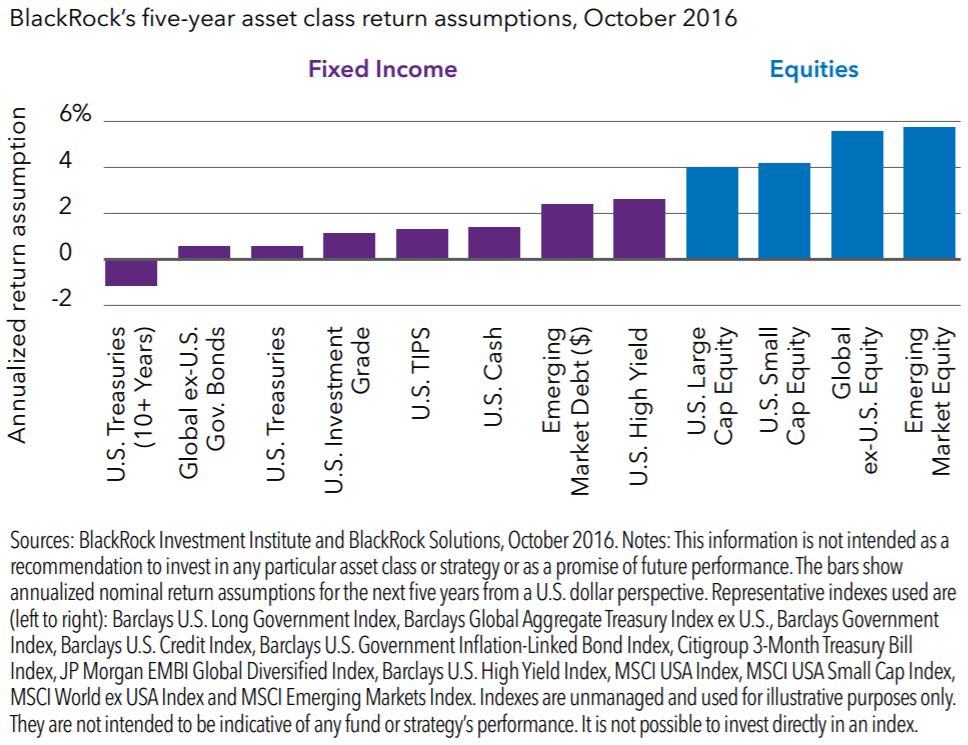

Many investors have favored perceived safer assets in recent years, but we believe a reflationary environment is taking shape that will reward selective risk taking. Structural economic changes should keep bond yields low for many years, in our view. This should make risk assets such as emerging market (EM) bonds and global equities relatively more attractive. See the chart above.

Taking risk where it’s most rewarded

Big structural changes to the world economy — think aging populations and weak productivity growth — along with supply/demand imbalances should keep government bond yields low for many years. This represents a sea change for how investors need to consider diversifying portfolios. For example, we see a global portfolio consisting of 60% equities and 40% bonds generating a nominal annual return of just 3% in U.S. dollar terms over the next five years before fees, based on our asset return assumptions.

With the global economy showing some signs of a reflationary tilt as U.S. growth accelerates, investors aren’t being compensated for the risks tied to many perceived safer assets, we believe. We expect annual returns on government bonds to be near zero and even potentially negative on a five-year horizon.

The takeaway: Investors should focus on assets where they are being better rewarded for the risks entailed, we believe. High valuations and low growth do imply lower returns for risk assets versus history, but risk assets’ returns are still attractive compared to those of safe havens. We see equities overall as relatively attractive in a low-yield world. Other assets offering attractive risk premiums include EM debt. O

ver the long term, we see more scope for investors to take advantage of the extra risk premiums available in alternative investments, such as real estate and private equity.