOS:

CUMULATIVE RETURNS, 1926-2010 [1]

As far as their performance are concerned, riskbudgeting strategies cannot escape the global market sell-off, particularly when they are long-only. This said, most of them deliver returns above traditional balanced funds since they have reduced gradually their exposure as long as market risk was increasing.

On top of that, the remarkable long-term properties of risk budgeting should be kept in mind. AQR Asness, Frazzini and Pedersen (2012) published a very long-term simulation of a typical risk parity strategy in a article in the Financial Analyst Journal [2].

Interestingly, these simulations show that not only risk parity strategies do extremely well since 1980 but they would have also been quite resilient between 1930 and 1980. Similar results can be found in many textbooks such as the authority on the matter published by T. Roncalli in 2013 [3].

Even if not doing it in a systematic manner, we definitely recommend thinking in terms of risk allocation more than in terms of dollar allocation since this has proven to be and will likely remain much more efficient.