It’s all about rates

Lower front-end rates have been pivotal to support flows into credit to the detriment of flows into equities. Investors continue to favour short-duration high-grade paper to insulate against steepening of curves, while outflows continue from high duration pockets.

Over the past week…

High grade funds continued on a positive trend for the sixth week in a row; and recorded the highest inflow in three weeks.

High yield funds inflows remained strong for another week, now counting 13 weeks of positive flows. Looking into the domicile breakdown, as charts 13 & 14 show, even though European-focussed funds recorded inflows, the majority of the inflow is concentrated in US and globally-focused funds.

Government bond funds flows went back to negative territory after a brief week of inflows. Money market funds weekly flows were negative for the third week in a row. Overall, fixed income funds flows remained strong and positive for the tenth consecutive week; with more than $30bn over that period.

European equity funds flows on the other hand moved back to negative territory after five weeks of inflows. The outflow from the asset class was the biggest in thirteen weeks.

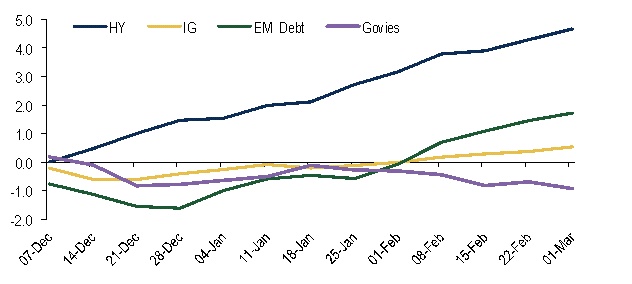

Chart 1: Reaching for yield continues in FI world (cumulative weekly flows, $mn)

Source: EPFR Global, 4wk cumulative flows for IG funds

Source: EPFR Global, 4wk cumulative flows for IG funds

Global EM debt fund flows continued on the positive trend for a fifth week, however we note a weakening of that trend recently. Commodities funds flow remained positive for a seventh week.

On the duration front, strong inflows continued in short-term IG funds for the 11th week in a row. Mid-term funds’ flows turned slightly positive after three weeks of sizable outflows, while flows into long-term funds remained negative for a second week.