With the sovereign debt crisis getting worse in Europe, highly different consequences are emerging for banks. Even if encouraging signs of an increased support to Greece are shaping up, European banks remain very strongly linked to sovereign spreads. According to the Goldman Sachs strategists, a convincing solution to financing issues in the Eurozone could lead to a strong rebound in bank shares but failure to develop such a solution would increase contagion risks and could cause a new round of selloff on equity markets. The American investment bank therefore recommends hedging extreme risks through puts with bank shares or the Eurostoxx 50 as underlyings. Explanations below...

- Banks: The binary dilemma

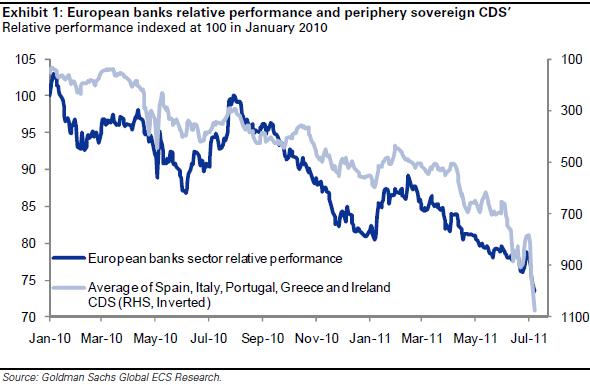

Goldman Sachs argues that it is obvious that in the short term equity markets will react to European policy and its consequences on sovereign spreads. With graphical evidence (see graphic 1), the bank shows that the relative performance of European banks has been highly correlated with the sovereign CDS of peripheral countries of the Eurozone. The experts of Goldman contend that if the spreads fall, this would reflect a greater willingness to finance budgetary transfers within the Eurozone which would lead to higher bank shares in the short term and consequently an equity market rally.

{kind=link}

- Hedging by purchasing puts looks attractive

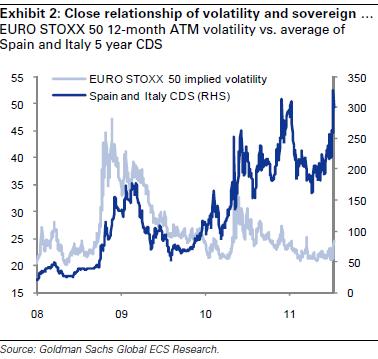

“However with the possibility that those extreme risks may happen, investors might wish to increase their hedging. We believe that put purchases on bank shares can lead an attractive hedging position with regard to the current market levels. Despite the recent widening of sovereign spreads in peripheral countries most notably Spain and Italy, implicit volatility remains comparably cheap” adds Goldman Sachs. Indeed, on the Eurostoxx 50, 12 month at the money volatility is around 25% which is much lower than the levels of May 2010 when it touched 33% (see graphic 2). 3-month at the money implied volatility on the Eurostoxx 50 is equally close to 25% while it reached 37% in May 2010. 12 month observed volatility on the Eurostoxx 50 had peaked at 25% in May 2010 when the index dropped by 17%. Since the beginning of July 2011, the index is down by 6%.

{kind=link}

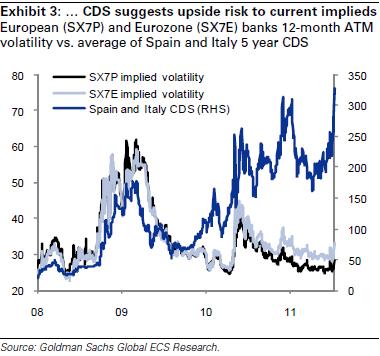

“With sovereign CDS at new peaks, we believe that there are still significant risks that implicit volatility may increase on the Eurostoxx 50. The same observation holds for the banking sector which is clearly the most vulnerable sector at the moment” justifies the Goldman Sachs strategic research team. Implicit volatility on European banks overall or simply on those of the Euro zone is much lower than the peaks reached last May (see graphic 3).

The drop in the synthetic SX7P index (representing European banks) was about 22% at that time while the banks have ceased to underperform since the beginning of the year. Right now they are trading at 9% below their highest yearly value. “It must be noted that banks and insurance companies represent 26.2% of the Eurostoxx 50 index and since the volatility of the index is currently lower than that of the sector, hedging through puts on equity indices is cheaper” specifies Goldman Sachs.

The drop in the synthetic SX7P index (representing European banks) was about 22% at that time while the banks have ceased to underperform since the beginning of the year. Right now they are trading at 9% below their highest yearly value. “It must be noted that banks and insurance companies represent 26.2% of the Eurostoxx 50 index and since the volatility of the index is currently lower than that of the sector, hedging through puts on equity indices is cheaper” specifies Goldman Sachs.

{kind=link}