The index revolution in hedge funds is here!

Well, actually, it arrived fifteen years ago — but some allocators spent the first decade or so fighting it tooth and nail to prevent it from spreading and, in the process, tried their damnedest to convince everyone it couldn’t, wouldn’t or shouldn’t work.

So here we are in 2022: a new generation of wealth managers is embracing factor-based hedge fund replication, an “index-like” strategy that has worked unexpectedly – even remarkably — well. For these forward-looking allocators, it’s a profound improvement over higher cost and riskier options, broadens the toolkit, and has the potential to materially improve client outcomes.

Here’s a quick guide:

Let’s Define “Index”

Everyone knows about hedge fund indices: HFR, EurekaHedge, PivotalPath, Bloomberg, etc. Each can tell you how hedge funds – which are often illiquid, expensive and subject to high minimums – performed last month. Useful as benchmarks, they are unfortunately useless for investment purposes. Imagine trying to invest in your local housing index.

Enter factor-based hedge fund replication. In layman’s terms, it means figuring out how a lot of managers (“hedge funds”) are invested across stocks, bonds, currencies, and commodities (“factors”) and copying them cheaply and efficiently (“replication”). The beauty is that it can work in a UCITS fund with low minimums, daily liquidity, reasonable fees. [1]

The Revolutionaries

In 2006, academic legend Andrew Lo of MIT posited in a paper [2] that statistical risk models, a variant of those developed by Nobel Laureate Bill Sharpe, could determine with striking accuracy how a portfolio of hedge funds was positioned across major asset classes. Simplistically, long small/value and short large/growth drove performance during the dotcom crisis; which stock, not so much. Research by our firm, Goldman Sachs, Credit Suisse, Merrill Lynch, ING and several boutiques confirmed the results. The next step was to transform this “risk model” into an investment product. We launched the first hedge fund vehicle in May 2007, and several firms above soon followed with US mutual funds and eventually UCITS vehicles. The race was on.

The Establishment

There was one minor problem: virtually everyone in the hedge fund establishment hated it. Built on mystique and inaccessibility, the industry bristled at the idea of a cheap robot dog keeping pace with, let alone outracing, a stable of hand-picked, purebred greyhounds.

Even worse, replication raised thorny commercial questions, such as why any rational person would invest in an illiquid fund of hedge funds with 5% all-in fees once presented with a daily liquid version at 1%. So, the establishment circled the wagons.

The stories are quite incredible. A $10 billion fund of funds ran a secret replication program internally, only to shut it down because it “worked too well.” Famous academics (conveniently funded by an investment bank) published intellectually disingenuous critiques – the equivalent of punching a hole in a boat then concluding that it wasn’t seaworthy in the first place. Faced with indisputable evidence that replication had modestly outperformed indices through the GFC, a consulting firm comically claimed the results were irrelevant because they would simply predict the top 7% of funds in advance. Even within the investment banks above, clients were steered to hedge funds where the economics of retrocessions, prime brokerage and other activities dwarfed those of a replication fund. It might even be funny if client dollars weren’t involved.

Why Now?

Simply put, a new generation of allocators is taking over the wealth management space. They grew up in a world where “index” is an efficient and predictable way to get asset class exposure. They’ve watched plenty of hedge fund myths – e.g., the infallible genius — wither in the face of reality.

They recognize that “active” and “passive” can and should co-exist: Millenium, the Sharpe ratio machine, may be a brilliant choice for a few elite clients, but an accessible, liquid, index-like product is far better suited to the other 99%.

Through the lens of model portfolios and long-term client management, they understand the value of predictable, “index-like” results – where the benchmark can be an allocator’s best friend or worst enemy.

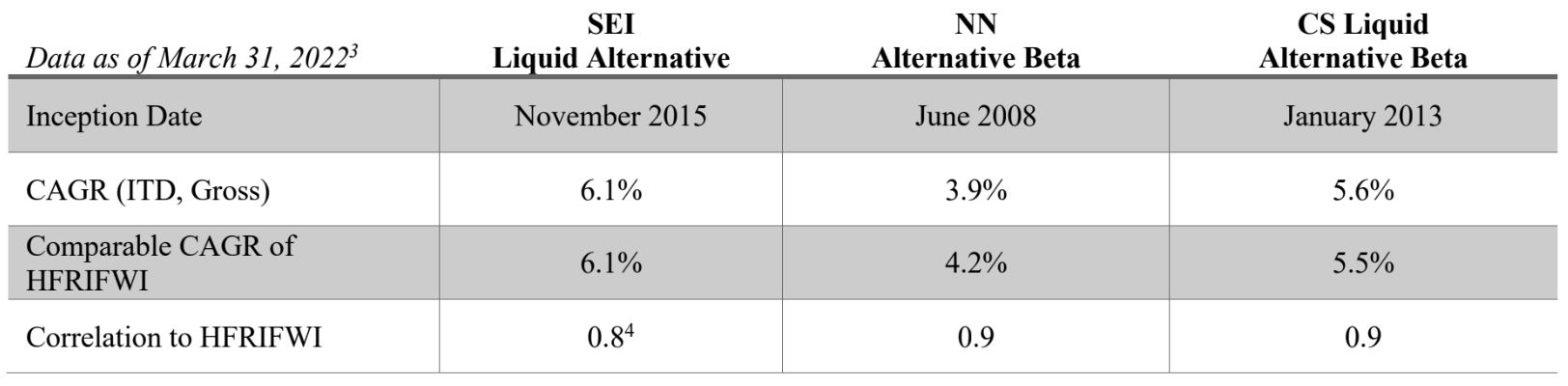

Where Should Allocators Start?

In UCITS land, there are three “pure play” factor replication products: SEI Liquid Alternative Fund

(note: we subadvise this one), NN Alternative Beta and Credit Suisse Liquid Alternative Beta. Each has

its own design nuances, yet all three have roughly matched the performance of “hedge funds” – here, for

comparison, the HFRI Fund Weighted Index – with impressively high correlation:

But that only tells half the story. The real comparison should be to hedge fund strategies packaged in UCITS funds. These “diluted” hedge funds – see the HFRX Global Investable Hedge Fund index – tend to underperform the real thing by several percentage points a year. By replicating the real thing cheaply, the replication funds above often rank among the top multi-strategy UCITS funds. [3] For wealth managers, this means replication-based UCITS funds are more “index-plus” than “index-like” and potentially can deliver on the allocator’s trifecta of strategy exposure, consistent outperformance and low fees.

Conclusion

One common knock on factor models is that they “replicate only beta” – not the pure alpha gold that allocators seek. This critique pre-dates the appreciation of factor rotations. Outside of some ivory tower statistics class, no one questions the “alpha” generated by, for example, the dotcom-era value vs growth trade or the recent Treasury short. And this, of course, is how hedge fund managers often describe each other: “Druckenmiller nailed the Treasury short,” “Andurrand went all in on his long crude oil bet,” “Maverick caught the value rotation early,” etc. All these factor rotations can be picked up by replication models. There are, of course, plenty of areas where you need to own the real thing – don’t try to replicate Citadel Wellington, PE-like distressed managers, or even merger arbitrage. But where replication works – hedge funds overall, equity long/short and (in our case) managed futures – it can work beautifully.

Whether revolutionary or evolutionary, it’s time has come.