Global stocks are up year-to-date, having shaken off worries about the strength of the global economy in the wake of the UK’s Brexit vote. But we believe further gains require a meaningful improvement in corporate earnings, particularly in developed markets.

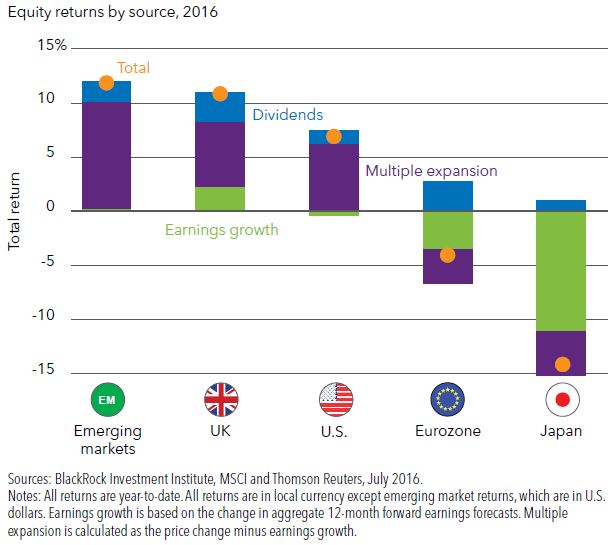

Equity markets are running on fumes. The chart above shows how multiple expansion — or rising price-to-earnings ratios — has been the main driver of returns in many markets this year. Earnings growth has been flat to negative.

The main ingredient required for further gains

The worst of the U.S. profits recession appears to be over. Second-quarter earnings growth for the S&P 500 likely will still show contraction from last year’s levels. Yet we find reasons to be marginally more optimistic about the second half. Sales growth has been better than expected, and is on track to turn positive for the first time since the fourth quarter of 2014. We also see the energy sector’s drag on earnings fading by year-end. The problem? High U.S. valuations and strong flows into U.S. equities already appear to reflect part of the good news. A U.S. market overweight has become a consensus trade, our analysis shows, raising the risk of sudden reversals.

In Europe, analysts have slashed their expectations for 2016 earnings growth since the beginning of the year on a collapse in expectations for the banking sector. Earnings are set to contract in seven out of 10 European sectors in the second quarter. The bright spot: global multinationals with geographically diverse sales, in sectors such as health care, materials and technology. In Japan, many companies are budgeting for a weaker yen in the second half, surveys show. This increases the risk of downward earnings revisions if the yen stays strong and hurts the overseas earnings of Japanese companies.

The main takeaway for investors: Be selective. We prefer quality companies that can increase earnings in a low-growth environment or grow their dividends. U.S. stocks with high dividend payouts, by contrast, look expensive and offer limited earnings potential at this time, we believe.