Japan is also leveraged to the global cycle, highly sensitive to activity in Asia, China and the U.S. Its main exporting products are also cyclical. Moreover, monetary and fiscal stimulus would remain highly supportive, with upside from consumption provided confidence returns. Second, Japan is undergoing market friendly structural changes. Suganomics’ focus is on decarbonization, digitization, sector productivity improvement, and higher mobile penetration. These reforms would further improve foreign investors’ access and corporate governance, with intensifying corporate activity. While Japanese companies tend to keep their operating and non-operating costs in control, their key weakness lies with lower gross-margin than in other DM stocks.

Thus, a more fluid corporate environment could unleash Japanese equities’ top-line growth leverage. PM Suga is running against the clock before October elections and is speeding up reforms, though these could be jammed by his declining poll support and politics. For now, investors give reforms the benefit of the doubt, but little is priced in yet.

Third, Japanese equities remain under-owned. Anemic growth, the toll from the trade war and the pandemic resulted in declining allocation to Japanese stocks (2% decline in world market cap since 2018), primarily driven by households and foreigners. Households’ huge savings could gradually be put back to work. Fourth, with the pandemic gradually abating and as the Japanese economy regains some momentum, we see a wider set of investment themes, supporting stockpicking. These themes include stocks sensitive to domestic consumption, exposure to Asia, reflation policies or capex.

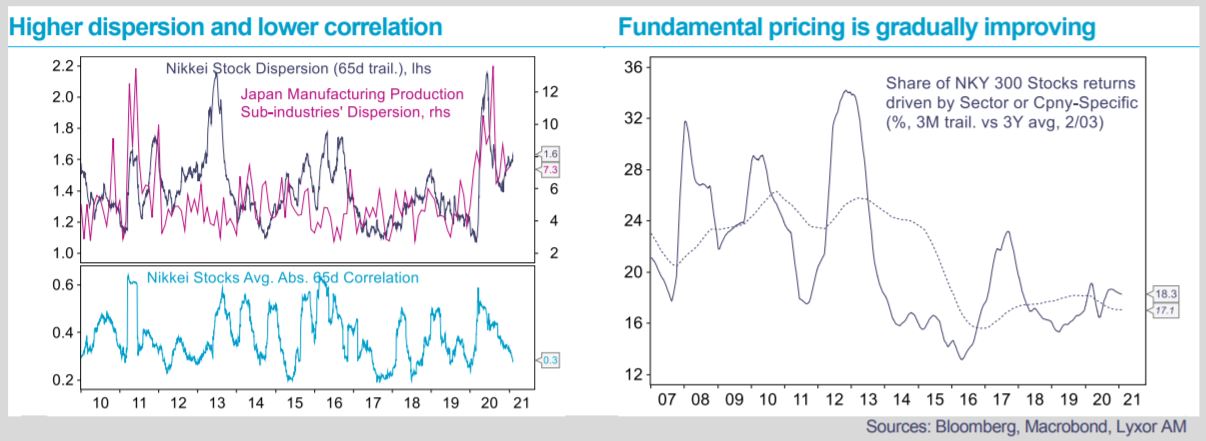

The alpha environment has already improved. Dispersion across stocks, sectors, factors and themes (a gauge of managers’ arbitrage potential) remains elevated and consistent with diverging economic trends across sub-industries. Meanwhile correlations are steadily declining, emphasizing more diversified opportunities. Moreover, fundamental pricing (how stock prices reflect underlying companies’ fundamentals) is improving, another pivotal factor for alpha generation.

We are not surprised by the rising number of new Japanese equity fund launches. Our peer group of Japanese equity

UCITS confirms the above observations. Their returns are increasingly differentiated and reflect uneven positioning and

uneven investment themes. They raised their overall exposure, expressing confidence. Importantly, while their alpha

was impaired during the 2017-2019 trade war, it is now back in positive territories. All on all, making greater room for

Japanese equity active managers in portfolios makes sense to us.