The objective of these funds is to invest mainly in quality short-term instruments, i.e. commercial paper, certificates of deposit, treasury bills and short-term fixed or variable rate bonds near their maturity, hence with little exposure to changes in their value. In Europe, funds are classified into two broad categories, short-term money market funds and regular money market funds, based on their exposure to interest rate, credit and liquidity risks.

![]()

In Europe, the negative low interest rates present a quasi existentialist challenge (which is far from being an isolated instance, fund closures having accelerated in Japan since negative deposit rates were introduced by Bank of Japan). Investors face increasing difficulties earning any return on asset classes that must be the least risky as well as traded in the money market. While prior investments still enable managers to turn in positive performances, redemption values are gradually sinking into negative territory.

Regulations and the tightening of spreads between bank rates and deposit rates have created an environment that has adverse consequences for liquidity. This excess liquidity could weigh further on short-term issuance by banks. This situation could encourage managers to increase maturity past the horizons set out in the guidelines, invest in lesser quality instruments and increase concentration in selected issuers in order to earn the few extra basis points needed to maintain minimum returns. In this context, investors are being forced to move out of short-term funds into longer term and, hence, more flexible regular funds.

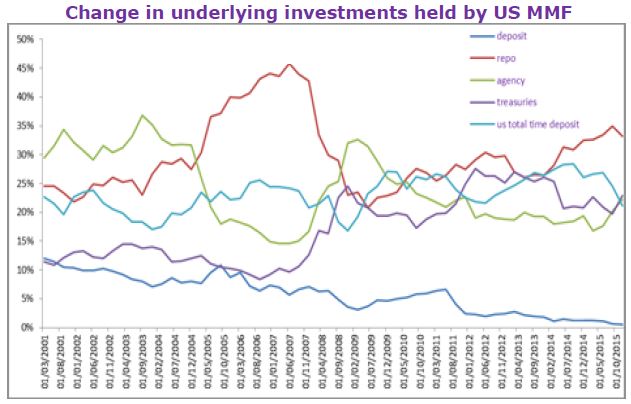

Managers have broadened the range of underlying investments and their asset allocation, as underlined by the changes in underlying investments held by US money market funds, which face similar constraints. Managers have moved out of US Treasuries in favour of repos and certificates of deposit.

Everywhere, and Europe is far from being an exception, money market funds have increased the “barbell’isation” of their portfolios: on the one hand, funds invest at the most distant permitted maturity and, on the other hand, they multiply investments in short term repo is order for average maturity to meet regulatory requirements. These strategies are obviously susceptible of affecting portfolio sensitivity and risk profile.

The adverse market conditions are compounded by concerns that there could be changes in the regulatory framework. The European Commission has been working on a European framework for money market funds, which could result in the introduction this year of new rules concerning liquidity, issuer concentration, internal ratings, holding limits and redemption reserves.

The new law on the cash accounts of depositaries has come as a rude blow for UCITS. These accounts, which were remunerated at 0%, will be reset from 1 May 2016 at -0.40%, in line with European Central Bank’s deposit rate. This will create a dissymmetry between managers and investors, who still have the possibility to deposit excess cash in accounts remunerated at 0%.

On the other hand, changes in banking regulations could, to a lesser extent, favour the development of money market funds: prudential regulations will encourage ownership of assets eligible to the different liquidity ratios, i.e. LCR and NSFR. Certain institutional investors - insurers, mutual insurers and public undertakings, even corporates - will have no choice but to invest in money market funds as part of their cash management. Money market funds address this constraint, providing banks with daily access to the cash resources while meeting regulatory requirements.

The still relatively attractive remuneration compared with deposits, banking regulation and investor constraints suggest that investments in money market funds will not dry up in the US or in Europe, as underlined by recent change in assets under management (see left-hand chart below).

Flow momentum appears to be correlated very much to risk aversion, money market funds seemingly acting as a vehicle for managing changes in cash positions in reaction to this factor. In the US, outflows peaked between 2009 and 2011, following the 2008 crisis. In Europe, cash inflows reached nearly EUR 48bn in 2015. It will be observed that investors have not modified their strategy, continuing to invest in money market funds, in turn maintaining performances between -0.05% and 0.02%, way above Eonia.

Since 2011, it will be observed that investors react instantly to any event by divesting money market holdings. Examples abound, the Eurozone sovereign debt crisis in August 2011 being a case in point. Cash inflows/outflows do track our risk perception index. The latest data published reveals that there were cash outflows in December 2015, but that there were cash inflows in the next few weeks. In a context of abundant liquidity, money market funds enable investors to react rapidly to deteriorating market conditions by moving in and out.

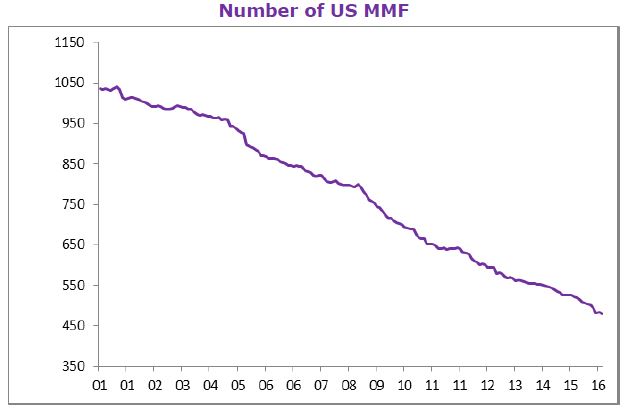

Nevertheless, pressures on the regulatory front and on returns are likely to lead to a consolidation of the MMF industry: the failure to recoup certain costs due to the low returns is denting managers’ revenues and earnings. Compliance and operational costs induced by the changes in the regulatory framework will increase the cost structure of money market funds. The focus is already on achieving economies of scale, leading to the closure of an increasing number of small and medium-sized funds and the development of larger funds (which have a broader customer base).

Bottom-line

NIRP and the tightening of prudential regulations since the 2008 crisis pointed to a decline of money market funds. However, these vehicles still address the needs of certain investors. The rate for the European Central Bank’s deposit facility is one factor, but so are the regulatory constraints facing the different industry players. Institutional investors account for a large part of the assets managed by money market funds. These investors need to deposit most of their cash positions in assets available on a daily basis. The two main options are bank deposits and money market funds. So long as money market funds remain relatively attractive compared with bank deposits, they are not staring at extinction. While the MMF industry is undergoing a consolidation, it is proving resilient, having adapted to the range of assets available for investment without departing drastically from its business model. In other words, money market funds have put up an unexpectedly spirited resistance to the exceptional circumstances created by NIRP and will probably stay the distance so long as these exceptional circumstances are not here to stay.