Policy uncertainty was recently been at the highest levels we have ever seen. However spreads have remained relatively tight and volatility was close to record low levels. The cash bond market is still trading in a tight range in the past couple of months and implied vols across a wide range of asset classes up to recently were close to the lows.

According to Bank of America Merrill Lynch analysts, report shows that this is a direct result of improving trends across a number of macro indicators, valuation attractiveness and surprise factors.

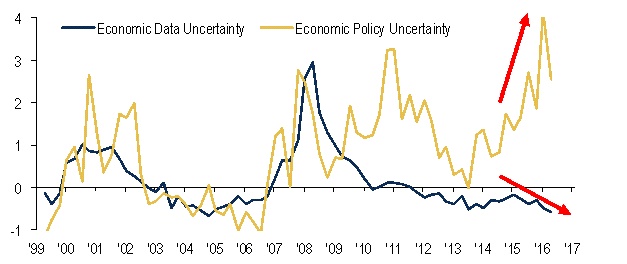

- Source: BofA Merrill Lynch Global Research, Bloomberg; z-score analysis

Why vols and spreads are low?

Why are vols and spreads staying relatively low, despite the rise in policy uncertainty and populism? We think the reason is improving trends across a plethora of macro and risk valuation indicators. An improvement in trend happened not only on a level basis, but we also note a decline in the volatility and dispersion that these metrics exhibit.

Assessing economic certainty

In order to assess the level of economic data uncertainty we pool a broad range of macroeconomic, sentiment and valuation indicators. We employ a z-score approach to assess the trends seen across these metrics. It is a blend of metrics that capture changes on trends on the level, the volatility and the dispersion (if applicable) of these indicators. We find that this pool of metrics exhibits a significant level of correlation to the trends seen in credit spreads and the trends of the vol market.

Where from here?

We firmly believe that as the QE’s positive backdrop will weaken going forward, credit spreads will likely move wider from here. Implied vols have already started to react so far this month on the back of tapering and rising political risks and are more likely to move higher from here heading to the French elections.