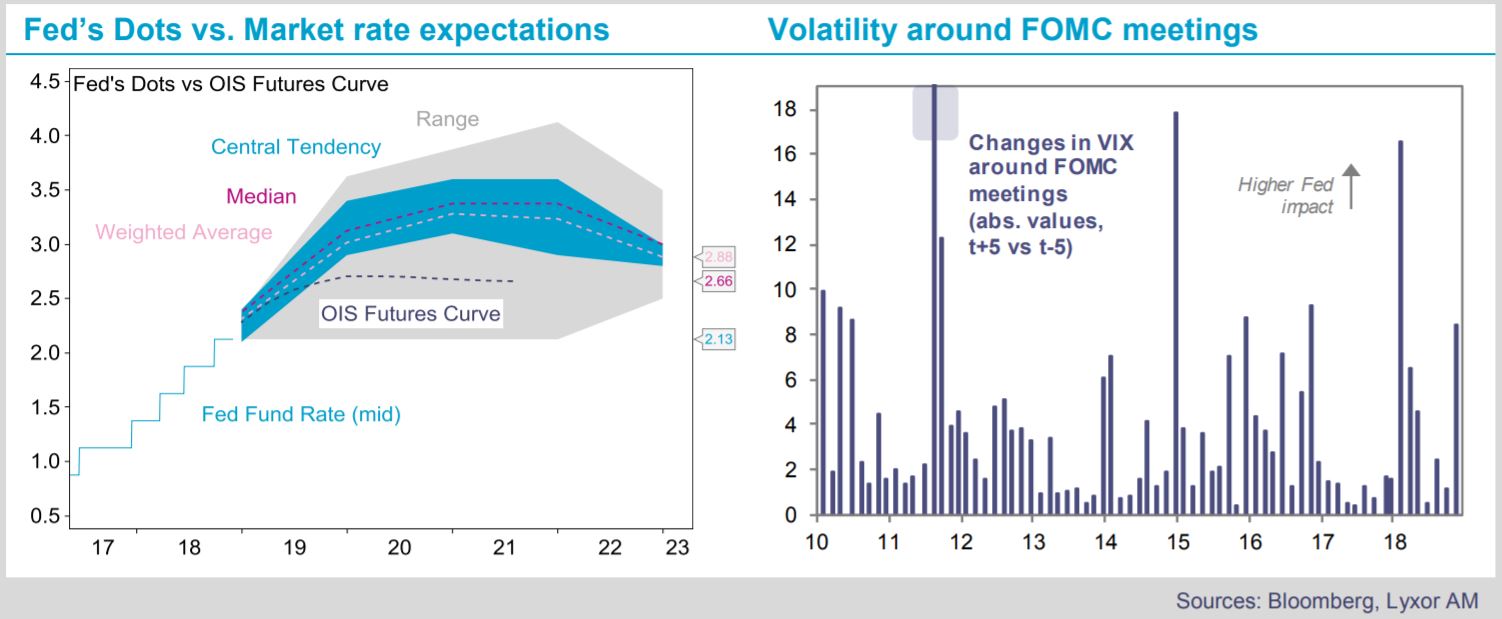

The confirmation of a changing Federal Reserve System’s ("Fed”) tone and hopes for a truce in the U.S. trade standoff both supported risky assets this week. Rates have been trending down since mid-November, in sync with a weakening pulse of global growth and escalating political risks in China and Europe. This week, the Fed Chair Jerome Powell shifted his stance, with rates considered being a “long way” from the neutral rate in October to “just below” from now on. The Fed’s minutes were also dovish. While pointing to a hike in December, they suggest the Fed would be increasingly data dependent. With sovereign yields down 25 bps since midNovember, markets are now expecting only two rate hikes in 2019, in addition to that of December’s.

The change of tone at the Fed is also being factored in hedge funds’ portfolios.

Overall, CTAs fully neutralized their short bond positions over the month of November. This was a fast reshuffling, though executed with diverging regional positioning. They cut about a quarter of their U.S. bond shorts, but they built up long bond positions both in Europe and Japan. We note that CTAs remain substantially long dollar against EUR, JPY, CHF, and GBP. They are also short in equities, especially in Europe and Japan. CTAs fully cut their energy positions.

Since the summer, Global Macro strategies generally made limited profits on bonds. A number of managers were expecting more Fed gradualism since the beginning of the fall, but generally positioned to that effect prematurely. They recently recovered part of the losses made before rates peaked. Managers expecting a more hawkish scenario saw a symmetrical profit pattern. Trading timing mattered more than the fundamental views.

Both sides have now converged on bonds. We see limited short U.S. duration in portfolios in favor of more relative value positions. Outside of the U.S., Global Macro strategies currently hold meaningful UK cash futures, and some strategies added long German duration to factor the weak European economic releases. We see more diverging stances in non-bond asset classes.