The last twelve months have shown a dispersion in the returns of CTAs. At the end of Q1 2016, the rolling one-year performance of the SG Trend Index, which measures the performance of the trend following industry, was -4.1%, whereas the performance of the Lyxor Epsilon Global Trend fund was -1.7% for the same period. Over 2015 as a whole the Lyxor Epsilon Global Trend fund returned +5.4% and during Q1 2016 it returned +3.0%. “The CTAs who did well during this period where those which reduced overall exposures and focused on the few trends available”, explains Guillaume Jamet, principal fund manager of the Lyxor Epsilon systematic trend program.

Trend following strategies are also referred to as Commodity Trading Advisors, or CTAs. They exploit the momentum effect: prices going up (going down) tend to keep going up (going down). Trend following strategies work best in environments in which markets show clear and identifiable trends and in which correlations between asset class returns are low.

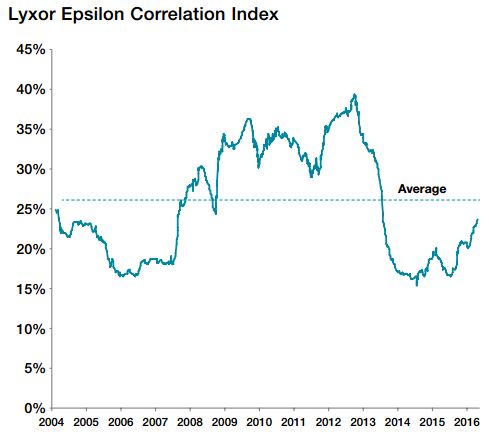

The less advantageous market context relates both to correlations and on the level of market ‘trendiness’: The Lyxor Epsilon Correlation Index increased from 20% to 24% during the first quarter of 2016, approaching 26%, which is the average index value since it was created in 2004.

The index is backward looking: it analyzes some of the drivers of the past performance of trend following strategies, but gives no indication

of future results.

The index is backward looking: it analyzes some of the drivers of the past performance of trend following strategies, but gives no indication

of future results.

Source: Lyxor AM. Data as of 31/3/2016

The Lyxor Epsilon Correlation Index* uses various return and risk indicators to estimate the correlation amongst markets on a rolling 1-year basis. A low value means that markets tend to move independently, while a high value means that markets tend to move in lockstep.

“This environment clearly was less favorable than the twelve months ending Q4 2015, without becoming worrisome”, comments Guillaume Jamet.

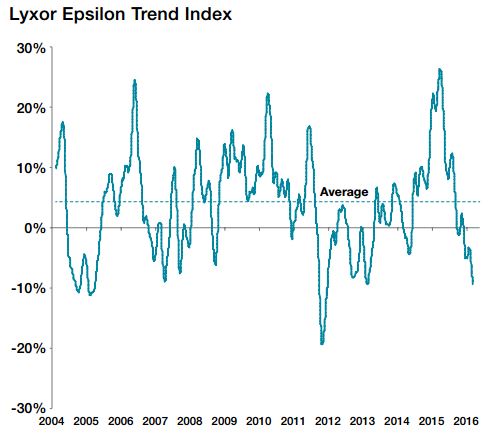

During the same period the Lyxor Epsilon Trend Index dropped from -2% to -10%. This value is well below 4%, which is the average index value since it was created in 2004.

“Markets have been clearly rangy during the lasts 12 months due to a high level of macro-economic uncertainty. 2016 seemed to start with trends, such as on equities and on oil, but most of these trends reverted as of late February”, tells Mr. Jamet. “Models that adapted to this environment will be reactive once trends re-occur. The overall exposure level of the Lyxor Epsilon Global Trend fund is below average currently.”

The Lyxor Epsilon Trend Index* uses various return and risk variables to calculate the average strength of trends on financial markets on a 1-year rolling basis. A high measure means that, on average, the financial markets included in the index have been characterized by a higher directionality, either downward or upward. A value close to zero corresponds to a regime when most markets are trading randomly. A low negative index value means that markets are “rangy” on average.

The index is backward looking: it analyzes some of the drivers of the past performance of trend following strategies, but gives no indication

of future results.

The index is backward looking: it analyzes some of the drivers of the past performance of trend following strategies, but gives no indication

of future results.

Source: Lyxor AM. Data as of 31/3/2016

Due to their diversification over a broad investment universe and their ability to go short, trend following strategies are amongst the few strategies able to benefit from any macro trend, be it bear equity markets, interest rate hikes or currency wars.