Volatility regimes are decisive for most investment approaches, particularly hedge funds. For both top down players (CTAs, Global Macro, FI Sovereign Arb.) and bottom-up strategies (L/S Equity, Event Driven, Credit Arb.), volatility deeply influence their universe and the trendiness of opportunities.

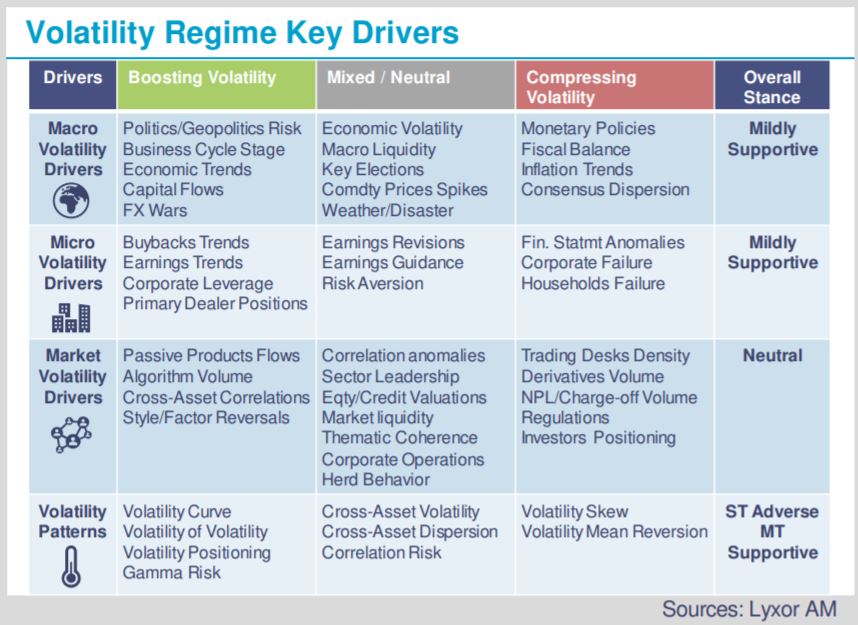

Volatility regimes are determined by a wide set of drivers, which influence one another. It takes a coalition of drivers to alter volatility regimes, requiring a 360° analysis to anticipate volatility trends. Upstream, macro volatility is paced by inflections of the business cycle, dispersion across world economies, swings in monetary policies and credit conditions, as well as by other tail and geopolitical factors. Macro volatility reverberates at a micro level, affecting households and corporate fundamentals. In turn, both households and companies accumulate actual and/or perceived risks and imbalances (through leverage, shifting income/profits, etc.), which finally spread to market volatility. Turning flows are primary movers for market volatility, triggered by changing macro and micro risks as well as by changing market patterns (trading leverage, imbalanced positioning, stretched valuations etc.). However, as volatility became a key input for risk taking (setting leverage and asset allocation targets) and an asset class on its own, volatility has also become its own mover in a circular reference. When direct and indirect short-volatility exposures pile up, investors become vulnerable to non-linear deleveraging and sudden asset re-correlation known as gamma and correlation risks. Several volatility flash crashes came as reminder.

With these drivers in mind, which run upstream to downstream and vice versa, we believe that the days of ultralow volatility (<15 for G3 equities) are behind. Since 2018, factors such as an ageing cycle, multiple geopolitical risks, a global economic deceleration have largely contributed to the rise. Yet, volatility is still a long way from late cycle levels. Massive monetary injections are offsetting some of the above pressures and curb economic volatility. They help keep market volatility in a mean-reverting pattern, witnessed by series of volatility spikes rapidly faded or by a negative volatility auto-correlation. Moreover, volatility is capped by sustained short-volatility flows from direct volatility allocations, as well as risk-premia, risk-parity or volatility-targeting strategies. All in all, mixed volatility drivers (summarized on the table) could keep G3 volatility around 20 for now, but the more short-volatility flows stack up, the closer we get to a high volatility regime. Central banks reaching their limits, the slowing growth of buybacks (which buy equities on weakness and distort valuations) and passive products (which crush dispersion) could also contribute to a structural inflection.

In the meantime, consequences from higher volatility – be it constrained – are emerging in trading and alpha generation conditions. There are evidences of more fundamental discrimination (equity/credit issuers respond more closely to their fundamentals). Equity/credit dispersion is now firmly off from lows back to average.

Ultimately, higher macro volatility would also result in more themes to exploit. As we slowly and steadily march toward a higher volatility regime, bottom-up pickers might be the prime initial beneficiaries, later relayed by top-down strategies.