Risk assets have swiftly recovered from the late January pullback as the news flow on multiple fronts remains supportive. Both the earnings season and economic releases keep beating expectations on both sides of the Atlantic, while most recent Covid-19 trial results suggest vaccination campaigns may accelerate substantially in Q2. In the meantime, central banks remain highly accommodative and their guidance suggests it is unlikely to change in the coming quarters.

Additionally, the new U.S. administration is negotiating another fiscal stimulus package, which could end up above USD 1 trillion. In this context, long-dated inflation expectations have rebounded and reflation trades, which involve cyclical assets such as equities, EM assets, commodities and inflation breakevens, performed well and could continue to do so.

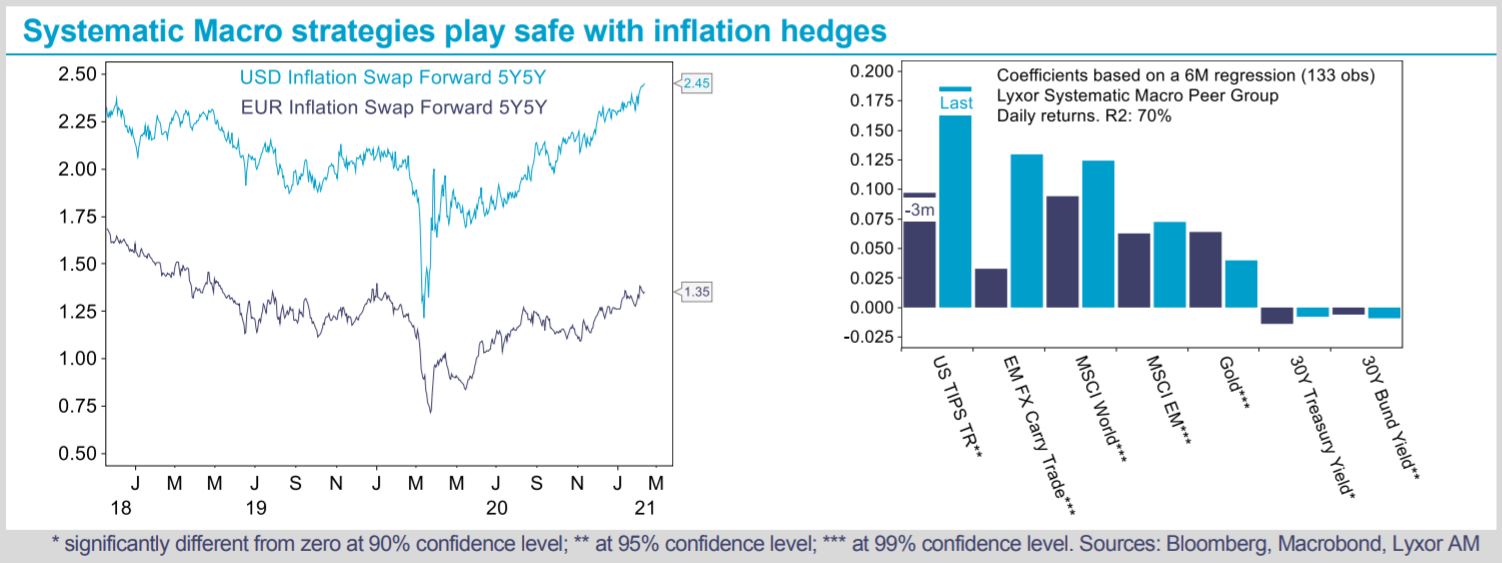

In the space of alternatives, Global Macro strategies have embraced reflation trades in the past quarter, scaling up positions on EM FX, equities, commodities and inflation linked bonds at varying degrees. Our estimates suggest Systematic Macro strategies have particularly increased positions into Treasury Inflation-Protected Securities (TIPS), while still having some residual exposure to duration on German bunds (see chart).

Long positions on EMFX and Gold also appear substantially above the average of recent years. In turn, Discretionary Macro strategies are positioned for a steepening of the Treasury curve, with some of them having turned outright short on Treasuries. They expect implied volatility in fixed income to rise and play that view via swaptions.

Going forward, investors face a delicate balancing act as rich equity valuations point to frothy markets, however, the positive earnings momentum will drag multiples lower. Our stance on Global Macro strategies stands at Overweight on the back of their ability to deliver returns and manage risks at this stage of the business cycle. Global Macro strategies have shown to be opportunistic in capturing risk premiums across asset classes and geographies according to market conditions. Their diversified portfolios and relative value approach should allow them to absorb regular spikes of volatility caused by lingering market concerns over the normalization of monetary policy and the sustainability of equity valuations.