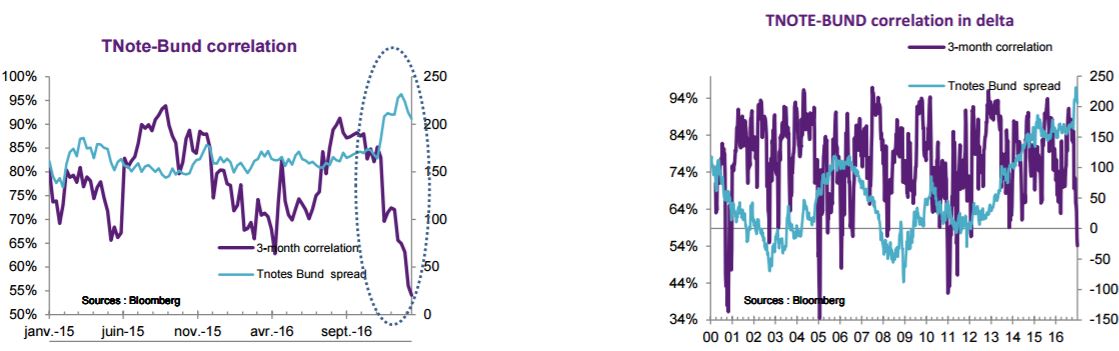

2016 marked a watershed for the sovereign bond market. European bonds underwent a sharp selloff in Q4 2016, this when the year had kicked off on a bullish note that lasted right through to September. The political events in 2016, the outlook for growth and for inflation and monetary policies were the main drivers behind the sea change in sovereign interest rates. There has clearly been a change of regime since the election of Donald Trump.

Currently, correlation between TNote and Bund sits at 54%, which corresponds to the levels observed in 2011, this when the correlation between sovereign rates in the US and Europe had been camping above 80% on average.

To understand how this change of regime came about, we examine below the main determinants for the German Bund and US TNote.

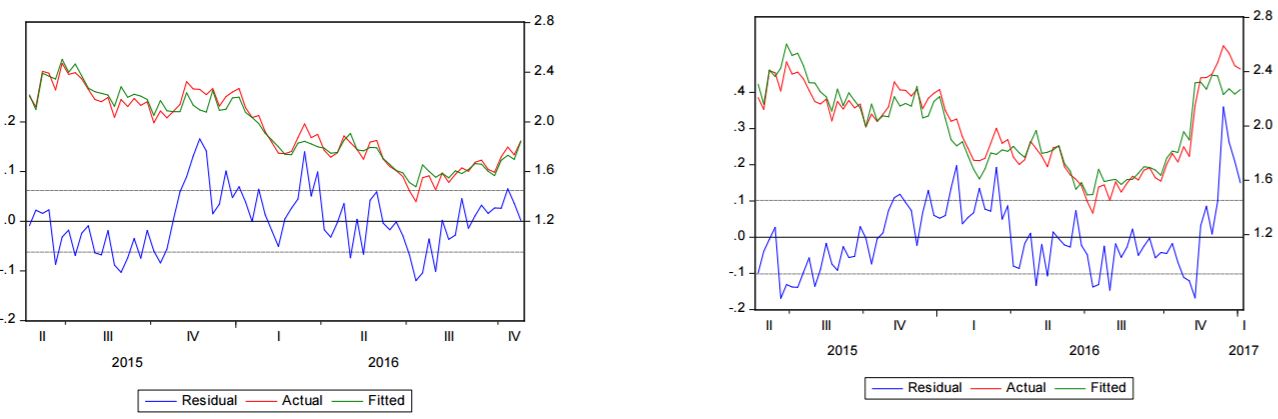

Bund model

Metrics for European interest rates have been influenced mainly by the

uncertainty surrounding the evolution in the ECB’s monetary policy, the

fall in inflation and, more recently, political risks. Liquidity injections have

a direct bearing on short-term interest rates. The decline at the short end

then spreads to long-term interest rates through an integration

mechanism. The model we have constructed confirms that, over the past

two years, Bund’s performance has been driven by three factors: the

ECB’s balance sheet, inflation expectations, and political risks (these risks

being contained in the residues).

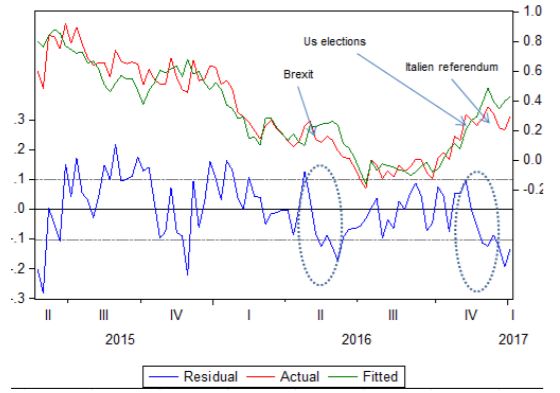

To some extent, interest rate metrics in 2016 would be explained in the case of the US by the evolution in interest rate levels in Europe and by the

improvement in the US economic situation, i.e. growth and inflation expectations, rather than expectations as regards future interest rate levels. The TNote model as a function of Bund and inflation expectations functions correctly from 2015 until November 2016. This ceases to be the case once the

outcome of the US elections is integrated. In other words a new regime has come about in which the TNote takes over from the Bund.

To some extent, interest rate metrics in 2016 would be explained in the case of the US by the evolution in interest rate levels in Europe and by the

improvement in the US economic situation, i.e. growth and inflation expectations, rather than expectations as regards future interest rate levels. The TNote model as a function of Bund and inflation expectations functions correctly from 2015 until November 2016. This ceases to be the case once the

outcome of the US elections is integrated. In other words a new regime has come about in which the TNote takes over from the Bund.

TNote model as a function of Bund and US inflation expectations pre- and post-US elections

Why this brutal change of regime?

The strong correlation observed in 2016 can be explained by investment flow metrics: investors engaged in arbitraging between risk-free assets on both sides of the Atlantic during a period of negative interest rates in the Eurozone. Also there was the fact that quantitative easing (QE) drove domestic investors in the Eurozone to buy foreign bonds, which lessened QE’s impact on Eurozone interest rates. At the same time, the Federal Reserve proved sensitive to the international environment, notably uncertainties arising from the EU referendum in the UK. As a result, the divergence in monetary policies was not the factor of de-correlation it should have been in 2016.

By contrast, the new regime takes on board both the lags in the cycles and the expectations regarding the future trajectory of monetary policy at the respective central banks (even though the prospect of a tapering by the ECB is very much on the cards at the start of 2018).

Since Donald Trump’s election, the rise in interest rates is the telltale sign of the new playing field in the bond markets.

The reasons lie in the domestic political component and a context that is more favourable to inflation, which is being fuelled by the upturn in commodity prices, notably for crude oil. What can be observed is that the political component is not of the same order depending on whether it is external or domestic. In the US, the upturn in inflation and the fiscal stimulus package proposed by Donald Trump (coming when there is full employment) would lead to inflationary pressures on wages and to the appreciation of the US dollar. Reacting to these expectations, the markets have pushed up US interest rates since Donald Trump’s election. This factor has had a greater impact on US Treasuries than the political risks in Europe.

These factors are behind this discontinuity, ushering in a new regime, which could be described as more conventional in that measures and announcements by central banks once again play a decisive role.

Correlation being weak by past standards, the prospect is that it will recover to normative levels, which in turn is favourable to there being greater stability in the TNote-Bund spread in Q1 2017.