Markets last week scrambled to come to terms with two major exogenous shocks: the spread of the COVID-19 virus and the oil price slump. Such shocks to the global economy are rare. Two huge and unconnected shocks coming within days of each other is an unprecedented event.

After initially evaluating the spread of the COVID-19 virus as a temporary earnings disruption, the reaction in financial markets mutated on 12 March into a full-blown search for liquidity.

Volatility rose sharply in equity markets. On 13 March, the S&P 500 index rose by 9.3% after falling by 9.5% the previous day . These were the index’s biggest single-day moves since October 1987.

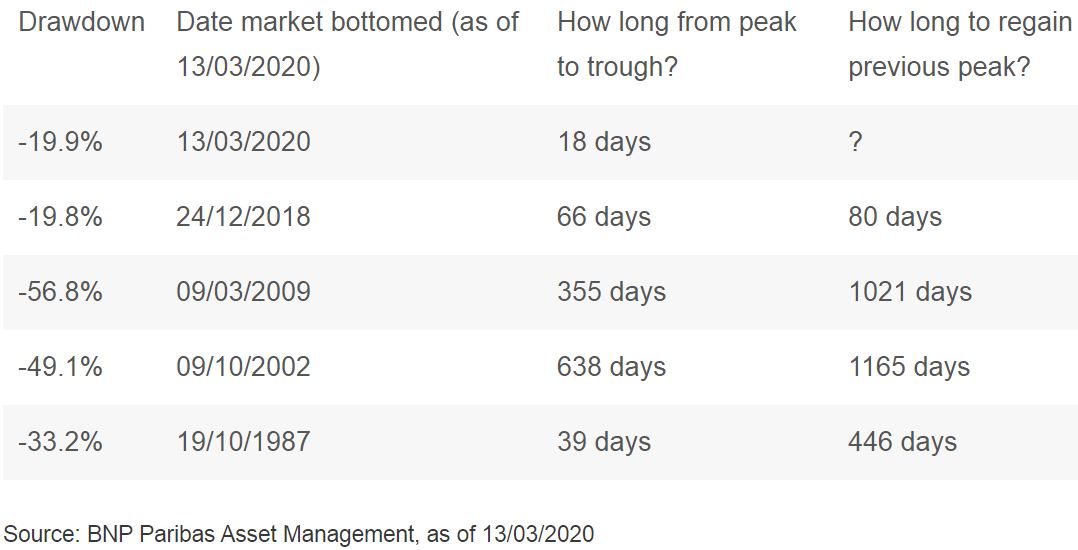

The speed and extent of the sell-off in equity markets last week was unprecedented. Through 13 March the S&P 500 index fell 19.9% from its high in 19 February. Risk premia in credit spreads went from cycle tights to approaching recession levels. There is no precedent for such a rapid sell-off in equity markets (see Exhibit 1 below).

Exhibit 1: S&P 500 drawdowns exceeding (or close to) 20% since 1987

Reviewing recent events in financial markets

Valuations in financial markets have been dislocated by the prospect of an abrupt shutdown of the global economy coupled with an oil price shock.

Markets appear to be repricing for a worst-case scenario, including a global recession, the locking down of large metropolitan areas in multiple countries and a severe credit crunch. At some point, investors will realise that the selloff has gone too far in integrating extreme outcomes and resist it.

As we write on the morning of 16 March, it is becoming clear that the COVID-19 shock will lead in the US, as it already has elsewhere, to a virtual halt in the normal activities of businesses and citizens. In this respect, it cannot be compared either with the 2008-2009 crisis (primarily impacting the financial system and housing markets) or the 1973 oil price shock.

There will be a substantial contraction of economic activity. The intensity and duration of the acute stage of the COVID-19 virus will determine the extent to which economic activity contracts. The subsequent recovery will depend mainly on the recovery in household and business confidence. We expect to see policymakers announcing further measures in coming days to protect the economic system.

On 15 March, the US Federal Reserve (Fed) announced a package of extraordinary policy initiatives including a 1 percentage point reduction in its federal funds rate to 0.00–0.25%. In addition, the Fed will buy another USD 700 billion in assets, bringing its balance sheet up to USD 5 trillions, well above the USD 4.5 trillion at which it peaked at the end of the previous quantitative easing programme.

Central banks are very aware that the negative shock posed by the coronavirus is a health issue and cannot be fixed by easier monetary policy.

Draconian health and fiscal policies are much better tools than monetary policy in addressing the current situation. But, in this emergency, central banks are doing all they can to limit risks to the financial system and preventing the inevitable cash-flow crunch from triggering a financial crisis that would aggravate a recession.

Positioning and strategies for our equity portfolios

It is clear to us that COVID-19 will have a dramatic impact on the global economy and has raised the risk of a global recession. It represents a negative shock to both supply and demand, meaning there is no easy fix for global policymakers.

Financial markets tend to lead the global economy. The best buying opportunities will arise when investors are dispirited, having abandoned all hope. We are mindful that equity markets tend to fall well ahead of recessions and bottom before the consequences on economic activity and employment are apparent.

The unprecedented rapidity with which markets have fallen and the extreme outcomes now being envisaged will inevitably provide opportunities in the coming days. Our objective is to increase holdings in quality stocks with free cash flow and low debt levels.

We anticipate there will be opportunities to acquire quality stocks at attractive valuations. Our teams are working together closely following valuations of those stocks that interest us in the current environment.

Coming into this crisis, our equity portfolios had a pronounced bias to growth and quality over value. We have sought to invest in conservative companies with strong balance sheets. This strategy has proved favourable so far. We are confident it remains appropriate and will continue to generate attractive relative performance.