For stocks to climb, earnings need to grow.

When it comes to valuing shares, the price-to-earnings (P/E) ratio is a bit like the baloney sandwich of equity valuation. Wall Street’s finest might all know about more elegant, sophisticated and nutritious alternatives. Come lunch time, however, and you can bet they will join the queue and, more likely than not, opt for the baloney special at the local deli. The same bankers are also known to have a weak spot for good old P/E ratios when it comes to valuing shares.

Of course, this valuation measure has many weaknesses. On the plus side, it allows for comparisons with historic valuations and across sectors. But you either have to look quite hard to compare like-with-like or make plenty of adjustment. For historic comparisons of P/E ratios for a whole index, you should take into account changing sector weightings, accounting rules or simply different stages in the economic cycle.

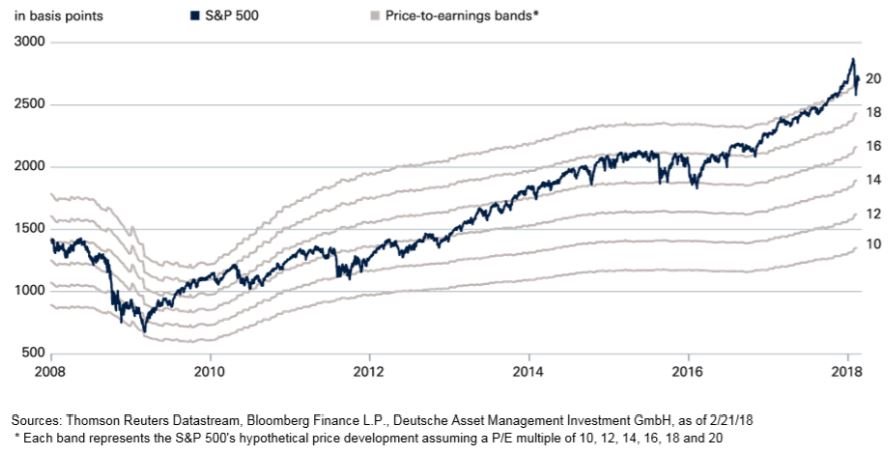

To put it succinctly: It all depends on the context, when you try to decide whether a P/E ratio of 15 is cheap or expensive. Our "Chart of the Week" shows the level of the S&P 500 since 2008, together with P/E valuation bands. The trailing P/E ratio of 15 in early 2008 has proved too high in retrospect. After all, earnings only started to crumble towards the end of that year.

By contrast, the P/E ratio of 15 in 2010 proved to be a bargain, because it was based on depressed earnings of the previous 12 months. So, there was plenty of scope for price gains on the back of growing earnings; until 2014, the P/E ratio remained fairly stable. Since then, much of the later gains in the S&P 500 was due to multiples expansion. The break-up at the turn of the year was due to U.S. corporate tax cuts. Investors priced in the likely earnings gains, even though these only are likely to begin to materialize in 2018. Independently of this, we have been assuming for a while that the S&P 500 may have already passed its peak P/E ratio of the current cycle. We continue to expect earnings to grow in 2018, and retain a constructive stance on U.S. equities. However, we prefer Europe and emerging markets.