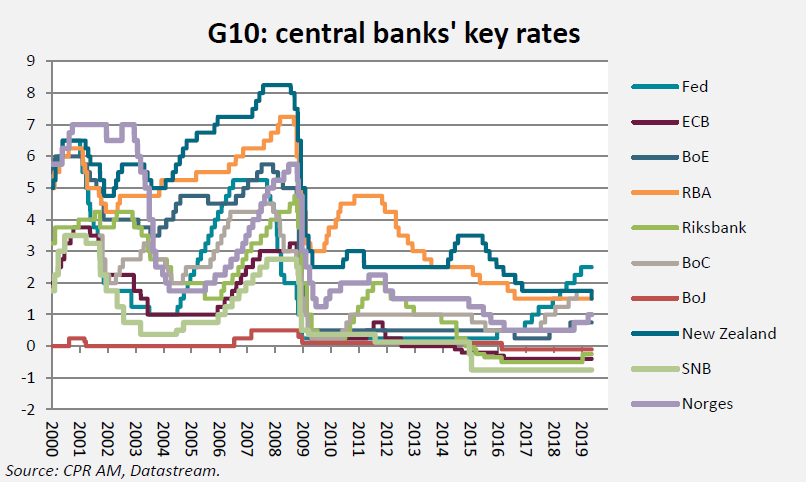

In the decade following the Great Recession, central banks in developed countries have resorted overwhelmingly to unconventional measures to satisfy their mandates, be they dual (price stability and full employment) or solely focused on price stability. For example, the ECB, the Fed, the BoJ, the BoE and the Riksbank have launched quantitative easing programs, purchasing various assets (government bonds, corporate bonds, covered bonds, mortgage-backed securities, equities, ETFs, etc.). The SNB has even bought large amounts of securities denominated in foreign currencies to combat the overvaluation of the Swiss franc. Several central banks have also opted for a negative interest rate policy (ECB, BoJ, SNB, Riksbank).

In the end, the central banks of the developed countries will not have the same room for maneuver when the next recession will take place:

- It is hard to imagine that policy rates can plunge too far into negative territory (below a certain threshold, which Benoît Coeuré [1] calls the "physical lower bound", households would withdraw their deposits from banks en masse, what would threaten financial stability)

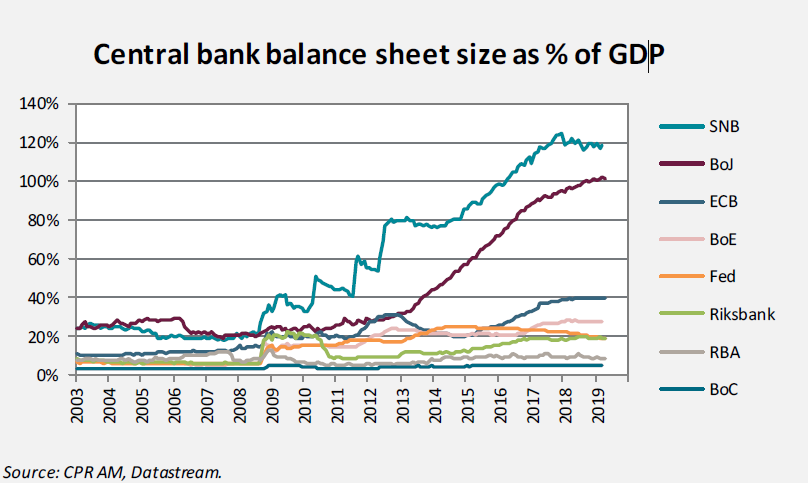

- It is hard to imagine that central banks’ balance sheets would expand indefinitely: 1) for reasons of the rising scarcity of purchasable assets (for example, the Bank of Japan will become the first Japanese equity holder in 2020 [2]), 2) for reasons of financial stability [3] because of possible losses on the assets held (it is difficult to imagine that the size of the balance sheet exceeds much more of - say - 100% of the GDP) and 3) for reasons of interference with the political authorities.

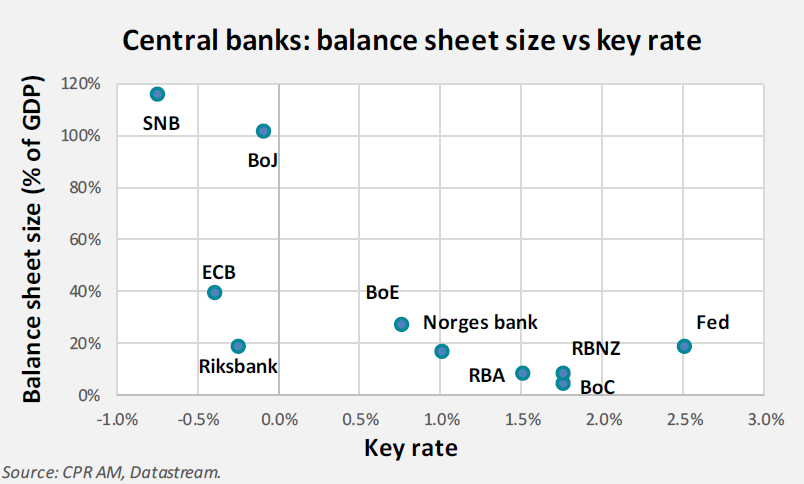

Here is the comparison of key rates / balance sheet size for the central banks of G10 countries (data for March 2019):

In these conditions:

- With negative rates and a very high balance sheet size (respectively 117 and 102% of GDP), the SNB and the BoJ seem to have relatively little room for maneuver to cope with a possible recession or to fight against a possible strong currency appreciation (the Swiss franc and the Japanese yen are generally considered as heaven currencies).

- The Fed is the central bank of the G10 with the highest interest rates and its balance sheet is not so high when it is considered as % of GDP (19% of GDP). The Fed appears as the central bank with the highest room for maneuver to cope with the next recession in the G10 space.

- The RBA, the RBNZ and the BoC are in an intermediate position with key rates at 1.50 / 1.75% and a very small balance sheet relative to the economy (9%, 9% and 5% of GDP respectively). The potential in terms of QE or in terms of possible loans to banks is very important for these central banks. Note that for these three countries, the evolution of the real estate market is threatening ...

- The ECB appears to be one of the central banks with the smallest room for maneuver in the G10 space... because its interest rates are already very negative and because the size of the balance sheet is already relatively large (in addition to the self-imposed issuer share limits).

- The balance sheets of the Norges Bank and of the Riksbank are limited in size. But it must be taken into account here that the public debt is itself very weak in Norway and Sweden. Therefore, the potential for very large QE is limited...

In the end, the Fed appears as the central bank of developed countries that has the greatest room for maneuver for the next recession while the Bank of Japan, the Swiss National Bank and to a lesser extent the European Central Bank will have much less. This should translate into an appreciation of the yen, the Swiss franc and the euro against the US dollar. Note that over the period from 2007 to September 2008, the sharp decline in US long-term rates relative to its G10 equivalents contributed to a global depreciation of the US dollar.