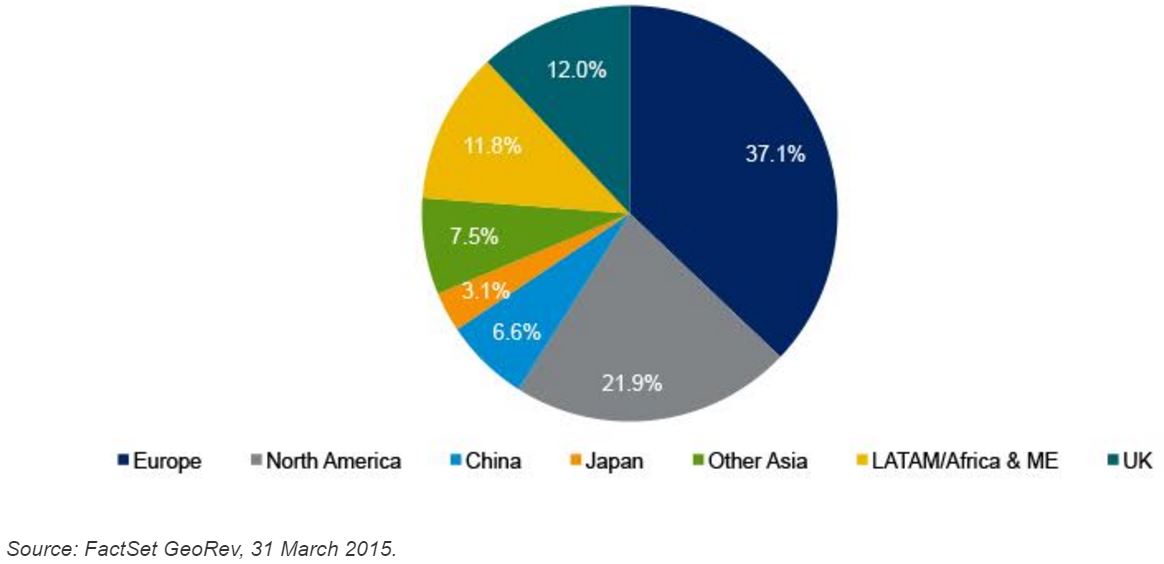

As investors in European equities, our focus is on stock-specific opportunities. We are agnostic as to where a company is based; what is important for us is finding individual stocks that have been mis-priced by the market. The macroeconomic environment is something we take into account, but it is possible to find interesting stock-level opportunities almost anywhere. Europe is an open economy and the kinds of companies we invest in often have operations not just in their home market but across the continent and the rest of the world too.

Chart 1: Geographical revenue exposure of MSCI Europe index

France (odds to win Euro 2016: 3/1) – opportunities in aerospace

France weathered both the global financial crisis and sovereign debt crisis better than many other European countries but growth has been hard to come by in the past few years. The French stockmarket encompasses a wide range of industries, both export- and domestic-focused. Aerospace & defence is one where we see opportunities. Partly this is to do with travel trends and the launch of new aircraft, but importantly we also see restructuring potential in the sector. Companies that have previously experienced problems, but are taking self-help measures to fix them, can be among the most interesting opportunities for us. These kinds of self-help stories are stock-specific by nature, and could potentially be found across any sector, or indeed any country.

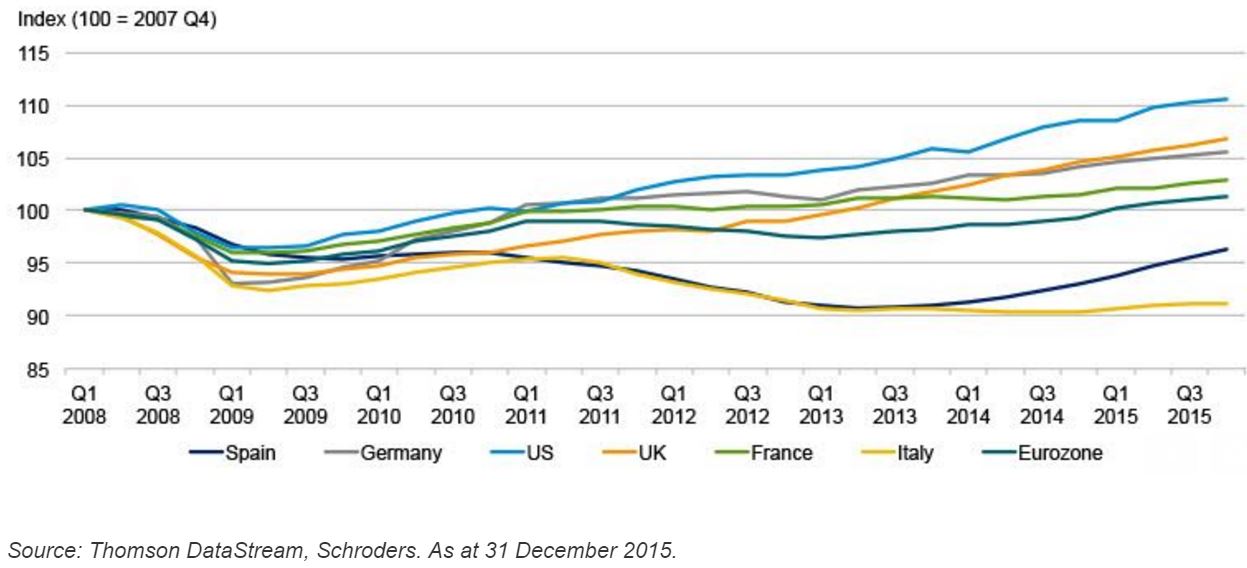

Chart 2: Real GDP since the global financial crisis

Germany (odds: 4/1) – not just about exports

Germany is well-known for its footballing prowess and the strength of its export sector. The automotive industry is perhaps the most obvious example and one that is enjoying strong demand currently. German car exports totalled $152.7 billion in 2015, representing 22.7% of the global total [1].

The opportunity presented by strong demand for cars is one that we prefer to access via the supply chain. Auto suppliers, in Germany and elsewhere, are at the forefront of technological innovation such as automatic safety features and indeed self-driving cars.

There are domestically-focused opportunities within Germany too, however, and one of these is the residential property segment. The low bond yield environment has contributed to the relative attractiveness of this sector but factors such as higher wages and a rising population in Germany are also important. The regional fragmentation of the sector means merger & acquisition appeal has been another draw.

Spain (odds: 5/1) – consumer recovery

Footballing success has been one of the few bright spots for Spain in the period since the global financial crisis. High unemployment, sovereign debt worries, and an overhang of speculative property developments were among the factors weighing on the economy. More recently, that picture has changed considerably and Spain was among the fastest-growing economies in Europe in 2015, with GDP up 3.2%. The inconclusive general election of 2015 appears to have been no barrier to the country’s ongoing economic improvement. The consumer sector is recovering strongly, as demonstrated by strong demand for new cars (registrations up 10.3% year-on-year in January-April 2016 [2]).

However, a more benign economic backdrop does not necessarily translate into opportunities for equity investors like ourselves. Spain’s main index, the Ibex 35, is dominated by banks; indeed just two banks make up 22.5% of the index [3]. We have concerns over the capital strength of the larger banks, some of which have significant international exposure. Tapping into Spain’s economic recovery does not necessarily mean investing in Spanish firms. The Spanish consumer recovery can be accessed by investing in companies - German auto parts firms, for example, or French hoteliers – which have operations across the region.

UK (odds: England 8/1, Wales 66/1, Northern Ireland 250/1) – heavy weighting to commodities

The UK is well-represented at Euro 2016, with Scotland the only nation to miss out. The point made earlier about the diverse revenue base of European stockmarkets applies doubly to the UK. Over 70% of the large cap FTSE 100’s revenues come from outside the UK [4]. Indeed, the composition of the index means it is often more exposed to global commodity price trends than to the health of the domestic UK economy. Oil & gas is 13.1% of the index and basic resources a further 5.7% [5]. The mid-cap FTSE 250 is often seen as more representative of the UK economy, with 52% of its revenues coming from the UK.

Belgium (odds: 11/1) – brewing giants

According to the bookmakers, Belgium’s football team may be competing with the giants of Europe but its stockmarket is relatively small. The 20 companies that make up Belgium’s main index – the BEL 20 - have a combined market capitalisation of €368 billion, compared to €1,207 billion for France’s 40-strong CAC index [6]. However, within this there are some well-known multinational firms, notably beverage and brewing group Anheuser-Busch InBev which is further enlarging itself with the acquisition of UK/South African brewer SABMiller.

Italy (odds: 18/1) – technology drives opportunities

Both the Italian and Spanish stockmarkets substantially underperformed their northern European counterparts in recent months and offer some interesting value opportunities. Again, banks form a large part of the Italian index. High levels of non-performing loans have been a source of concern so far this year, though we would note that the reform process is ongoing. Certain banks are well-capitalised and look attractive.

Chart 3: Spanish and Italian stockmarkets have underperformed recently

Technological innovation is perhaps not typically associated with Italy but there are several companies making use of technology to reach new audiences. One such is luxury goods group Yoox Net-a-Porter, an e-commerce platform selling designer clothing and accessories. Another is online banking and investment platform FinecoBank. Both provide an innovative service for consumers happy to save and spend online.