Summary

For a few years now, the central banks have had the habit of preparing the financial markets and economies for changes in monetary policy, but the reversal of a seven-year-long ultra-accommodating monetary policy, the Fed’s, is obviously more important than usual. In our opinion, there is no urgency or need to start a real tightening cycle or normalise monetary policy, and this viewpoint is widely shared throughout the financial markets, if forward curves are any indication. The US economy can probably withstand some interest rate increases; the global economy, probably a bit less; and the financial markets (especially emerging ones), less still. This means that the Fed’s message is now absolutely crucial. Misinterpretation of the Fed’s decisions remains a significant risk factor. In all, the Fed will probably make an opening gambit at the next FOMC on 16 December, but it will stay in very gradual mode and, at the most, would tighten by 25 bp per quarter: in this case, the fed funds rate would reach only 1.50% at the end of 2016 (+125 bp compared to today, but there are reasons to believe that the Fed’s rate of tightening will be even slower, with a terminal rate target that is much lower than in previous cycles (less than 3%, far less than what the ‘dots’ suggest). Betting on low long-term rates and a flattening of the US curve still makes just as much sense.

Introduction

At the September FOMC meeting, the Fed decided to leave its rates alone. This is hardly surprising, but everyone agrees it is just a matter of time before the Fed begins to reverse an eight-year, hyper-accommodating interest rate policy. The purpose of this memo is to put the Fed’s very recent decision into perspective and present our forecasts and strategies anew.

Why is the Fed’s next move so critical?

The Fed is has been in easing mode since the financial crisis, and it is gradually coming out of it.

- The Fed stopped its QE programmes gradually during 2014. The announcement that these programmes would be stopped sent the markets into a dive, specifically the emerging markets, which had benefited greatly from the inflow of liquid assets from that unconventional monetary policy. (NB: It is worth mentioning the funds that went to the emerging markets and the market’s decline in 2013 and 2014 with the capital outflows).

- The Fed now wants to move out of the "zero" rate policy, and the fear is that the financial markets will correct downward. Since the 2000s, the central banks have preferred to announce their monetary policy stance in advance to prepare the financial markets, so the Fed issued a message saying that it would begin to raise its key interest rate before the year’s end.

Given the length of the monetary easing cycle and its magnitude, it can be argued that an increase in interest rates has never been so important.

What are the Fed’s projections?

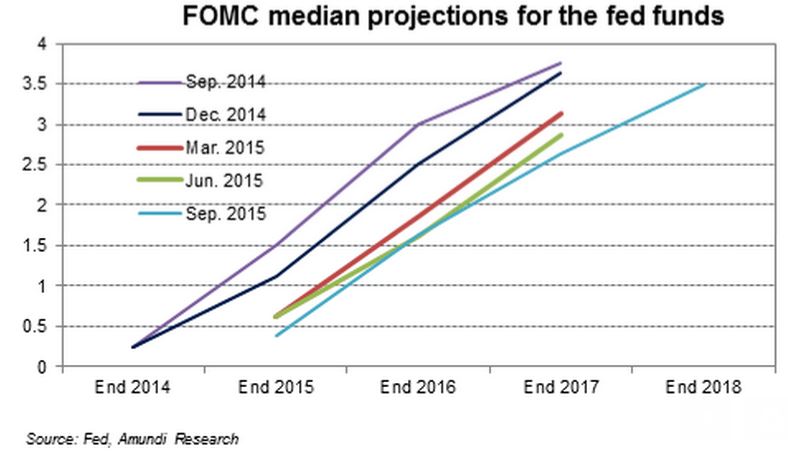

There are clear disagreements among FOMC members. Jeffrey Lacker, the Richmond Fed president, was in favour of a 25 bp rate hike. On the contrary, one member, probably Narayana Kocherlakota, the Minneapolis Fed president, who will vote only in 2017, indicated that he was in favour of negative rates in 2015 and 2016. Once again, the median Fed’s projections (“dots”) have been lowered by the FOMC members. They indicate a hike in 2015, four hikes in 2016, four hikes in 2017 and an end of the tightening cycle in 2018. One has to highlight the fact that the majority of voting members indicated a rate hike in 2015. They will probably continue to lower the dots for 2016, 2017 and 2018.

Three comments should be made here:

- FOMC members are envisaging a much slower and less abrupt tightening cycle than was typical of past tightening cycles;

- The outlook for the terminal fed funds rate is lower than in previous cycles, which is legitimate, because potential growth is now weaker (insufficient investment, weaker gains in productivity, two components that we see as being integral to the "great stagnation" theme). FOMC members have indicated that they only expect a 2% GDP growth on the long-run and they have lowered their growth projections for the whole horizon. For the time being, FOMC members indicate that they expect the terminal rate of the fed funds to be around 3.5%, while the fed funds reached 5.25% during the previous cycle. We believe that the FOMC members are too optimistic on this.

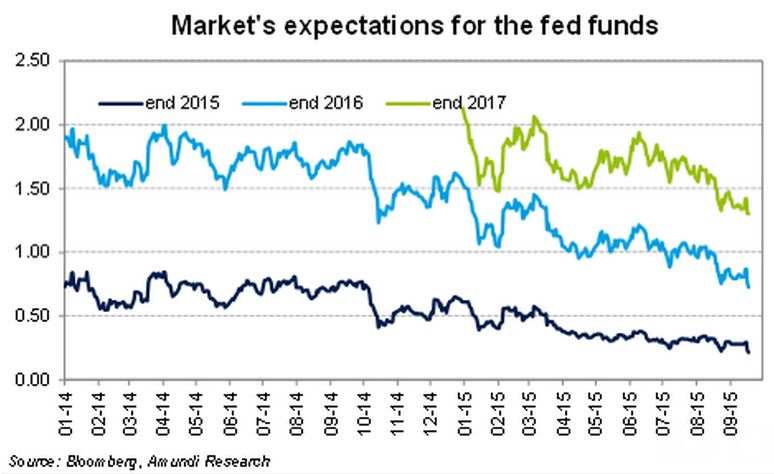

- And, finally, it is important to highlight that the markets are not giving the Fed’s dots any credence, judging that the projections the Fed has supplied are too high. The series of modifications to these projections shows that the FOMC members have tended to converge towards the scenario priced in by the markets. For instance, this is the fourth time in a row that the FOMC members revised downward their fed funds projection for 2017, now at 2.50/2.75%.

What is the Fed’s strategy?

Of course, to get a real sense of what the Fed will do, we have to put ourselves in its place. Not all FOMC members have the same diagnosis of the US economy and their disagreements are now becoming apparent. The downside to this is that there are many governors, and disagreements are already apparent. Some members of the Fed (the doves) want to extend the current accommodating policy, while others (the hawks) want to "normalise" monetary policy. Recently, William Dudley summed up the Fed’s strategy nicely, saying that arguments in favour of raising rates were now "less evident."? Although “International developments have increased the downside risk to US economic growth somewhat," he hopes that the Fed will raise rates by end-2015, adding that in a context of general uncertainty on the markets, such a decision would be reassuring, a sign of confidence in the country’s economy ("I really do hope we can raise interest rates this year… But let’s see how the data unfold before we make statements about when that might occur.").

There are three arguments likely to mitigate the vagaries of monetary tightening:

- The international macroeconomic backdrop: Fears of seeing China collapse further, with an impact on the emerging economies, but also on the developed economies (via their exports) are a significant restriction for the Fed. This is especially true since there is no shortage of deflationary pressures: contraction of global trade in value, stagnation of global trade in volume, falling commodity prices, declining inflationary indices and/or anticipations (see especially the eurozone or Japan), stagnation of wages and industrial prices, etc.

- The US macroeconomic backdrop: Growth is solid, but right now investment and wage growth are not enough for an acceleration in growth at a time when potential growth is itself lower (the Fed’s staff itself sees potential growth at around 1.7%-1.8%). Nonetheless, actual growth is now higher than potential growth, which, all other things being equal, is seen as a "green light" to monetary tightening.

- The market backdrop: It is clear that the market backdrop is not providing the Fed with a comfort zone. Excessive appreciation of the dollar, a rise in long-term rates, and a slump in the stock markets are all negatives for the domestic economy (impact on competitiveness, wealth effect for households). Add to this the many countries (including India) that had already criticised the Fed at the end of its QE, accusing it of failing to take the international backdrop into account.

What are the different scenarios and our forecasts?

There are now three possible scenarios:

Scenario 1: The Fed raises key interest rates at the December FOMC and follows the dots. Without a doubt, this sends a positive message on confidence in the US economy, but the risk is high that the financial markets will think overall conditions (China, emerging economies, current deflationary pressures) do not justify what could appear to be the first phase of a real normalisation of monetary policy. Sending this message or letting the markets believe in a real – and rapid – normalisation will push us to call this strategy a monetary policy error. We do not believe in this scenario, but are not ruling out the risks of misperception of the Fed’s action; far from it.

Probability: low.

Scenario 2: The Fed raises the key interest rate at the December FOMC but strives to explain its prudence and the gradual nature of monetary policy, reiterating how much it believes in the recovery, but also how data-dependent its action will remain and all the hurdles it has to face. In other words, it tries to convince us that it will continue to steer monetary policy and that it is not moving into a ’traditional’ normalisation phase. Remember the last monetary normalisation cycle, when the Fed tightened 17 times, at every FOMC.

Probability: very high.

Scenario 3: The Fed skips its turn for a few FOMC, considering the risks too high. This one will seem justified, if the macroeconomic situation worsens dramatically. For now, growth is real in the developed countries, and even if the emerging pseudo-bloc economies are moving in a negative, even very negative, direction (Russia and Brazil, in particular), the domestic demand of many countries (China and India) remains relatively strong. In such conditions, a monetary tightening before the year’s end, and more tightening spaced out over time, seem much more credible at this moment.

Probability: medium.

In all, we think it is reasonable to bet on an upcoming monetary tightening (next December FOMC): The US economy can fully withstand some interest rate increases; the global economy, probably a bit less; and the financial markets (especially emerging), less still. This means that the Fed’s message is now absolutely critical: How can you back up optimism about the US economy without further worsening the pessimism on the overall backdrop and the financial markets? Such is the Fed’s dilemma. The Fed will stay in very gradual mode and, at the most, would tighten by 25 bp per quarter: in this case, the fed funds rate would reach only 1.50% at the end of 2016 (+125 bp compared to today, but there are reasons to believe that the Fed’s rate of tightening will be even slower, with a terminal rate target that is much lower than in previous cycles (less than 3%, far less than what the ‘dots’ suggest).

What will be the impact on long-term rates and the US rate curve?

In the last two cycles of monetary tightening, Fed communication has been excellent to such an extent that long-term rates remained stable during the monetary normalisation. If we believe in Janet Yellen’s ability to convince the markets that their policy and strategy are appropriate, then we can conclude that US long-term rates are already relatively high, at around 2.20-2.30%, although a short-term overreaction is possible when fed funds are raised. In fact, it is primarily the short portion of the curve that is likely to rise in the coming months, with the curve then flattening. Yield curve should therefore continue to flatten.

It should also to be noted that the Fed will probably continue to reinvest the treasury bonds it holds, which will begin to reach maturity in February 2016. One of the major risks is of the tightening cycle coming to a premature end (see the above-mentioned risks), in which case long-term rates would significantly trend downward.

A progressive tightening policy would please equity markets, because it keeps low rates and favours a lacking element of the recovery: investment.