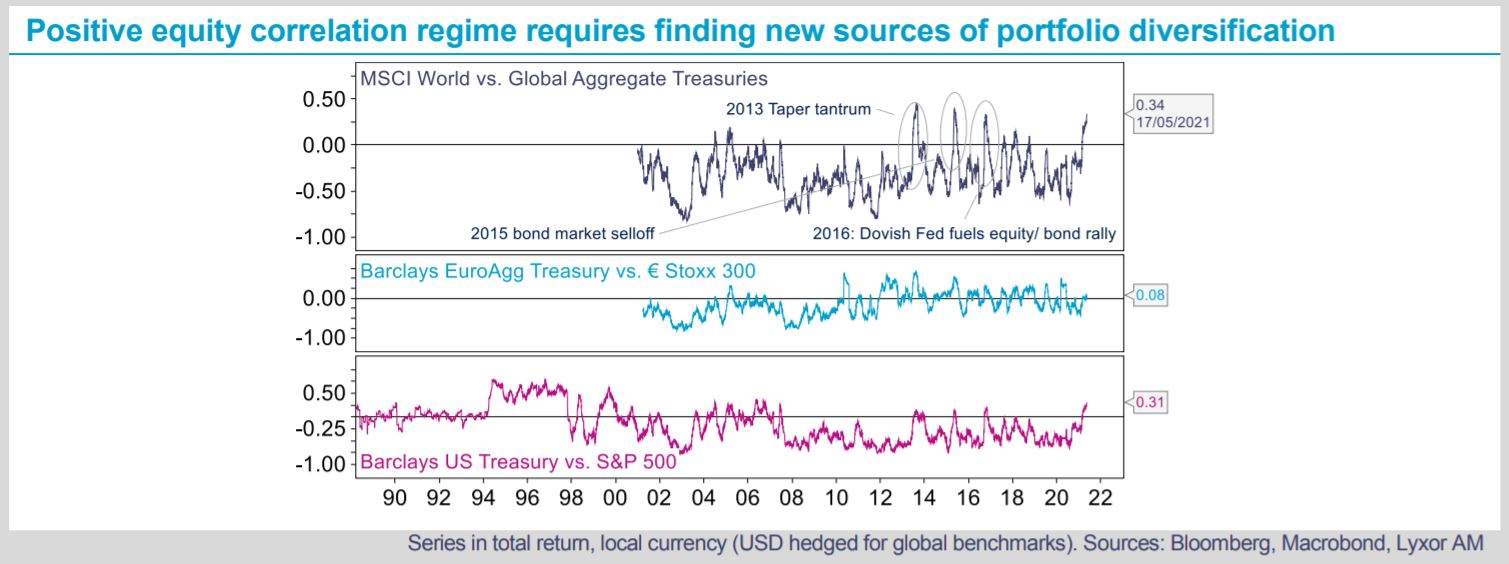

With bond yields facing upward pressures as the global economy heats up, finding diversification across traditional asset classes has been increasingly difficult. Equity valuations, which were propelled by low interest rates in the past decade, are vulnerable in the face of rising bond yields. Traditional equity/ bond portfolios are not as diversified as they had been. We estimate the global equity/ bond correlation has turned positive early March and continued to rise to 0.34 at present, a record since 2016. A positive correlation regime between equities and bonds is not necessarily a bad thing. In the late ‘90s, returns were positively correlated for years because both asset classes were rising. In the past decade, shifts in correlation regimes were short lived, but have the potential to cause substantial pain for investors. At this stage of the business cycle we are monitoring the extent to which a rise in bond yields would hurt equities and the fact there are not so many alternatives to fixed income to protect portfolios.

As an alternative strategy, CTAs are generally considered to be a pure diversification strategy. Their long-term correlation to equities and bonds is close to zero and their track record in bad times is outstanding. Our stance on the strategy has been Overweight since February. We believe they continue to provide diversification and upside potential. CTAs do have a positive correlation with equities at the moment, which we estimate between 0.5 and 0.6 depending on the CTA benchmark. Yet, their fixed income exposure is virtually zero or negative. The strategy recently covered Treasury shorts and turned short on European bonds. The 3-month correlation to Bund and Gilt futures has turned negative lately. Also, their long positioning to commodities is a hedge against rising inflation expectations but could be a source of risk due to their elevated exposure.

Going forward, our stance on the strategy remains Overweight. As long as the rise in bond yields does not trigger

an equity correction, which is our base case, CTAs have the potential to continue delivering attractive returns. Our

stance on equities remains constructive, to the extent that we expect the earnings momentum to provide a cushion

against rich valuations. We are also positive on cyclical commodities at this stage of the business cycle.