Such portfolios can provide an element of protection for a company’s capital and profits as market volatility rises.

Volatility has moved relentlessly lower during 2017, and any disruption to this trend has been immediately and completely quashed. This makes sense in light of the dual influences of improving fundamental and ongoing friendly conditions nurtured by central banks around the world. At this point, investors expect ongoing strength in growth and profits, so any downside surprises could catch investors wrong footed. As a result, investors are beginning to add to long-short equity portfolios to navigate the markets moving forward.

THE BATON PASSES FROM MONETARY TO FISCAL POLICYMAKERS

The S&P 500 Index has more than tripled in value since its low in March 2009, while the operating earnings of S&P 500 companies have doubled to around US$1 trillion. This remarkable feat was achieved with huge help from low interest rates, coupled with stimulus in the form of quantitative easing (QE), which some would argue created artificial market conditions by prolonging the economic cycle and dampened volatility. QE brought down the cost of capital for businesses and this low cost of borrowing allowed even subpar businesses to survive and prosper. Without QE to act as a buffer, it is probable that some of these subpar companies would have struggled.

Post US elections, investor focus shifted from monetary policy to fiscal policy. Trump’s ‘America First’ policies have rejuvenated market expectations for growth (fiscal policy, tax reform and deregulation).

Trump’s ‘America First’ presidential promise – where he pledged to spend US$1 trillion on a 10- year infrastructure programme, overhauling the country’s roads, bridges and tunnels – has excited the markets. Trump has also pledged ambitious reforms to the US tax system, which has not been significantly reformed since 1986. “The US corporate tax rate, including state and local taxes, is the highest among advanced economies”, notes a January 2017 report by PwC. This has rendered American companies uncompetitive compared to their peers in other countries. If Trump’s plan is enacted, this could revitalise the US domestic investment, while the tax amnesty on foreign cash will encourage US companies to bring their foreign cash home and further invest or distribute it in the US. However, the fine print contains ‘border adjustability’ of the taxes with serious ramifications for the likes of Apple and Walmart.

Markets have come to agree that the Trump administration is one of the most pro-business administrations of recent years. However, Trump’s last few months in the White House have raised doubts on his ability to deliver on his campaign pledges, pushed out the expected timelines of legislative changes, raised questions on his governance style and created nervousness among the US allies around his priorities. So this tide is not going to raise all boats. One thing is for sure, going forward there will be winners and losers among US companies.

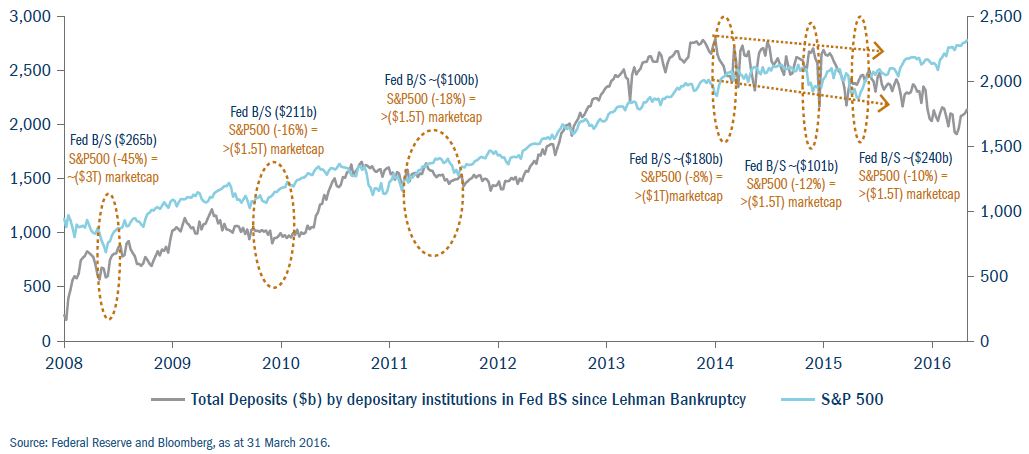

On the monetary front, in the years since the financial crisis, the Fed has expanded its balance sheet by almost five times. They have signalled a willingness to reduce their debt burden now. However, there is clear correlation between balance sheet reduction and market corrections (see Figure 1). As the baton passes from monetary policy to fiscal policy, will the volatility trend continue to be quashed? Could any downside surprises catch investors wrong footed?

Figure 1: Correlation between Fed Balance sheet and S&P 500 and the breakdown post US Elections

TIME FOR ABSOLUTE RETURN

This is an environment in which long-short equity portfolios are designed to perform well, as their managers have the ability to navigate the markets’ volatility by dynamically altering their exposure to equity investments. Such long-short portfolios can benefit more from the diverging fortunes of companies, which present greater opportunities for fundamental stock-picking. They can invest not only in stocks they believe are poised to rise, but also ‘short’ those likely to fall.

At Columbia Threadneedle Investments, we believe that an absolute return strategy with a long-short US equity portfolio could be attractive for investors who are looking for less volatility and the potential for consistent investment returns.

We believe that turning these opportunities into solid returns takes highly skilled stock-picking, driven by a fundamental research framework. As legendary investor Warren Buffett has said: “It’s common for promoters to cause a stock to become valued at 5-10 times its true value, but rare to find a stock trading at 10-20% of its true value. So you might think short selling is easy, but it’s not.”

STOCK SELECTION CAN DRIVE OUTPERFORMANCE

Long-short equity portfolios can benefit more from the diverging fortunes of companies, which present greater opportunities for fundamental stock picking. In managing our US Equity long-short portfolio, the Threadneedle (Lux) American Absolute Alpha Fund, we seek to take advantage of market volatility by holding long positions in companies we expect to flourish over the long term and go short in companies which are expected to have a tougher time. Unlike many of our peers, we do not invest in complex derivatives. We place great importance on fundamental research and industry analysis and believe that this approach will tend to identify quality companies that are more likely to outperform over the long term. We combine our team’s experience and rigor with the extensive resources and robust risk framework of Columbia Threadneedle Investments to create alpha. A powerful combination of fundamental, bottom-up stock picking, together with top-down analysis, coupled with a strong buy/sell discipline, helps us deliver strong risk-adjusted returns.

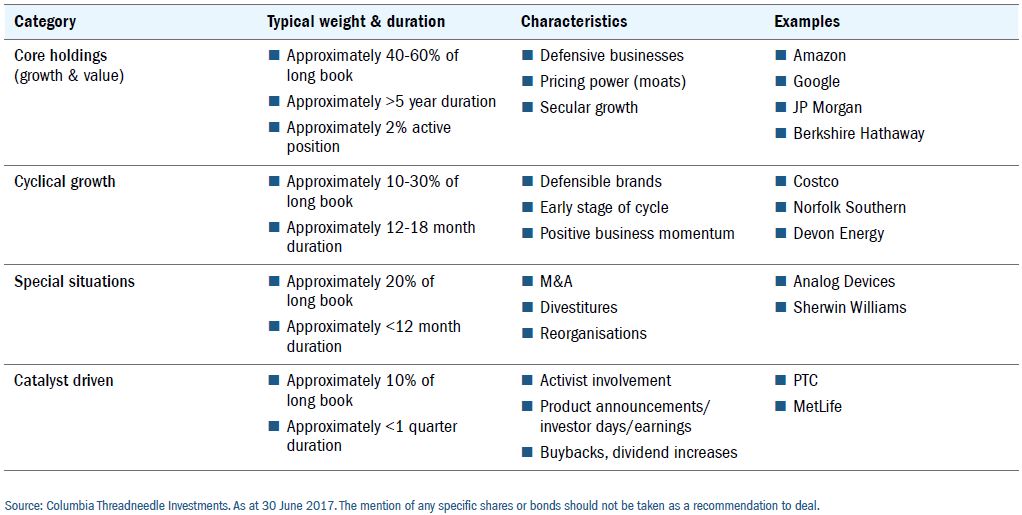

Our long book comprises four distinct ‘buckets’ (Figure 2): core growth and value stocks; cyclical growth stocks; special situations such as companies reorganising or involved in mergers; and catalyst-driven opportunities, such as companies due to make product announcements.

Figure 2: Long book construction

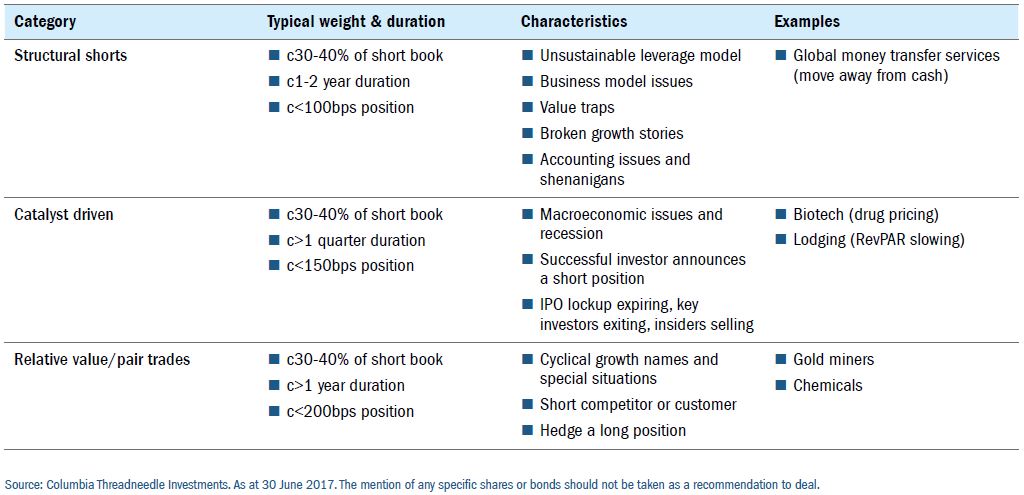

By contrast, our short book (Figure 3) contains: structural shorts; catalyst-driven opportunities; and relative value/pair trades.

Figure 3: Short book construction

In order to deliver a smooth return to investors, we aim to invest in companies which we believe will generate a 15% total operating earnings yield (operating earnings yield plus growth in operating earnings). This target is key because if we select the right companies, they have the potential to double their operating earnings yield over five years.

When the market is low, our short positions help us to maintain smooth returns for investors while also allowing us to buy more of our quality compounders. When the market recovers, we reduce our short positions and deliver returns due to our long holdings.

In response to recent market uncertainty, we have reduced the strategy’s number of holdings. At present, we have approximately 40 long and 40 short stocks. To make it into the portfolio, each stock must have a specific thesis, and we must be clear how the value will be unlocked. We aim to understand these businesses very well and also to have a deep understanding of how the stocks will react to the various market signals. This gives us the conviction to manage our positions precisely.

This is a stock-pickers equity market and we believe that only those asset managers with a robust research framework will be able to sustainably deliver alpha. After all, you need to be where the puck is going, not where it has been.