Tactical allocation, which involves buying and selling the right assets at the right time, requires responsive investment decisions and the full use of the discretionary margins available to the fund managers. But these two prerogatives often meet investment biases (direct or indirect) which can severely impair portfolio returns.

For more than 20 years, the teams at CPR AM have developed a robust tactical allocation expertise. This is based on a key principle that is applied daily to our entire portfolio management: asset allocation - and the responsiveness that comes with it - is the only performance driver. As a result, our approach generates marked investment choices while avoiding structural biases. This philosophy extends to all stages of the investment process, from drawing up forecasts to optimising portfolios and selecting investment vehicles.

Avoiding biases as soon as we draw up our forecasts:

Our allocation process is based upon a methodology unique to CPR AM that was developed back in 1997 and is regularly upgraded by our investment and research teams. We call this our ‘probability weighted multi-scenario approach’. Prior to all investment decisions, and during CPR AM’s asset allocation committee, we develop several market scenarios which illustrate different views of the world over a three-month horizon. In doing this, we strive to extend our understanding of risk in order to better anticipate future market trends. Our approach therefore takes into account additional risks (upward and downward) to counter the inherent drawbacks of a single scenario “black or white” view - which ultimately aggravates any forecasting or diversification errors. This process, which includes monthly reviews, generates strong asset allocation decisions with the view to delivering regular outperformance in all market conditions.

Our forecasts are determined on a team basis and cover a wide range of asset classes within a global investment universe. During CPR AM’s asset allocation committee, all members of the team of fund managers discuss their performance forecasts for each asset class and within each scenario. The combination of these “votes” is then reviewed and debated by all attendees. Through these discussions, we eliminate each fund manager’s potential biases (for instance, a preference for his/her own asset class) very early on in the process. Beyond its democratic aspect, this way of working enables all concerned to discuss different points of view. It favours debate between different investment teams (credit and equities, euro and global equity etc.) and improves the consistency of our forecasts.

Improving consistency through modeling:

CPR AM’s balanced investment process is driven by a proprietary asset allocation model. The main data inputs are the forecasts issued by the asset allocation committee. This quantitative model will translate the fund managers’ convictions into a consistent allocation through an optimisation process. This tool, which is designed to be highly flexible, is able to adjust fully to different portfolio constraints. As a result, our model delivers optimal asset allocation for every single fund, based both on the common forecasts and on specific constraints. In this way, portfolio construction for all funds is driven by the same investment principles, and is therefore not subject to the preferences of a given fund manager. In this context, modeling is used as a safeguard that prevents the implementation of structural biases in a given portfolio.

Far from restricting fund managers’ convictions or room for manoeuvre, the use of models helps to implement decisive investment choices in a disciplined and consistent manner.

Between two monthly asset allocation committees, the strategy is reviewed and/or refined on a weekly basis to improve responsiveness. Here too, collegial decision-making is a key factor.

Selecting instruments with care:

At CPR AM, we focus on asset allocation as our main performance driver. The selection of instruments is therefore conducted in a way that reflects our pre-determined asset allocation decisions as closely as possible. We prefer to invest in “pure” instruments that are highly representative of their underlying assets and offer strong liquidity. As a result, we primarily invest in ETFs, tracker funds or simple derivatives (for instance, futures on equity indices). We believe this decision guarantees compliance with allocation choices and prevents the implicit biases that can result from selecting active managers.

Were we to select external funds, the strategy of the chosen fund manager may play against the desired asset allocation and reduce the potential added value.

While we primarily invest in “beta-one” vehicles, we nevertheless pay particular attention to the choice of instruments, bearing in mind that the quality of different index-based instruments may vary. In this respect, our asset allocation team has developed a proprietary tool dedicated to picking ETFs.

From theory to practice:

Of all investment biases, the most prominent is the “natural habitat” bias – the domestic preference which explains why fund managers allocate stronger exposures to their own country/region due to superior knowledge. Within an asset allocation fund, this bias can have a number of consequences: a structurally higher weight in a given geographical area, or a particularly dynamic steering of the portfolio on a given area for no obvious reason.

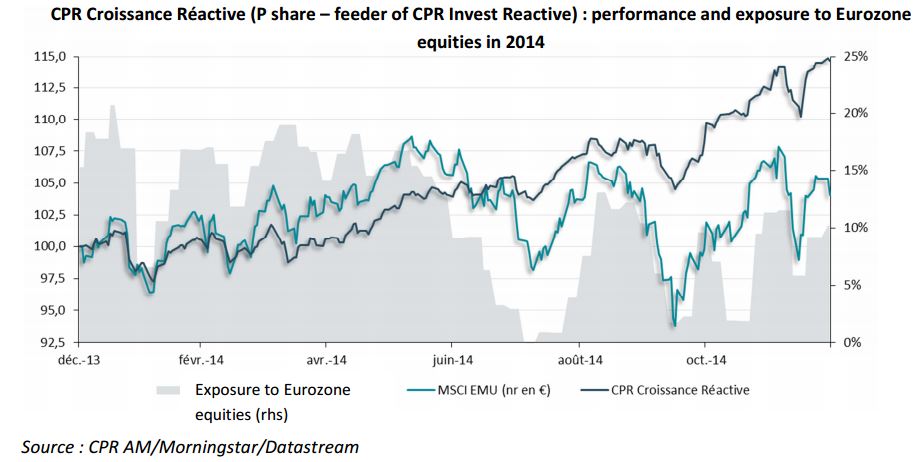

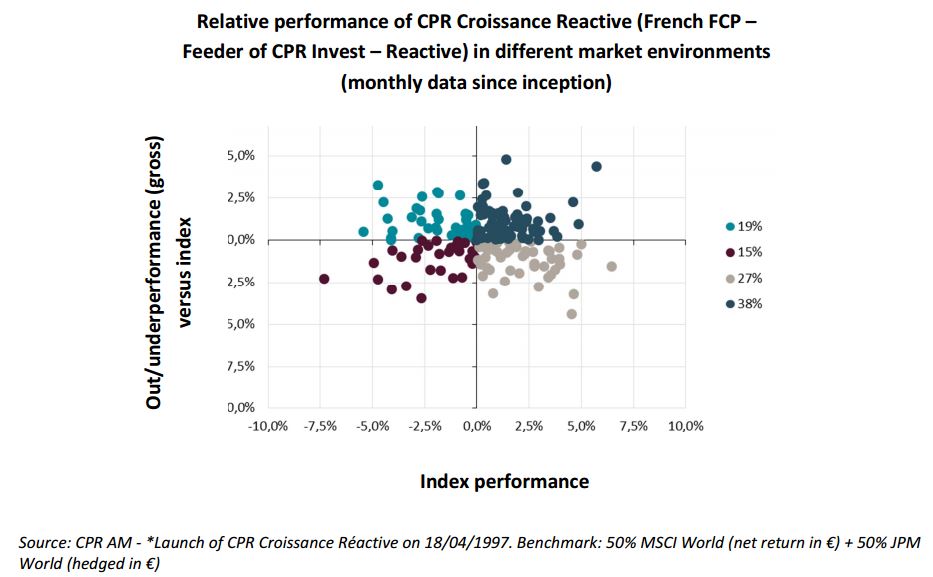

The crisis in the Eurozone provides an interesting case study. The average correlation between flexible balanced funds and the Eurozone equity index is rather surprising. Not only is the correlation very high, but it is also relatively stable over time. CPR AM’s approach has enabled us to limit these biases - and our funds have stood out within their European balanced peer group. Over the past few years, our exposure to the Eurozone has been very dynamic and our portfolios have typically shown stronger resilience to market turmoil (summer 2011, summer 2014, etc.).