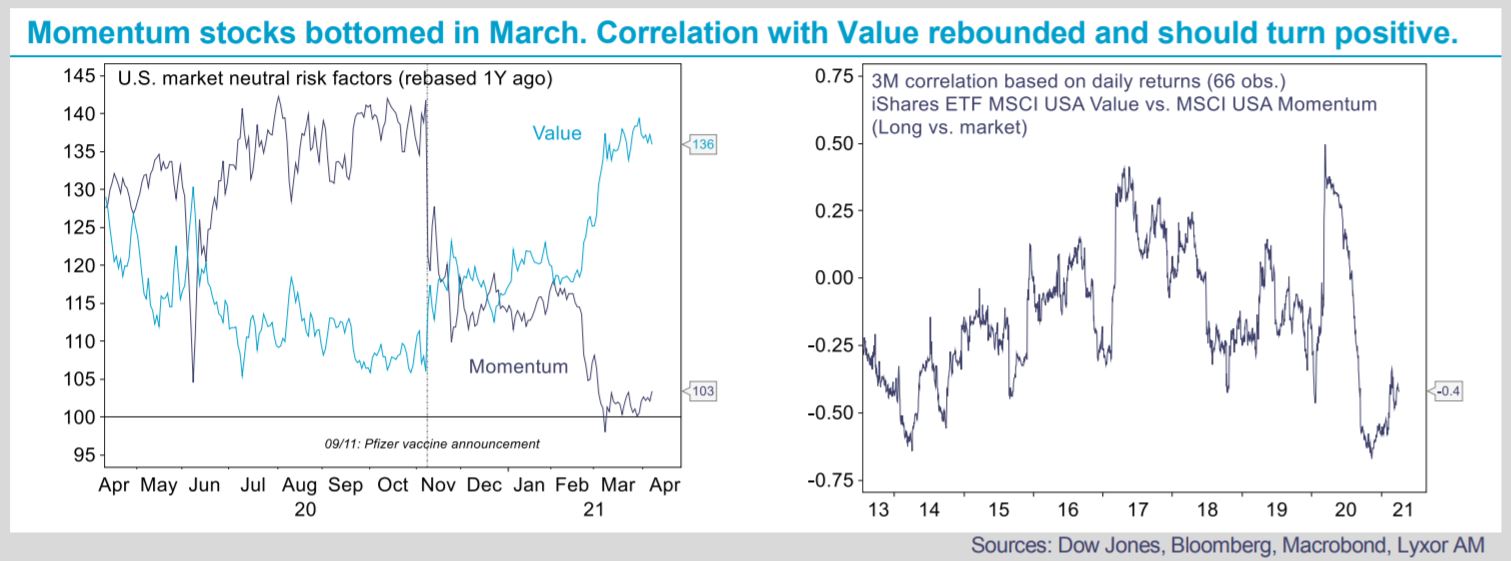

Yet, estimates of the correlation between Momentum and Value vary depending on the benchmark. Dow Jones Thematic or MSCI USA Value/ Momentum indices fail to reflect adequately the new correlation regime due to their quarterly or semi-annual rebalancing, which provokes inertia.

Alternative strategies with a Momentum bias such as Market Neutral L/S performed reasonably well lately. They outperformed year-to-date, up +1.8% according to Lyxor Alternative UCITS Peer Groups. Such strategies use proprietary approaches to build Momentum exposures, with probably less inertia than the benchmarks discussed above. They thus appear to have an enhanced Value bias (see page 2), which is implied by their Momentum exposure.

Going forward, the near-term prospects for the strategy have marginally improved. The Momentum bias allows Market Neutral L/S to capture better economic prospects, now that the correlation with Value is increasing. For investors that are risk constrained, the low volatility features of the strategy coupled with the current cyclical bias are somewhat supportive.

However, longer term, the strategy remains vulnerable to factor rotations as it is uncertain that the recent trend for value will last very long. Additionally, no market directionality will curtail their capacity to capture the economic rebound, with fundamentals back in favor.

Market Neutral L/S are likely to keep underperforming other hedge fund strategies as showed by their track record over the last few years. At this stage of the business cycle, Event-Driven, CTAs, and Directional L/S look more attractive to us.