The post-ECB correction observed since last Friday confirms our view described in August and again last week in our latest Asset Allocation monthly publication: after a historically calm summer, September is likely to be a month of transition towards more volatility.

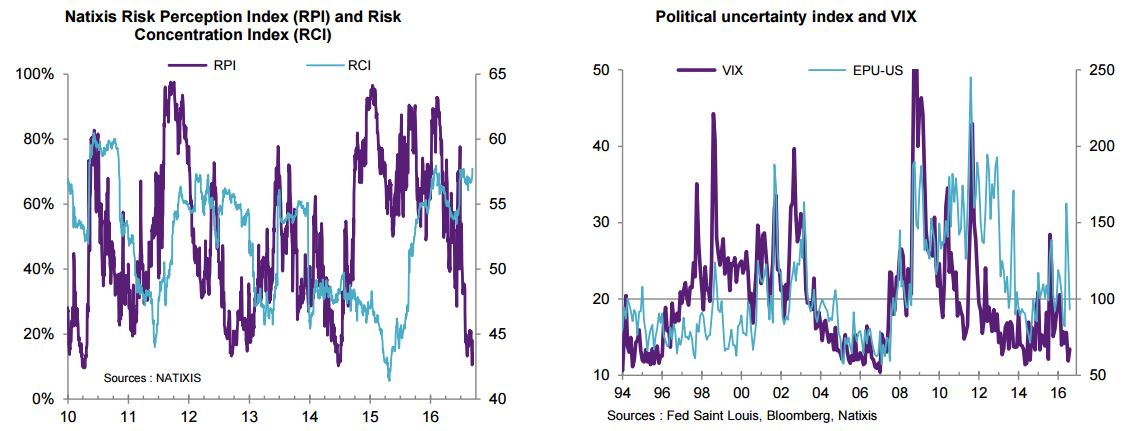

Our Proprietary Risk Perception Index (RPI) that was standing at a two-year low last week, has already jumped from 10% to 18% over the last few days while our Risk Concentration Index (RCI) remains high. We expect that we will return into a normalized and intermediate risk regime (with a RPI typically ranging from 25% to 50%) in the next few weeks. The 21 September FOMC meeting will be the key event of the month as we expect the Fed to hike in December.

We see two major catalysts in the short run for a higher risk/volatility regime:

1. Transition among central banks, which will prepare the markets for changes at the end of the year against the backdrop of increased divergence between the Fed’s stance - with a 25bp rate hike expected in December this year - and that of the other main central banks (ECB-BoE-BoJ), which are expected to adopt an even more accommodative bias. We believe the market underestimates the Fed’s resolve to increase its rates, which Janet Yellen spelled out in her latest speech at Jackson Hole (the market prices in only a 52% probability of a hike in December and no move is completely priced in before 2018!): we are turning negative on T-Notes, with a risk of a correction after the 21 September FOMC meeting.

For the euro zone, we expect an extension of the QE programme after March 2017, but we do not believe new measures will be taken (deposit rate cut, increased purchases, substantial change to the purchase rules, etc.). We expect range trading in EUR government bonds, which are subject to divergent forces (disappointment with the ECB, European political risk, negative directional on T-Notes due to the rate hike), and we are more defensive on long durations. We remain positive on Gilts due to the expected rate cut at the end of the year, as the impacts of Brexit are yet to come.

2. An expected rise in political risk. This factor is likely to be very present over the next few months (US elections, referendum in Italy, rise of anti-European Union parties). However, a rise in political risk is always accompanied by a resurgence of volatility. It may also trigger a more or less protracted risk aversion shock (for more details, see Political risk: what impacts on assets?). We maintain a positive view on gold as a potential hedge.

Beyond those two catalysts, we also see two majors ongoing transitions :

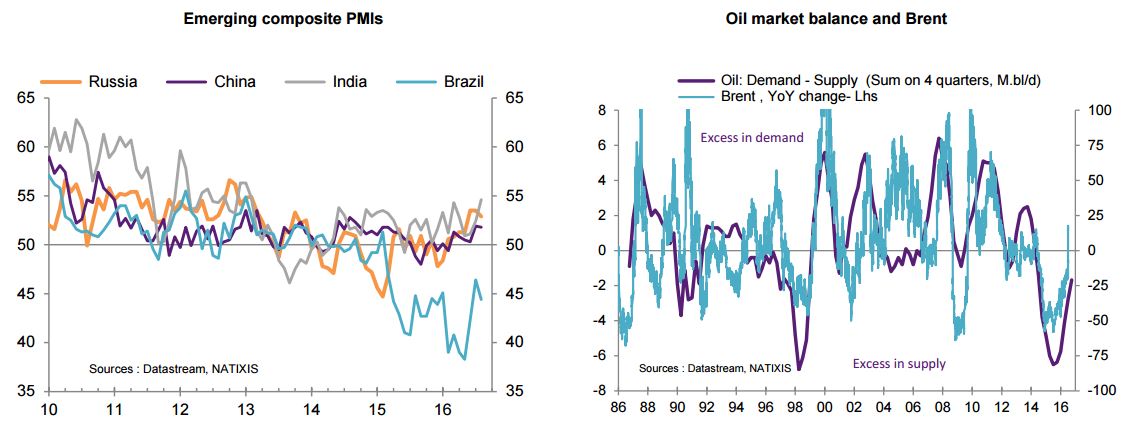

3. Transition in the oil market: beyond speculative positions and/or decisions on an OPEC/non-OPEC agreement to freeze production, oil price developments reflect a gradual market rebalancing (reduced excess supply). The coming weeks will nevertheless be particularly volatile pending the results of the informal meeting of OPEC and non-OPEC members on 26-28 September in Alger.

4. Transition in emerging economies, with an upward revision of growth prospects (mainly in Latin America) against a backdrop of an improvement in the economic and political news flows. With this in mind, our preferred call is now Brazil and we remain positive on oilexporting countries. We are nevertheless tactically reducing our exposures to emerging equities due to the risk of a repricing following a Fed rate hike, and after the strong rally and the massive flows from non-residents (see our flow indicators in the Appendix). We remain positive on emerging debt, whose carry remains very attractive.

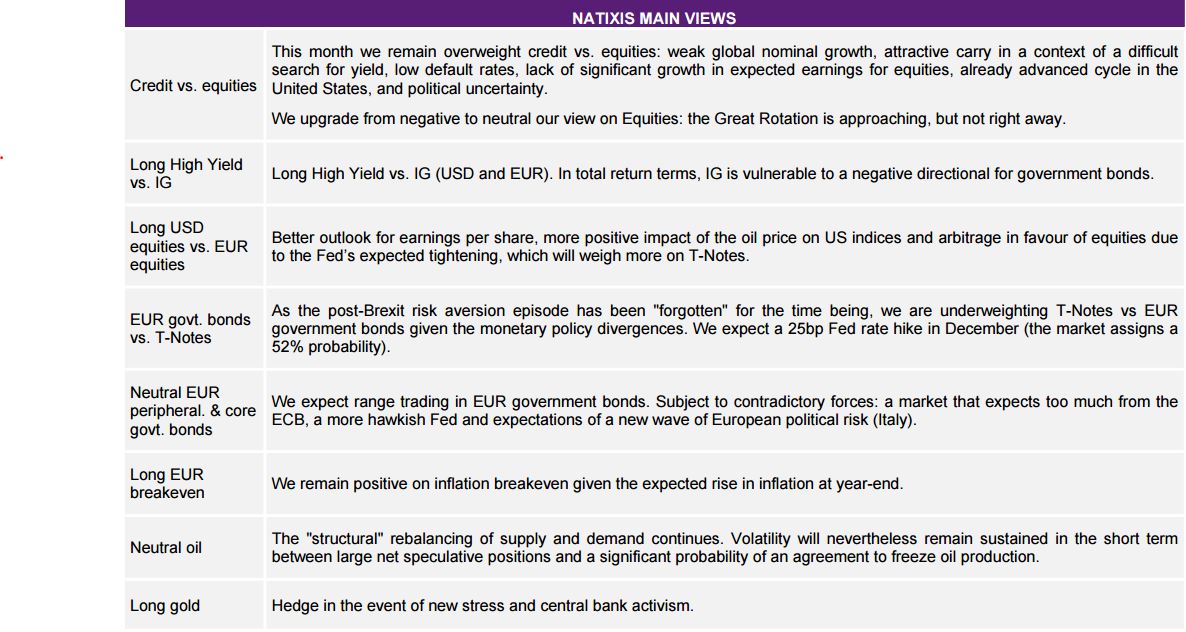

Overall, here are the summary of our asset allocation views for the coming month (see Asset Allocation):