The Special Situations strategy went through a roller coaster since February. Typically, due to their long structural market beta, managers tend to underperform in risk-off episodes. However, as they also tend to look beyond short-term volatility, they usually rebound faster. This time, they started the year with more cautious beta exposures but were more concentrated on sectors that were hardest hit during the market crash, in energy and consumer stocks. They have now retraced about two-thirds of their losses. While market corrections usually open buying windows for Special Situations and activist strategies, we find that, since the market crash, global activists launched less than 30 new campaigns.

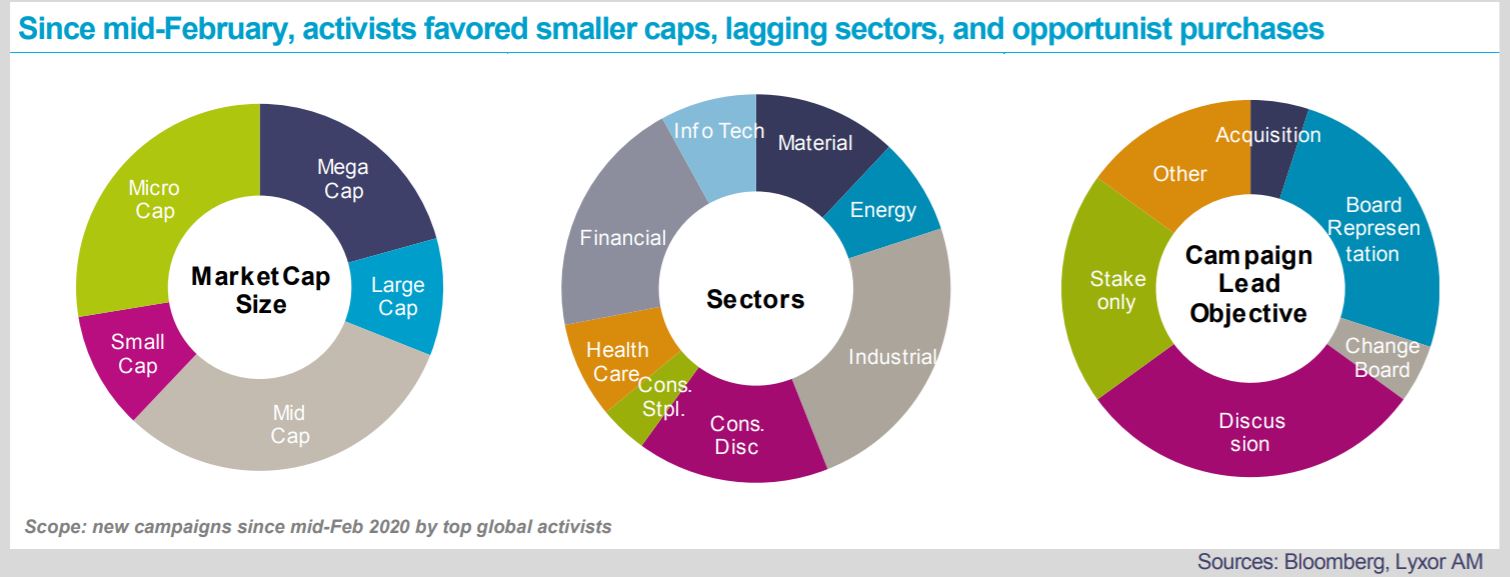

A majority of these targeted companies are mid or small caps, displaying mixed credit solidity, mainly in the industrial and financial sectors, which lagged since February and still trade at substantial discounts. Moreover, the lead objectives of these campaigns seem opportunist (holding discussions, building stakes) rather than targeting a specific change (acquisition/assets sales, shareholders distribution, or governance change). Similar observations emerge from the stage of the business cycle of these new positions, none of them in clear turnaround situations or calling for deep restructuring.

All in all, activists have not shown the same appetite for bargains than in previous selloffs. A V-shaped market rebound and rich valuations are not providing a large universe of oversold stocks. Moreover, given that the full effects of the pandemic on businesses have yet to emerge, concentrated and buy-and-hold Special Situations managers are still reluctant to add much risk. Instead, they have opportunistically picked cheap stocks still under pressure from the virus, in aerospace, reits, financial services, leisure businesses – a majority of which performed nicely in the recent weeks.

According to public filings as of the end of March, in aggregate, the bulk of activists’ positions concentrate in financials, tech and communications, and industrials sectors.

So far, corporate activity is still far from pre-crisis level. M&A, asset sales, IPOs, which are critical in Special Situations’ exit strategies, remain anemic. Encouragingly, the number of extraordinary shareholder meetings, where most corporate operations are decided, are healthily rebounding. It suggests corporate activity will normalize along with trading conditions. A more decisive rotation back into value stocks, especially in the small and mid cap segments, would also be a strong tailwind for Event Driven managers (and for most fundamental investors). We keep a constructive view.