Looking at the referendum result in terms of macroeconomics, financial markets and politics, our views are as follows:

Macroeconomics. The vote for Brexit is, we believe, likely to

reinforce a recent loss of momentum in parts of the UK economy.

We believe the result of the referendum will hit consumer and

business confidence, at least in the short term. Business

investment, already fragile, will be hurt, and so will credit

growth. Capital outflows are to be envisaged; the UK’s current

account balance will be hurt, as will government finances. As a

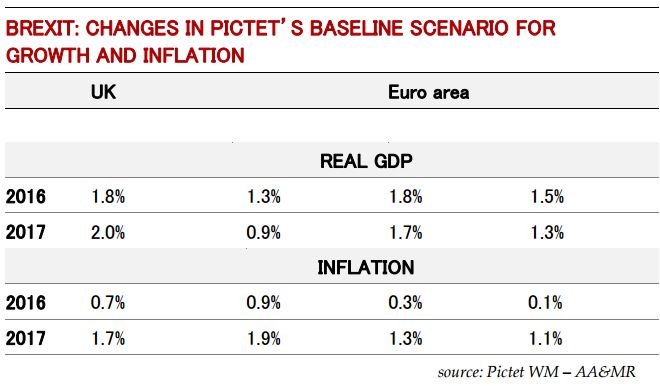

consequence, our baseline scenario is for real UK GDP growth of

the order of 1.3% this year and 0.9% in 2017, well below our

expectation earlier this year that UK GDP would grow by 1.8% in

2016 and by 2.0% in 2017. In addition, a sharp drop in sterling can

be expected to lead to a rise in imported inflation that will offset

any weakness in domestic inflation, at least in the short term.

We now believe real growth in the euro area could be 1.5% this

year instead of the 1.8% rate we had been forecasting. And we

expect the euro area economy to expand by 1.3% rather than 1.7%

in 2017. But given that the UK only accounts for 2% of the world

economy (on the basis of purchasing power parity), we believe

the Brexit vote will have only a slight impact globally. Our

central scenario now is that world growth will be of the order of

3% this year and next, instead of 3.2%. Central banks will likely

take coordinated action to avoid a liquidity crisis.

We now believe real growth in the euro area could be 1.5% this

year instead of the 1.8% rate we had been forecasting. And we

expect the euro area economy to expand by 1.3% rather than 1.7%

in 2017. But given that the UK only accounts for 2% of the world

economy (on the basis of purchasing power parity), we believe

the Brexit vote will have only a slight impact globally. Our

central scenario now is that world growth will be of the order of

3% this year and next, instead of 3.2%. Central banks will likely

take coordinated action to avoid a liquidity crisis.

Markets. Given our analysis that financial markets had never

fully priced in Brexit, and given the rebound seen in the days

running up to the referendum, we believe that volatility will rise

significantly despite central banks’ interventions and that risk

assets will come under pressure in the days that come. We also

believe that after the shock has passed, risk assets will stabilise

while market participants tease out the form that Brexit takes. But

this stabilisation could prove temporary and give way to

renewed market pressures.

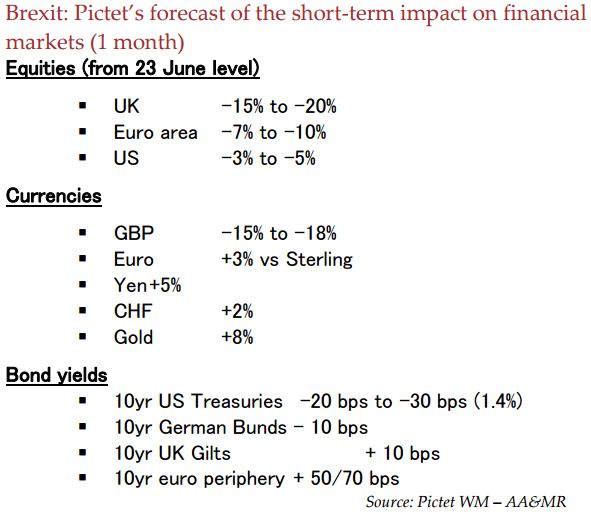

Our central forecast foresees a short-term drop of 12-15% in UK

equities from their current levels. We also believe that the fall-out

from Brexit will be felt in euro area equity markets, with the Euro

Stoxx 50 sliding by 7-10% in the short term. By contrast, we

believe US equities will remain relatively (but not totally)

immune from the Brexit vote. We expect a number of ‘safe haven’

assets to be boosted by the UK referendum result in the short term, including the Swiss franc, the US dollar, Japanese yen, gold

and core government bonds. Having risen close to GBP1:USD1.50

by referendum day from less than GBP1:USD1.39 at the end of

February, we believe the shock caused by the Brexit vote will

cause sterling to drop sharply again before stabilising in a range

of GBP1:USD1.25—USD1.35. The Swiss franc will also come

under renewed upward pressure, forcing the Swiss National

Bank to intervene in an effort to stop the Swiss franc from rising

beyond €1:CHF1.08.

Our central forecast foresees a short-term drop of 12-15% in UK

equities from their current levels. We also believe that the fall-out

from Brexit will be felt in euro area equity markets, with the Euro

Stoxx 50 sliding by 7-10% in the short term. By contrast, we

believe US equities will remain relatively (but not totally)

immune from the Brexit vote. We expect a number of ‘safe haven’

assets to be boosted by the UK referendum result in the short term, including the Swiss franc, the US dollar, Japanese yen, gold

and core government bonds. Having risen close to GBP1:USD1.50

by referendum day from less than GBP1:USD1.39 at the end of

February, we believe the shock caused by the Brexit vote will

cause sterling to drop sharply again before stabilising in a range

of GBP1:USD1.25—USD1.35. The Swiss franc will also come

under renewed upward pressure, forcing the Swiss National

Bank to intervene in an effort to stop the Swiss franc from rising

beyond €1:CHF1.08.

We expect a steepening in the yield curve on UK gilts in the short term before action by the Bank of England (BOE) leads to curve flattening. Expectations that the BOE would gradually move to normalise policy will need to be put on hold. We also foresee a renewed decline in US Treasury yields, with 10-year US Treasury yields perhaps falling by 20-30 basis points from their current levels. We expect a slight fall in German Bund yields (perhaps by 10 basis points) to be accompanied by a rise in yields on peripheral euro area bonds before possible intervention by the European Central Bank steadies the fixed-income market. Similar trends are to be expected in European corporate bonds.

Politics. The political impact of the vote for Brexit will be significant, but the UK and Europe have time to negotiate the mechanics of the UK’s exit from the EU. Article 50 of the European Treaty establishes a two-year negotiating period. During this time, the UK parliament will have its say, with results that cannot yet be foretold. There could be a “hard” exit (with no preferential access for UK exports to the EU) or a “soft” one (with some preferential access in return for notable concessions, in line with Norway’s relationship to the EU). We believe the UK could lose around 4% of potential GDP growth in the next five years if we see a “soft” exit, but that the UK could fall into recession in the short term and lose a cumulative 8% of potential GDP growth over five years should there be a “hard” exit.

The result has led David Cameron to announce his resignation as British prime minister. More fundamentally, we believe the referendum result provides a second wind to populism (and the tenants of economic protectionism) throughout the western world. We believe this populism will remain centre-stage in European politics for some time, increasing uncertainty and making life uncomfortable for mainstream policy makers. The future of the European economic union is at risk.