Since early September, risky assets have corrected as investors priced in a peak in global growth, broadening impacts from supply-chain bottlenecks, inflation data questioning the "transitory" narrative as well as the spike in energy prices, and central banks becoming more hawkish and preparing to taper their purchases. While China continued its regulatory crackdown, markets also had to digest the (managed) collapse of Evergrande and deepening power shortages. Finally, in the U.S., the political stalemate concerning infrastructure spending and the increasing of the debt ceiling added extra uncertainty.

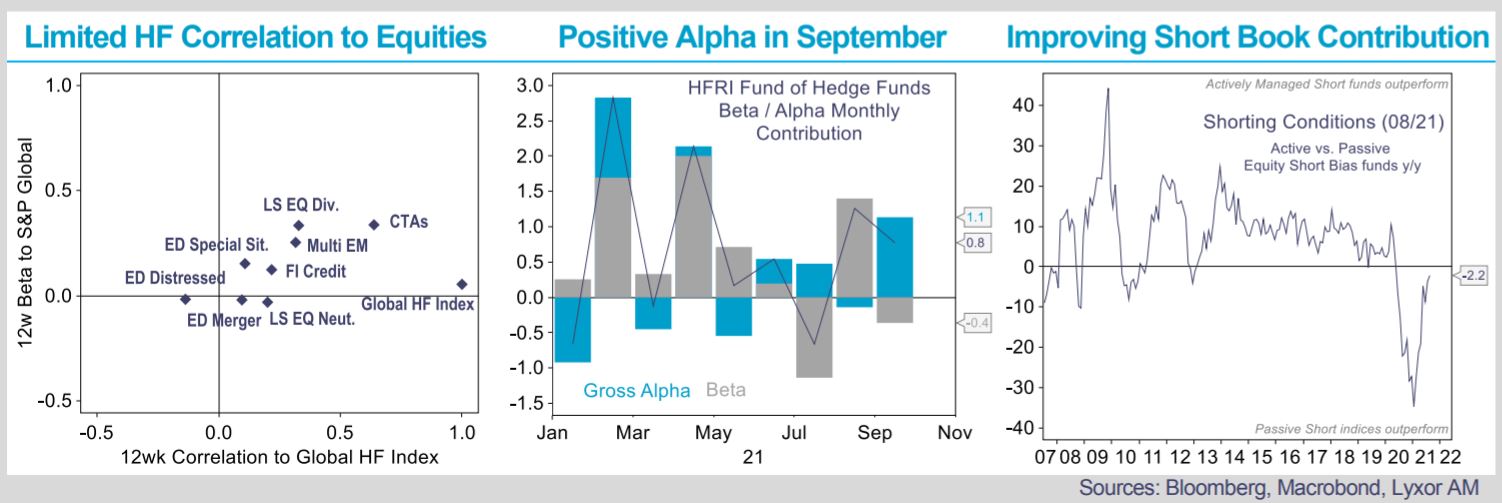

As a result, global equities headed south and sovereign yields surged in response to more hawkish central banks and firming inflation, with the ’stagflation’ narrative gaining support. Higher risk-aversion and the Fed’s nearing tapering supported the dollar, while credit spreads widened. Depleting inventories also boosted energy assets. Below we assess how hedge funds navigated increasingly challenging markets and discuss how they are currently positioned.

L/S Equity managers have decently navigated these markets, generating small positive alpha (especially on their short positions) but their implicit stance is diverging across regions. U.S. managers detracted only marginal alpha. They maintained their modest overall exposures throughout September and further reduced them early October, keeping limited factor tilts. They steadily reweighted the energy and rate-sensitive sectors, consistent with soaring energy prices and yields. Also, they just started to buy the dip on tech stocks that have corrected the most, as well as sectors negatively impacted by the pandemic. While they took profits on financials, they did not add much on defensive stocks. U.S. managers do not appear to be overly concerned by the macro backdrop, but higher tail risks, especially in the U.S., keep them in wait-and-see mode. Meanwhile, they are increasingly turning tactical and opportunistic.

In Europe, managers maintained their overall exposures, reweighted value, domestic stocks, and sectors more vulnerable to Covid, to leverage on economic reopening. They modestly added to industrials and energy, but do not have large sector bias. Regionally, they cut their UK and core-EMU allocations in favor of the Nordics. EU managers’ current stances are consistent with continued economic reopening and recovery, but with greater focus on risk management.

Managers in Japan have steadily increased their net exposures since August but took some profits by mid-September.

They gave back some of their alpha gains following policy announcements by the new PM Kishida. Subsequently, they sold

stocks vulnerable to greater wealth redistribution and tax prospects (one of Kishida’s priorities), but kept a positive tilt on

cyclicals, while staying neutral on value. They also added stocks most hit by Covid-restrictions. Japanese managers

appear confident that Japan’s recovery will re-accelerate, with a balanced contribution from external activity and

consumption. L/S China managers have generated small alpha since September. They have further reduced but not trashed their overall exposures, especially on

stocks sensitive to consumption and manufacturing. Instead,

they favor energy and stocks boosted by a secular trend (i.e.

those more likely to benefit from the ongoing economic model

re-orientation). They also started to buy on dip sold-out realestate and tech stocks. Their portfolios are now increasingly

focused on onshore and smaller caps. Chinese managers

seem to favor a "barbell approach", isolating their

portfolios from the ongoing cyclical risks while

concentrating their key calls on secular trends.

Event-Driven strategies have not substantially altered their

allocations. A number of merger deals in the consumer,

financial and energy sectors were unsettled by rising macro

uncertainties and selectively saw substantial spread

widening. Managers generated alpha thanks to quality dealpicking, while continuing to deploy more cash. Merger

managers still look optimistic despite the intensifying

regulatory risks. Special Situations managers maintain low

overall exposures, with a bias toward cyclicals, but not

specifically toward value. Special Situations managers

look increasingly focused on risk management.

Event-Driven strategies have not substantially altered their

allocations. A number of merger deals in the consumer,

financial and energy sectors were unsettled by rising macro

uncertainties and selectively saw substantial spread

widening. Managers generated alpha thanks to quality dealpicking, while continuing to deploy more cash. Merger

managers still look optimistic despite the intensifying

regulatory risks. Special Situations managers maintain low

overall exposures, with a bias toward cyclicals, but not

specifically toward value. Special Situations managers

look increasingly focused on risk management.

L/S Credit managers in the U.S. started to raise exposures (mainly through crossovers) as credit spreads widened. They have bought back some tech at the expense of industrial and consumer issues. In Europe, managers reduced exposures but still favor riskier segments. L/S Credit managers do not appear to expect major weakness in credit, at least in Europe where they feel confident to take more risk.

Global Macro managers’ low overall exposures, short bond positions and steepeners offset most of the losses from their long equity and short dollar positions. They further reduced their equity positions but do not seem to be taking profit yet on their short govies. Macro managers implicitly see the reflation story continuing, albeit at more moderate pace, and expect yields and inflation to firm up.

CTAs reduced their equities, nearly neutralized their long bond exposures, maintained their long energy holdings, and more recently added to base metals. CTAs are implicitly positioned for continued global recovery, limited further yield increase, with more hedges against surging riskaversion and inflation (through dollar and commodities).