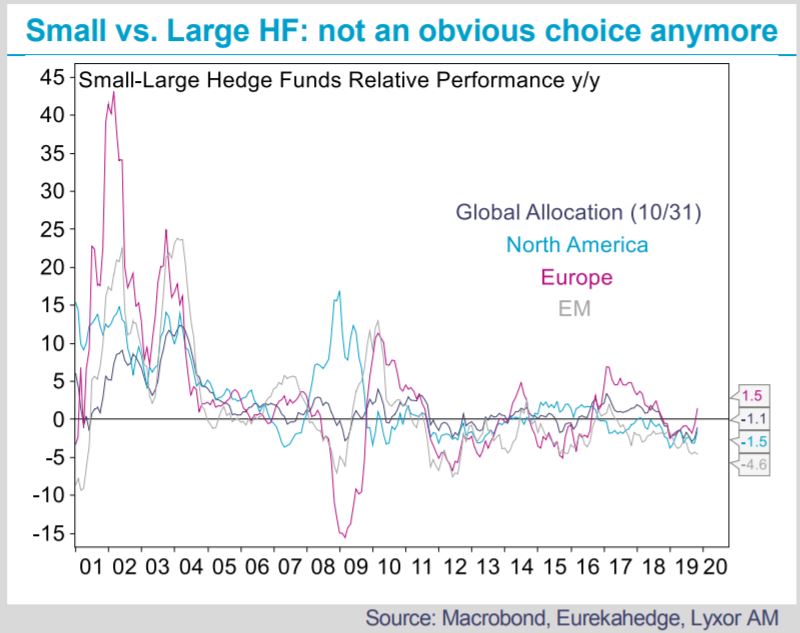

Should alternative portfolios favor smaller, medium, or larger hedge funds? The choice might not be as obvious as before and may be more dependent on the stage of the business cycle. For many years, small hedge funds have steadily outperformed their large peers, sometimes by double digits in the 2000’s. Since the financial crisis, returns between these groups have leveled off, and they share the lead one after the other.

Smaller funds’ flexibility has been a key advantage as they are able to move capital faster. Their reduced impact on market liquidity also allows them to access a wider spectrum of niche and specialized segments. More dependent on variable fees than on management fees, managers bear greater pressure on performance and tend to show more ‘animal spirit’. Moreover, many talented traders within larger firms created their own smaller funds, boosting alpha generation. In contrast, their higher relative fixed costs have become more impactful in recent years, only partially offset by lower investors fees. Finally, smaller fund indices might overstate returns due to survival bias.

The advantages of larger funds have started to be more impactful in recent years. Their larger asset base provides them with negotiating power on execution costs (brokerage and leverage fees in particular), while diluting their fixed costs (such as their administration fees, cost of access to information, research teams, etc.). In a world of lower growth and lower rates, fees and costs have become key performance variables. Size of assets also matters positively in areas such as activism, private equity, primary issuance markets, etc. Additionally, they may be better equipped and staffed to deal with rising regulation/compliance and risk management costs. In a more challenging environment for asset raising and alpha generation, larger funds may have now more arguments and means to attract and retain talents. Apart from the inertia typical of larger structures, their main constraints lie with tighter market access and greater liquidity impact (higher slippage cost, sliced trading execution), both costly for alpha.

Relative advantages and constraints did converge, thus sustainably reducing the performance gap linked to

size. Our analysis suggests that a growing share of the gap (about 2/3) can be explained by the smaller funds’ more aggressive market risks, either through leverage or riskier sectors/country/instrument exposures. Their volatility, also structurally higher, is consistent with market exposures. In short, excess alpha generation from smaller funds shrunk, making their structurally higher beta exposure matter more. As a result, small funds tend to lead in early and mid cycles but lag in late cycles and recessions.

Small funds have underperformed since 2017, in sync with rising uncertainties and decelerating economic growth. Exception to the rule: we find that the lag vs. large funds mostly stemmed from weaker alpha. They regained some the lost ground in recent weeks, mostly due to their relative market risks this time.

While the performance gap between small and large funds shrunk in all regions, global and European small managers kept a slight alpha edge relative to their U.S. and EM peers.

We find that medium sized funds went through similar changes and broadly show median characteristics between those from small and large funds. They might be best fit for those looking for a balanced risk/reward mix.