However, stimulus and highly accommodative monetary conditions managed to mitigate the impact on household income and corporate profits, witnessed by stable unemployment and a strong earnings season.

With virus infections moderating, restrictions will be gradually lifted. After a laborious start, purchase and distribution of vaccine doses have substantially accelerated, allowing the region to catch up part of its lag with countries such as the UK or the U.S. Europe is now two-to-three months behind, not quarters behind. It suggests that a broader economic re-opening is at hand, with pent-up domestic demand boosting growth in H2 2021.

European significant exposure to the global cycle will also positively contribute. Europe seems well-positioned to benefit from U.S. reflation policies. Europe also looks wellpositioned to navigate some of the post-pandemic secular trends in green capex, while navigating digitization will be more challenging. A key challenge for Europe will be to navigate the Northern vs. Southern economic rift. With low funding rates, still affordable valuations, more economic stability and multiple business turnaround, corporate activity is set to accelerate in Europe, providing catalysts.

We find that L/S Equity Directional managers focusing on Europe are becoming more optimistic, but in a cautious way. Overall, their net exposures remain close to historical highs, with limited short positions, though they refrain from adding leverage. They had already reallocated to stocks sensitive to economic reopening and are now starting to move towards riskier investment cases. However, they still pass on the hardest hit businesses found in airlines, hospitality, or retail. In recent days, they marginally favored cyclical positions, such as industrials, materials, and financial stocks. In aggregate, portfolios show a slight tilt on cyclicals and growth factors. Yet, as they worry about continued market rotations, managers are keeping increasingly balanced exposures across factors and sectors, rather focusing on single stock-selection.

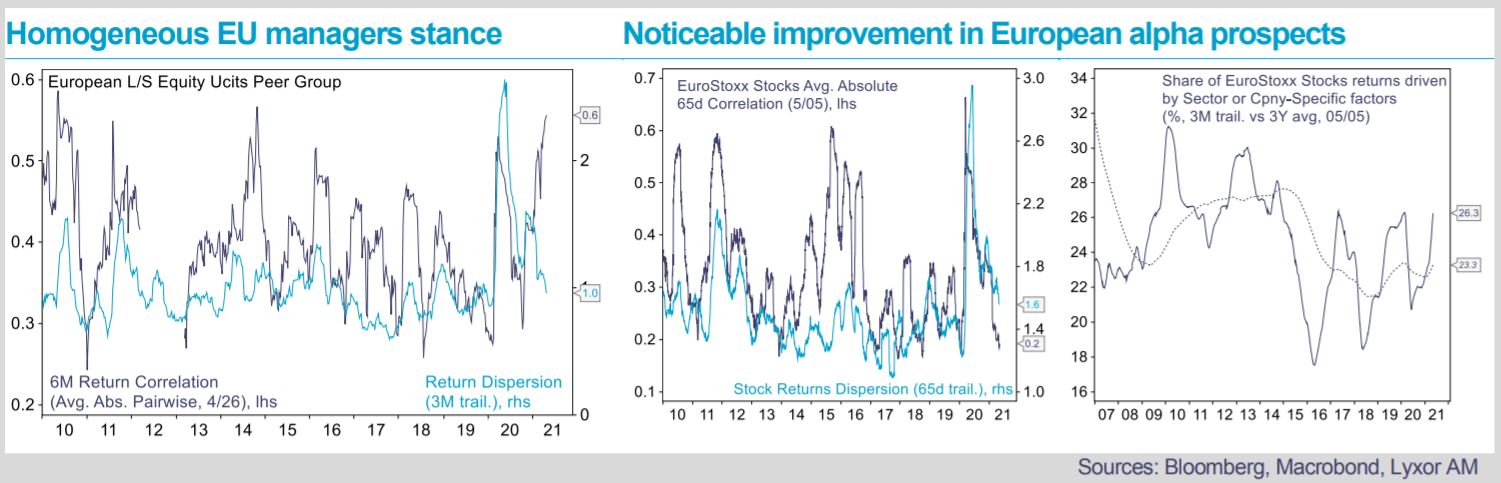

Regionally, they have reweighted stocks in core EU countries (Germany and France in particular) and in the UK, at the expense of Nordic markets which had shown to be more resilient in rougher times. Also, they have noticeably reweighted companies reliant on domestic revenues since mid-March, selling those exposed to foreign revenues. The high level of correlation across managers’ returns and their low dispersion, suggest a homogeneous stance on the European recovery.

Wildcards and several false starts in European activity are keeping managers in cautious optimism. They are also concerned that, past the initial activity spike, companies’ comparables and valuations could be harder to beat later this year. Some of them also enjoyed strong returns year-to-date and prefer to lock them. After a disappointing Q1, alpha has improved since April, for smaller funds especially, that outperformed the larger, mainly due to a higher market beta.