Although we had expressed concern demand could be weak for this first operation (due notably to the timing of the AQR, the results of which will be announced around 26 October), it seems were had underestimated the caginess of European banks. At the same time, and as pointed out by ECB Vice President Vitor Constancio, it will be necessary to wait for the results of the second operation on 11 December to pass a first judgement on TLTRO.

Several factors suggest that demand should be stronger for the second operation:

Several factors suggest that demand should be stronger for the second operation:

- First, the relatively small number of counterparties for this first TLTRO, with only 255 participants (out of a total of 382 eligible entities). Although the number of entities with an initial borrowing allowance is not known, the number of participants is substantially less than for the first VLTRO (523) and the second VLTRO (800).

- Second, press releases by the banks indicate that there was a higher participation by peripheral banks. Whereas Spanish and Italian MFI represent 32% of potential borrowing allowances (EUR 54bn and EUR 75.3bn), 14 of them have already borrowed EUR 39bn (or 47% of the EUR 82.6bn that will be allotted). It seems that core banks stayed on the sidelines, bearing in mind they account for more than 50% of potential borrowing allowances, but they could participate more massively in the December TLTRO.

- Some banks, one being Intesa, have already indicated that they will up applications for the December TLTRO.

- European banks with significant outstanding VLTRO will wait for the December TLTRO to avoid the extra 10bp associated to a roll (VLTRO liquidity costs 0.05% vs. 0.15% for TLTRO liquidity).

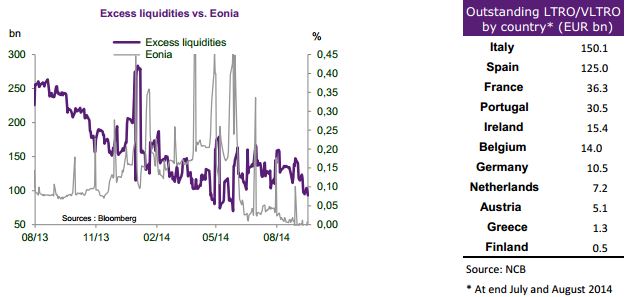

As regards the injection of liquidity in the short term, it will be necessary to wait for the ECB announcement concerning next week’s VLTRO repayments. Given the significant participation by Southern European banks (which have the biggest VLTRO outstandings and, in some cases, the least eligible collateral - see table overleaf), it is to be feared that a sizeable chunk of the EUR 82.6bn announced yesterday will be rolled, hence that the net injection of liquidity will be slight.

Under these conditions, assuming autonomous liquidity factors are stable, excess liquidity will in the best of cases recover to around EUR 180bn, while in the worst of cases it will be stable around EUR 93bn. Based on the premise that, in any case, VLTRO repayments will continue (on average EUR 5.6bn each week since July), excess liquidity observed in coming months is likely to converge towards EUR 100bn before rising from 17 December (allotment date for 2nd TLTRO).

While Eonia forwards did not budge much and still price in negative fixings out to the end of the year between -3bp and -4bp (-6bp mid 2015), the ECB will struggle to increase the amount of long-term liquidity provided unless there is an increase in loan production, which looks unlikely given growth prospects for the Eurozone economy. On the other hand, VLTRO repayments on 29 January and 26 February 2015 will see excess liquidity fall significantly below EUR 100bn.

Assuming that demand doubles for the December TLTRO (and that, as before, autonomous liquidity factors are stable), EUR 250bn would be allotted by the ECB, compared with which outstanding VLTRO would be EUR 341bn. This implies that nearly all the excess liquidity will be mopped up, hence the need for the ECB to embark rapidly on its ABS and covered bond purchases programmes to reverse this phenomenon.

While yesterday’s results do not bring into question the ECB’s objective of expanding its balance sheet, they do cast doubts about the central bank’s capacity to inject EUR 1,000bn (if it turns out that banks are reticent to participate in the TLTRO and that the ABS and covered bonds programmes do not amount to much because of the lack of liquidity for these asset classes). Unless there is a turnaround in Eurozone inflation (as ultimately the ECB’s mandate is to guarantee price stability), the probability of a fully-fledged QE, including the purchase of sovereigns, could rise gradually. In light of the selloff experienced by sovereigns yesterday, this option is not yet envisaged by the markets, but this could change rapidly.