We see reflation ? rising nominal growth, wages and inflation – accelerating globally in 2017, led by the U.S. This theme is central to how we suggest positioning portfolios for the coming year, including our preference for value stocks over bond proxies.

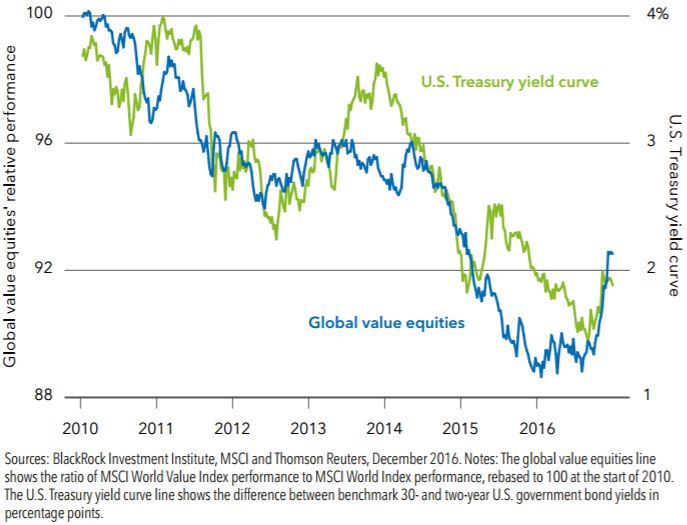

Global value equities’ relative performance and U.S. Treasury yield curve, 2010-2016.

With inflation taking root and growth picking up, we believe bond yields have bottomed, and yield curves are likely to steepen further in 2017. This environment should support reflationary beneficiaries, such as value stocks. Higher long-term rates drove a rotation within equities during the second half of 2016. Reflation contributed to value shares outperforming the broader market, as bond-like equities suffered.

Stocks over bonds

We expect more of this rotation in 2017, and see the stock market beneficiaries of the post-crisis low-rate environment further underperforming over the medium term. We generally prefer stocks over bonds and are optimistic about further upward revisions to earnings estimates. Within equities, we favor U.S. regional banks, selected health care stocks and companies able to expand their dividend payouts over time. Our research suggests dividend growers perform well when inflation drives rates higher.

On a regional basis, we have upgraded our views of Europe to neutral and Japan to overweight. Weaker currencies should support these markets, though we are wary of political, policy and trade risks in the eurozone. We favor emerging market (EM) equities, given structural reforms, improving profitability and low valuations. A sharp rally in the U.S. dollar or significant changes to trade agreements are risks, however. We see earnings growth and further rotation into big sectors such as financials underpinning a U.S. stock market advance in 2017, but we are cautious in the near term after large inflows and new record highs.

Within fixed income, a reflationary outlook challenges longer-term bonds. We favor shorter-duration bonds given their lower sensitivity to rising rates. We see stronger growth supporting credit over government bonds, and we have a long-term preference for inflationlinked securities over nominal debt.