The strategic positioning of discretionary and systematic managers

The recent strengthening of the debt crisis, coupled with a deteriorating outlook for 2012, is a real puzzle for asset allocators. On the one hand, though equity markets exhibit attractive valuation levels, they are highly affected by both the persistence of the volatility and the macroeconomic concerns. On the other, the absence of firm agreement on resolving the debt crisis in Europe and in the United States increases the pressure on the sovereign ratings and calls into question the very nature of so called "safe assets". This implies growing tensions on the yield curves (especially in France), and consequently on corporate spreads.

In this context, it seems relevant to analyze the strategic options that have recently been implemented by systematic and discretionary managers. To do this, we estimate the dynamic risk structures of the HFRX Macro and HFRX Macro Systematic indices.

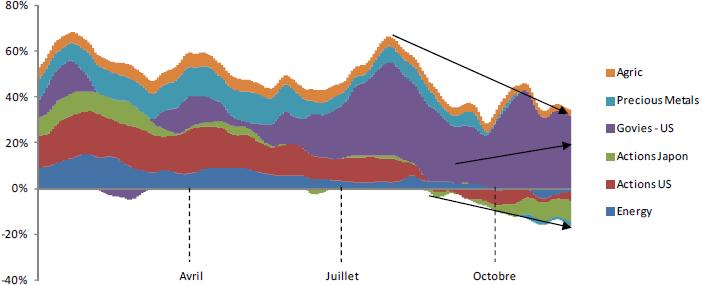

Figure 1 highlights the evolution of the risk structure of the HFRX Global Macro index since the end of July. We observe a significant reduction in equity and commodity exposures (energy, precious metals), in favor of the strengthening of the positions held in US sovereign debt. Since mid-September, developed equity exposures turned negative (beta estimated at -17 %). According to these results, the position of Global Macro managers is firmly defensive, and mainly focused on the traditional asset classes.

- Graphique 1 : structure de risque véhiculée par l’indice HFRX Macro

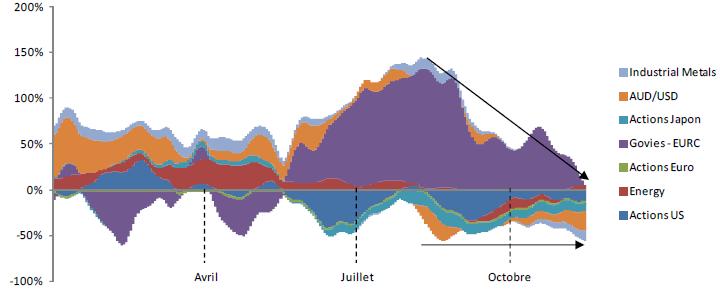

Figure 2 highlights a similar strategic behavior among systematic managers, albeit with some differences. On the one hand, the defensive positioning was initiated in June (short equity market) vs. September for Global Macro funds. On the other hand, with the resurgence of the sovereign debt crisis in August, CTAs significantly reduced their exposure to this asset class (core European debt), to remove it completely today. During this same period, they exhibited net short exposures to commodities (energy, metals) and to commodity currencies (AUD).

- Graphique 2: structure de risque véhiculée par l’indice HFRX Macro Systematic

Finally, the structural analysis of the risk structures of the HFRX Macro and HFRX Macro Systematic indices confirms the bear anticipations discretionary and systematic managers. Global Macro managers explicitly follow defensive strategies: short exposure to equities (around -20%) and long exposure to the US sovereign debt. On their side, CTAs managers are more aggressive: short exposure to equities estimated at -50% and exposure to the core Euro debt decreased to zero, thus calling into question the status of “risk-free asset” of this asset class.